Você também pode gostar

- The ECB Survey of Professional ForecastersDocumento12 páginasThe ECB Survey of Professional ForecasterscesareAinda não há avaliações

- NI Composite Economic Index Q3 2017Documento14 páginasNI Composite Economic Index Q3 2017Bianca ElenaAinda não há avaliações

- The ECB Survey of Professional ForecastersDocumento11 páginasThe ECB Survey of Professional ForecasterscesareAinda não há avaliações

- Nesg G1Documento6 páginasNesg G1yahayaAinda não há avaliações

- YR 12 Maths Exam QuestionsDocumento16 páginasYR 12 Maths Exam QuestionsakshatAinda não há avaliações

- INE Monthly Economic Survey July 2021 enDocumento14 páginasINE Monthly Economic Survey July 2021 enCatarina SantosAinda não há avaliações

- France vs Germany: An Analysis of Economic PerformanceDocumento25 páginasFrance vs Germany: An Analysis of Economic Performancevlad cernoutanAinda não há avaliações

- 2017 10 12 EXPO ForecastLAYFinalDocumento113 páginas2017 10 12 EXPO ForecastLAYFinalC.A.R. Research & EconomicsAinda não há avaliações

- Ba2 1 Aes2018Documento7 páginasBa2 1 Aes2018Ali EsmaeilbeygiAinda não há avaliações

- Annual Economic Report 2018 Part 1Documento24 páginasAnnual Economic Report 2018 Part 1sh_chandraAinda não há avaliações

- Medium Term Program (2017-2019) : October 4, 2016Documento28 páginasMedium Term Program (2017-2019) : October 4, 2016synwithgAinda não há avaliações

- Quarterly GDP Publication - Q4 2017Documento4 páginasQuarterly GDP Publication - Q4 2017BernewsAdminAinda não há avaliações

- Ant Montanes-Econ Sentiment & Confidence IndicDocumento14 páginasAnt Montanes-Econ Sentiment & Confidence IndicprofessionalAinda não há avaliações

- Institute and Faculty of Actuaries Examination: Subject CA3 - Communications Paper 2Documento6 páginasInstitute and Faculty of Actuaries Examination: Subject CA3 - Communications Paper 2anon_103901460Ainda não há avaliações

- March 2020Documento21 páginasMarch 2020yasahswi91Ainda não há avaliações

- SPAIN Trade Investment Statistical Country NoteDocumento10 páginasSPAIN Trade Investment Statistical Country Notelockleong93Ainda não há avaliações

- Task 2-Demand and Supply (350 Words) : - Great Supply Product: Motor VehicleDocumento10 páginasTask 2-Demand and Supply (350 Words) : - Great Supply Product: Motor VehicleLy Lê KhánhAinda não há avaliações

- Analyst Conference Call FY 2020: February 26, 2021Documento19 páginasAnalyst Conference Call FY 2020: February 26, 2021farokhcpuAinda não há avaliações

- Comparative Economic Analysis of India and SpainDocumento19 páginasComparative Economic Analysis of India and SpainDiksha LathAinda não há avaliações

- Sign in To Your AccountDocumento1 páginaSign in To Your AccountSlayerAinda não há avaliações

- Echap01 Vol2 PDFDocumento35 páginasEchap01 Vol2 PDFPASUPULA JAGADEESHAinda não há avaliações

- Business Expectations Survey: Fourth Quarter 2008Documento11 páginasBusiness Expectations Survey: Fourth Quarter 2008Rommel LoretoAinda não há avaliações

- 2017 q4 Commercial Real Estate Market Survey 3-8-2018Documento15 páginas2017 q4 Commercial Real Estate Market Survey 3-8-2018National Association of REALTORS®Ainda não há avaliações

- OECD GDP Growth Slows to 0.7% in Q4 2020Documento2 páginasOECD GDP Growth Slows to 0.7% in Q4 2020Nina KondićAinda não há avaliações

- Monthly Market Report 2 2017Documento28 páginasMonthly Market Report 2 2017Momo SemerkhetAinda não há avaliações

- Abhijit Ash - PHD PT - 22001 - Forecasting ModelsDocumento35 páginasAbhijit Ash - PHD PT - 22001 - Forecasting ModelsAbhijit AshAinda não há avaliações

- Economic AssignmentDocumento13 páginasEconomic AssignmentZhomeAinda não há avaliações

- Annual Economic Report 2018 Part 2Documento18 páginasAnnual Economic Report 2018 Part 2sh_chandraAinda não há avaliações

- 2018 q1 Commercial Real Estate Market Survey 09-07-2018Documento15 páginas2018 q1 Commercial Real Estate Market Survey 09-07-2018National Association of REALTORS®Ainda não há avaliações

- Business Expectations Survey: Third Quarter 2007Documento10 páginasBusiness Expectations Survey: Third Quarter 2007Rommel LoretoAinda não há avaliações

- MONTHLY ECONOMIC REPORT HIGHLIGHTSDocumento22 páginasMONTHLY ECONOMIC REPORT HIGHLIGHTSMadan GoswamiAinda não há avaliações

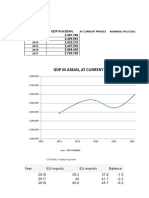

- ASEAN GDP 2012-2017Documento3 páginasASEAN GDP 2012-2017Mehul AgarwallaAinda não há avaliações

- Figure 2, We Can See That Manufacturing, Wholesale Retail and Motor Repair, and Agriculture, ForestryDocumento4 páginasFigure 2, We Can See That Manufacturing, Wholesale Retail and Motor Repair, and Agriculture, ForestryMikko VitugAinda não há avaliações

- p1d 20180604 Klems Solving The Productivity Puzzle Jaana RemesDocumento22 páginasp1d 20180604 Klems Solving The Productivity Puzzle Jaana RemesJamesMinionAinda não há avaliações

- The Hike in Core Consumer Price Index Is Temporary: CPI-U: All ItemsDocumento9 páginasThe Hike in Core Consumer Price Index Is Temporary: CPI-U: All ItemsInternational Business TimesAinda não há avaliações

- A1 - Part 1Documento18 páginasA1 - Part 1An KhánhhAinda não há avaliações

- Eurozone Crisis - SpainDocumento31 páginasEurozone Crisis - SpainMaitreyee GoswamiAinda não há avaliações

- High Uncertainty Weighing On Global Growth OECD Interim Economic Outlook Presentation 20 September 2018Documento24 páginasHigh Uncertainty Weighing On Global Growth OECD Interim Economic Outlook Presentation 20 September 2018ngnquyetAinda não há avaliações

- Feaco - Survey 2018 2019Documento46 páginasFeaco - Survey 2018 2019ΒΑΣΙΛΕΙΟΣ ΙΣΜΥΡΛΗΣAinda não há avaliações

- Press Release: Issued by DateDocumento5 páginasPress Release: Issued by DateMuhazzam MaazAinda não há avaliações

- Economic Survey IndiaDocumento16 páginasEconomic Survey IndiaAtanu MukherjeeAinda não há avaliações

- Figures and CommentsDocumento19 páginasFigures and CommentsTBP_Think_TankAinda não há avaliações

- Nielsen - A Weakening of Consumer Purchase or ShiftingDocumento42 páginasNielsen - A Weakening of Consumer Purchase or ShiftingTotok SediyantoroAinda não há avaliações

- Global Economics Outlook Points to Accelerating Eurozone GrowthDocumento1 páginaGlobal Economics Outlook Points to Accelerating Eurozone Growthshaan1001gbAinda não há avaliações

- 2018 - 02 - 20 Short - Country-Presentation - InvestRomaniaDocumento22 páginas2018 - 02 - 20 Short - Country-Presentation - InvestRomaniaJonian MollaAinda não há avaliações

- Analysis of Relation Between Budgets and Revenues From MoviesDocumento5 páginasAnalysis of Relation Between Budgets and Revenues From MoviesInternational Journal of Innovative Science and Research TechnologyAinda não há avaliações

- News Coverage - France: Economy and Business News From The Past WeekDocumento6 páginasNews Coverage - France: Economy and Business News From The Past Weekapi-248259954Ainda não há avaliações

- News Coverage - France: Economy and Business News From The Past WeekDocumento6 páginasNews Coverage - France: Economy and Business News From The Past Weekapi-248259954Ainda não há avaliações

- Dr. Abola - MacroeconomyDocumento34 páginasDr. Abola - MacroeconomyJonathan AguilarAinda não há avaliações

- Key Economic Challenges Facing JapanDocumento24 páginasKey Economic Challenges Facing JapanJohnAinda não há avaliações

- The ECB Survey of Professional ForecastersDocumento23 páginasThe ECB Survey of Professional ForecasterscesareAinda não há avaliações

- T E S - J 2017: Transmission of Material in This Release Is Embargoed Until 8:30 A.M. (EST) Friday, February 3, 2017Documento42 páginasT E S - J 2017: Transmission of Material in This Release Is Embargoed Until 8:30 A.M. (EST) Friday, February 3, 2017mukeshAinda não há avaliações

- JLL Italian Logistics Snapshot q2 2023Documento18 páginasJLL Italian Logistics Snapshot q2 2023abdalrahmananas45Ainda não há avaliações

- Reimv - 20100813 - UK Spotlight - August 2010Documento14 páginasReimv - 20100813 - UK Spotlight - August 2010alan.pattersonAinda não há avaliações

- The World in 2050Documento46 páginasThe World in 2050Ed WardAinda não há avaliações

- The ECB Survey of Professional ForecastersDocumento18 páginasThe ECB Survey of Professional ForecastersaldhibahAinda não há avaliações

- Business confidence hits record highDocumento7 páginasBusiness confidence hits record highRommel LoretoAinda não há avaliações

- Mahamoud IslamDocumento21 páginasMahamoud Islamvkumar66Ainda não há avaliações

- Economic and Business Forecasting: Analyzing and Interpreting Econometric ResultsNo EverandEconomic and Business Forecasting: Analyzing and Interpreting Econometric ResultsAinda não há avaliações

- Market Declines: What Is Accomplished by Banning Short-Selling?Documento7 páginasMarket Declines: What Is Accomplished by Banning Short-Selling?annawitkowski88Ainda não há avaliações

- Fintech Innovation in The Home Purchase and Financing Market 0Documento15 páginasFintech Innovation in The Home Purchase and Financing Market 0TBP_Think_TankAinda não há avaliações

- Covid 2Documento7 páginasCovid 2TBP_Think_Tank100% (2)

- HHRG 116 BA16 Wstate IsolaD 20190314Documento4 páginasHHRG 116 BA16 Wstate IsolaD 20190314TBP_Think_Tank0% (1)

- CPC Hearings Nyu 12-6-18Documento147 páginasCPC Hearings Nyu 12-6-18TBP_Think_TankAinda não há avaliações

- wp2017 25Documento123 páginaswp2017 25TBP_Think_Tank100% (7)

- Vanguard - Barry Q&ADocumento5 páginasVanguard - Barry Q&ATBP_Think_TankAinda não há avaliações

- WEF BookDocumento78 páginasWEF BookZerohedge100% (1)

- 381-2018 FetzerDocumento100 páginas381-2018 FetzerTBP_Think_TankAinda não há avaliações

- p60 263Documento74 páginasp60 263TBP_Think_TankAinda não há avaliações

- Insight: Can The Euro Rival The Dollar?Documento6 páginasInsight: Can The Euro Rival The Dollar?TBP_Think_TankAinda não há avaliações

- Nafta Briefing April 2018 Public Version-FinalDocumento17 páginasNafta Briefing April 2018 Public Version-FinalTBP_Think_TankAinda não há avaliações

- ISGQVAADocumento28 páginasISGQVAATBP_Think_Tank100% (1)

- Rising Rates, Flatter Curve: This Time Isn't Different, It Just May Take LongerDocumento5 páginasRising Rates, Flatter Curve: This Time Isn't Different, It Just May Take LongerTBP_Think_TankAinda não há avaliações

- El2018 19Documento5 páginasEl2018 19TBP_Think_Tank100% (1)

- Bullard Glasgow Chamber 20 July 2018Documento33 páginasBullard Glasgow Chamber 20 July 2018TBP_Think_TankAinda não há avaliações

- Solving Future Skills ChallengesDocumento32 páginasSolving Future Skills ChallengesTBP_Think_Tank100% (1)

- R 180726 GDocumento2 páginasR 180726 GTBP_Think_TankAinda não há avaliações

- F 2807 SuerfDocumento11 páginasF 2807 SuerfTBP_Think_TankAinda não há avaliações

- Inequalities in Household Wealth Across OECD Countries: OECD Statistics Working Papers 2018/01Documento70 páginasInequalities in Household Wealth Across OECD Countries: OECD Statistics Working Papers 2018/01TBP_Think_TankAinda não há avaliações

- Williamson 020418Documento67 páginasWilliamson 020418TBP_Think_TankAinda não há avaliações

- Macro Aspects of Housing: Federal Reserve Bank of Dallas Globalization and Monetary Policy InstituteDocumento73 páginasMacro Aspects of Housing: Federal Reserve Bank of Dallas Globalization and Monetary Policy InstituteTBP_Think_TankAinda não há avaliações

- DP 11648Documento52 páginasDP 11648TBP_Think_TankAinda não há avaliações

- pb18 16Documento8 páginaspb18 16TBP_Think_TankAinda não há avaliações

- Trade Patterns of China and India: Analytical Articles Economic Bulletin 3/2018Documento14 páginasTrade Patterns of China and India: Analytical Articles Economic Bulletin 3/2018TBP_Think_TankAinda não há avaliações

- The Economics of Subsidizing Sports Stadiums SEDocumento4 páginasThe Economics of Subsidizing Sports Stadiums SETBP_Think_TankAinda não há avaliações

- Financial Stability ReviewDocumento188 páginasFinancial Stability ReviewTBP_Think_TankAinda não há avaliações

- Working Paper Series: Exchange Rate Forecasting On A NapkinDocumento19 páginasWorking Paper Series: Exchange Rate Forecasting On A NapkinTBP_Think_TankAinda não há avaliações

- HFS Essay 2 2018Documento24 páginasHFS Essay 2 2018TBP_Think_TankAinda não há avaliações

- Has18 062018Documento116 páginasHas18 062018TBP_Think_TankAinda não há avaliações

- Functional English: TopicDocumento20 páginasFunctional English: TopicMughal ManoAinda não há avaliações

- Role of Entrepreneurship in Economic DvelopmentDocumento2 páginasRole of Entrepreneurship in Economic Dvelopmentamit_sachdevaAinda não há avaliações

- Youth Unemployment in South Africa Reasons, Costs and SolutionsDocumento3 páginasYouth Unemployment in South Africa Reasons, Costs and Solutionslandiwe NtumbaAinda não há avaliações

- Lec-2 - Chapter 23 - Nation's IncomeDocumento33 páginasLec-2 - Chapter 23 - Nation's IncomeMsKhan0078Ainda não há avaliações

- Chapter 7 Unemployment and The Labor MarketDocumento7 páginasChapter 7 Unemployment and The Labor MarketJoana Marie Calderon100% (1)

- Supportive MaterialDocumento2 páginasSupportive Materialhriday ganeshAinda não há avaliações

- MCD 2090 Tutorial Questions T6-Wk6Documento7 páginasMCD 2090 Tutorial Questions T6-Wk6Leona AriesintaAinda não há avaliações

- Social Problems in SocietiesDocumento4 páginasSocial Problems in SocietiesRobert Okoth OwuorAinda não há avaliações

- Developed & Underdeveloped (PPT)Documento22 páginasDeveloped & Underdeveloped (PPT)kavya ShivanandhAinda não há avaliações

- Banking On Cash Saudi Oil Woes The Index Factor: HMRC Faces Bill of Up To 43bn in Worst-Estimate' Refund BattleDocumento26 páginasBanking On Cash Saudi Oil Woes The Index Factor: HMRC Faces Bill of Up To 43bn in Worst-Estimate' Refund BattlestefanoAinda não há avaliações

- Bangladesh's Growing Income InequalityDocumento15 páginasBangladesh's Growing Income Inequalityফারুক হোসেন রিমন0% (1)

- Eco 404 Slides 2022Documento16 páginasEco 404 Slides 2022Abane Jude yenAinda não há avaliações

- Effects of Youth Unemployment on Income in Central Equatoria, South SudanDocumento53 páginasEffects of Youth Unemployment on Income in Central Equatoria, South SudanMichelle Magallen BellezaAinda não há avaliações

- Mining in the Philippines: A Destructive PracticeDocumento5 páginasMining in the Philippines: A Destructive PracticeIsaac Louise BaraquielAinda não há avaliações

- Akiko Sakamoto - Skills Development in Time of Continuing Job CrisisDocumento12 páginasAkiko Sakamoto - Skills Development in Time of Continuing Job Crisissmariano908Ainda não há avaliações

- IBM530 Assignment 2 - Individual Case StudyDocumento4 páginasIBM530 Assignment 2 - Individual Case StudyancamyuiAinda não há avaliações

- Soft skills II: Group project explores job opportunities for young peopleDocumento18 páginasSoft skills II: Group project explores job opportunities for young peopleOmar ALSHBLIAinda não há avaliações

- Basic Economics Understanding TestDocumento5 páginasBasic Economics Understanding TestDr Rushen SinghAinda não há avaliações

- Blood Brothers Knowledge OrganiserDocumento1 páginaBlood Brothers Knowledge OrganiserSAinda não há avaliações

- - -CPE-Useful-Idioms-Phrases - -Sheet1-đã chuyển đổiDocumento12 páginas- -CPE-Useful-Idioms-Phrases - -Sheet1-đã chuyển đổiĐào HiếuAinda não há avaliações

- The Great Depression of 1929Documento8 páginasThe Great Depression of 1929vishal_sagittAinda não há avaliações

- To Kill A Mockingbird by Harper Lee Chapter 1 To 7 Student HandoutDocumento7 páginasTo Kill A Mockingbird by Harper Lee Chapter 1 To 7 Student HandoutAnalisa JerueAinda não há avaliações

- Globalization & Cultural Differences in Strategic ManagementDocumento25 páginasGlobalization & Cultural Differences in Strategic ManagementSuciana Faskalina100% (1)

- The Impact of Unemployment of Economic Growth in Calamba City, LagunaDocumento16 páginasThe Impact of Unemployment of Economic Growth in Calamba City, LagunaKurt RaferAinda não há avaliações

- Unemployment (Economics) : Did You Understand The Text?Documento1 páginaUnemployment (Economics) : Did You Understand The Text?Alan CarranzaAinda não há avaliações

- Reorganise Relocate Deregulate Decentralise: - AtionDocumento5 páginasReorganise Relocate Deregulate Decentralise: - AtionLeena LebedevaAinda não há avaliações

- Zutavern J & Kohli M. Needs and Risks in The Welfare State.Documento21 páginasZutavern J & Kohli M. Needs and Risks in The Welfare State.Paulo TavaresAinda não há avaliações

- Economics Problem Set ExplainedDocumento8 páginasEconomics Problem Set ExplainedСофия МашьяноваAinda não há avaliações

- Instructions: Pager/XmlDocumento104 páginasInstructions: Pager/XmlWallace DittrichAinda não há avaliações

- Business CycleDocumento3 páginasBusiness CycleHlengiwe PhewaAinda não há avaliações