Você também pode gostar

- Circular 423 DOSRIDocumento11 páginasCircular 423 DOSRIDaryl G. LiangcoAinda não há avaliações

- c914 - 2016 Updates On DOSRI Rule PDFDocumento19 páginasc914 - 2016 Updates On DOSRI Rule PDFJoey SulteAinda não há avaliações

- Sec. 35. Limit On Loans, Credit Accommodations and Guarantees.Documento10 páginasSec. 35. Limit On Loans, Credit Accommodations and Guarantees.BernadetteGaleraAinda não há avaliações

- Inclusion To SBL To Dosri NotesDocumento2 páginasInclusion To SBL To Dosri NotesRon VirayAinda não há avaliações

- Special Assignment (Loan Function of Banks)Documento9 páginasSpecial Assignment (Loan Function of Banks)Michee BiagAinda não há avaliações

- Banking Regulation & Policy Department Bangladesh Bank Head Office DhakaDocumento8 páginasBanking Regulation & Policy Department Bangladesh Bank Head Office DhakaKhandaker Amir EntezamAinda não há avaliações

- BSP Policy StatementsDocumento8 páginasBSP Policy StatementsMark TeaAinda não há avaliações

- Loan Function of BanksDocumento4 páginasLoan Function of BanksSherlyn Paran Paquit-SeldaAinda não há avaliações

- SBB 29 02Documento5 páginasSBB 29 02Afework AtnafsegedAinda não há avaliações

- BSP Circular 170Documento2 páginasBSP Circular 170RJ SakuragiAinda não há avaliações

- Connected LendingDocumento5 páginasConnected Lending22satendraAinda não há avaliações

- Republic Act No. 3591 An Act Establishing The Philippine Deposit Insurance Corporation, Defining ITS Powers and Duties and For Other PurposesDocumento28 páginasRepublic Act No. 3591 An Act Establishing The Philippine Deposit Insurance Corporation, Defining ITS Powers and Duties and For Other PurposesJayMichaelAquinoMarquezAinda não há avaliações

- Banking Reviewer - Atty. CabaneiroDocumento10 páginasBanking Reviewer - Atty. CabaneiroYieMaghirangAinda não há avaliações

- Banking Midterms ReviewerDocumento6 páginasBanking Midterms ReviewerYieMaghirangAinda não há avaliações

- General Terms and Conditions - Personal LoansDocumento14 páginasGeneral Terms and Conditions - Personal LoansSumesh Kumar Prabhu SAinda não há avaliações

- Republic Act No. 3591: Per DiemDocumento12 páginasRepublic Act No. 3591: Per DiemEvielyn MateoAinda não há avaliações

- Philippine Deposit Insurance System R.A. No. 3591Documento14 páginasPhilippine Deposit Insurance System R.A. No. 3591Chris ChanAinda não há avaliações

- Assignment 7Documento62 páginasAssignment 7edrianclydeAinda não há avaliações

- The General Banking Law of 2000 Section 35 To Section 66Documento14 páginasThe General Banking Law of 2000 Section 35 To Section 66Carina Amor ClaveriaAinda não há avaliações

- Jose C. Go V. Bangko Sentral NG Pilipinas, G.R. No. 178429 October 23, 2009Documento35 páginasJose C. Go V. Bangko Sentral NG Pilipinas, G.R. No. 178429 October 23, 2009Nica NebrejaAinda não há avaliações

- 1-Pdic Law With 2 Amendatory LawsDocumento41 páginas1-Pdic Law With 2 Amendatory LawsJemima BukingAinda não há avaliações

- Chapter 4 - Purpose of Examination and SupervisionDocumento5 páginasChapter 4 - Purpose of Examination and SupervisionMhaiAinda não há avaliações

- (1963) RA 3591-PDIC CharterDocumento10 páginas(1963) RA 3591-PDIC CharterDuko Alcala EnjambreAinda não há avaliações

- Commercial LawDocumento193 páginasCommercial LawLouisa MatubisAinda não há avaliações

- Chapter 4 Purpose of Examination and SupervisionDocumento5 páginasChapter 4 Purpose of Examination and SupervisionMariel Crista Celda MaravillosaAinda não há avaliações

- Ra 3591 - PdicDocumento7 páginasRa 3591 - PdicIzobelle Pulgo100% (2)

- RA 3591 Philippine Deposit Insurance Corporation ActDocumento14 páginasRA 3591 Philippine Deposit Insurance Corporation ActKristine Kyle AgneAinda não há avaliações

- Restrictions On Loans and AdvancesDocumento1 páginaRestrictions On Loans and AdvancesBabu babuAinda não há avaliações

- Policy On Loans To Directors and Senior OffcialsDocumento8 páginasPolicy On Loans To Directors and Senior OffcialssagarthegameAinda não há avaliações

- New Deal Banking Act of 1933Documento29 páginasNew Deal Banking Act of 1933api-283648031Ainda não há avaliações

- Jan 162022 BRPD 01 eDocumento7 páginasJan 162022 BRPD 01 epk ghoshAinda não há avaliações

- PDICDocumento15 páginasPDICLouisse Vivien Santos LopezAinda não há avaliações

- FIM Summary of Bank Companies ActDocumento6 páginasFIM Summary of Bank Companies ActafridaAinda não há avaliações

- RA 9302 & 3591 - "Charter of The Philippine Deposit Insurance Corporation" and For Other PurposesDocumento27 páginasRA 9302 & 3591 - "Charter of The Philippine Deposit Insurance Corporation" and For Other PurposesJoeyMendozAinda não há avaliações

- CFAF Std. T&C (EL) - Standard Terms and Conditions Governing Education LoanDocumento5 páginasCFAF Std. T&C (EL) - Standard Terms and Conditions Governing Education LoanAvinab PandeyAinda não há avaliações

- AGREEMENT FOR PERSONAL LOAN - RevisedDocumento16 páginasAGREEMENT FOR PERSONAL LOAN - RevisedVinod VermaAinda não há avaliações

- Semi Final SPECIAL LAWSDocumento87 páginasSemi Final SPECIAL LAWSRedgie Mark Rosatase UrsalAinda não há avaliações

- Amended Draft Circular Transfer of Significant InterestDocumento13 páginasAmended Draft Circular Transfer of Significant InterestJM CBAinda não há avaliações

- General Terms and Conditions of South Indian Bank For Credit Facilities PDFDocumento29 páginasGeneral Terms and Conditions of South Indian Bank For Credit Facilities PDFbaba ramdevAinda não há avaliações

- Be It Enacted by The Senate and House of Representatives of The Philippine Congress AssembledDocumento11 páginasBe It Enacted by The Senate and House of Representatives of The Philippine Congress AssembledCeline MelchorAinda não há avaliações

- University of Mumbai: Submitted ToDocumento65 páginasUniversity of Mumbai: Submitted TomaheshAinda não há avaliações

- Loan Functions of BanksDocumento6 páginasLoan Functions of BanksMark AmistosoAinda não há avaliações

- Classification of BanksDocumento7 páginasClassification of BanksBrian PapellerasAinda não há avaliações

- 12 U.S. Code 1431 - Powers and Duties of Banks - U.S. Code - US Law - LII - Legal Information InstituteDocumento10 páginas12 U.S. Code 1431 - Powers and Duties of Banks - U.S. Code - US Law - LII - Legal Information InstituteDuke HunterAinda não há avaliações

- Terms and Conditions Governing Unsecured LoansDocumento15 páginasTerms and Conditions Governing Unsecured LoansamitioraAinda não há avaliações

- The State Bank of Vietnam Socialist Republic of Viet Nam Independence - Freedom - HappinessDocumento17 páginasThe State Bank of Vietnam Socialist Republic of Viet Nam Independence - Freedom - HappinessFx121Ainda não há avaliações

- Module 6.3 Banking RegulationDocumento22 páginasModule 6.3 Banking Regulationmay villzAinda não há avaliações

- 362 Credit Exposure Limits To A Single BorrowerDocumento10 páginas362 Credit Exposure Limits To A Single BorrowerBettina BarrionAinda não há avaliações

- Prudential Regulations FOR Small Enterprises Financing: First Edition-2004Documento61 páginasPrudential Regulations FOR Small Enterprises Financing: First Edition-2004rigan555Ainda não há avaliações

- Personal Loan Agreement: Bajaj Finance LimitedDocumento12 páginasPersonal Loan Agreement: Bajaj Finance LimitedShafiah SheikhAinda não há avaliações

- Credit Policy 25 DOSRI of Banking InstitutionDocumento18 páginasCredit Policy 25 DOSRI of Banking InstitutionNoel IV T. BorromeoAinda não há avaliações

- DOSRI AccountsDocumento3 páginasDOSRI AccountsJanna Robles SantosAinda não há avaliações

- Single Borrower ExposureDocumento7 páginasSingle Borrower ExposureSiam HasanAinda não há avaliações

- Compiled Cases Soriano vs. People Up To Alan Limso vs. PNBDocumento7 páginasCompiled Cases Soriano vs. People Up To Alan Limso vs. PNBKylie GavinneAinda não há avaliações

- Commercial Law ReviewerDocumento26 páginasCommercial Law ReviewerBill DiazAinda não há avaliações

- BSP Circular 969Documento38 páginasBSP Circular 969Rina Fajardo - NacinAinda não há avaliações

- The World Bank Group Sanctions Process and its Recent ReformsNo EverandThe World Bank Group Sanctions Process and its Recent ReformsAinda não há avaliações

- Unlocking Capital: The Power of Bonds in Project FinanceNo EverandUnlocking Capital: The Power of Bonds in Project FinanceAinda não há avaliações

- The Fiduciary: An In-Depth Guide to Fiduciary Duties-From Studebaker to EnronNo EverandThe Fiduciary: An In-Depth Guide to Fiduciary Duties-From Studebaker to EnronAinda não há avaliações

- The Law or To Disregard Established Rules (Are Proven) by Substantial Evidence."Documento8 páginasThe Law or To Disregard Established Rules (Are Proven) by Substantial Evidence."mjpjoreAinda não há avaliações

- The LTFRB Issued Memorandum CircularDocumento1 páginaThe LTFRB Issued Memorandum CircularmjpjoreAinda não há avaliações

- Administrativa Sanitario Records Section So Republic: PhilippinesDocumento15 páginasAdministrativa Sanitario Records Section So Republic: PhilippinesmjpjoreAinda não há avaliações

- Lang Naman Ang Gagawin Niyan, Right?Documento2 páginasLang Naman Ang Gagawin Niyan, Right?mjpjoreAinda não há avaliações

- Promissory NoteDocumento1 páginaPromissory NotemjpjoreAinda não há avaliações

- Obq Obli FinalDocumento97 páginasObq Obli FinalmjpjoreAinda não há avaliações

- Civil Law Memory JoggerDocumento3 páginasCivil Law Memory JoggermjpjoreAinda não há avaliações

- Civrev Marriage FinalasfhhDocumento65 páginasCivrev Marriage FinalasfhhmjpjoreAinda não há avaliações

- For Finals CrimrevDocumento41 páginasFor Finals CrimrevmjpjoreAinda não há avaliações

- ComplaintDocumento2 páginasComplaintmjpjoreAinda não há avaliações

- Peralta, J. (2012)Documento58 páginasPeralta, J. (2012)mjpjoreAinda não há avaliações

- Matthew John AlmoginoDocumento2 páginasMatthew John AlmoginomjpjoreAinda não há avaliações

- Albert v. University Publishing (Jore)Documento2 páginasAlbert v. University Publishing (Jore)mjpjoreAinda não há avaliações

- Western Institute Vs Salas (Jore)Documento2 páginasWestern Institute Vs Salas (Jore)mjpjoreAinda não há avaliações

- Cas SyapDocumento2 páginasCas SyapmjpjoreAinda não há avaliações

- Atty Leni and Ana MarieDocumento2 páginasAtty Leni and Ana MariemjpjoreAinda não há avaliações

- Atty Francisco GatchalianDocumento2 páginasAtty Francisco GatchalianmjpjoreAinda não há avaliações

- Tan v. SEC (Jore)Documento2 páginasTan v. SEC (Jore)mjpjoreAinda não há avaliações

- 68 Pacific Rehouse Vs CA (Ma Jovi Jore)Documento1 página68 Pacific Rehouse Vs CA (Ma Jovi Jore)mjpjoreAinda não há avaliações

- Yijuico v. Quiambao (Jore)Documento2 páginasYijuico v. Quiambao (Jore)mjpjoreAinda não há avaliações

- CMMCI v. Tsukahara (Jore)Documento2 páginasCMMCI v. Tsukahara (Jore)mjpjoreAinda não há avaliações

- 1st OBQ ObliconDocumento5 páginas1st OBQ ObliconmjpjoreAinda não há avaliações

- Obq Obli FinalDocumento3 páginasObq Obli FinalmjpjoreAinda não há avaliações

- Time Value of Money TVMDocumento48 páginasTime Value of Money TVMNikita KumariAinda não há avaliações

- Rift Valley University College of Business and Economics Department of Accounting and FinanceDocumento20 páginasRift Valley University College of Business and Economics Department of Accounting and FinanceYeabtsega FekaduAinda não há avaliações

- iSave-IPruMF FAQsDocumento6 páginasiSave-IPruMF FAQsMayur KhichiAinda não há avaliações

- MicrofinanceDocumento9 páginasMicrofinancesmartwebs100% (1)

- Corporate Brochure NewestDocumento20 páginasCorporate Brochure NewestSajan JoseAinda não há avaliações

- Financial Markets and Institutions 8th Edition by Frederic S Mishkin Ebook PDFDocumento42 páginasFinancial Markets and Institutions 8th Edition by Frederic S Mishkin Ebook PDFdon.anderson433100% (37)

- Mathematics of Investments: Simple Interest and Simple DiscountDocumento43 páginasMathematics of Investments: Simple Interest and Simple DiscountremelynAinda não há avaliações

- Auto Rickshaw - Business PlanDocumento28 páginasAuto Rickshaw - Business PlanAbhishek1881100% (1)

- Intacc 1 Notes Part 1Documento13 páginasIntacc 1 Notes Part 1Crizelda BauyonAinda não há avaliações

- Payfirma Ebook PaymentProcessing101Documento54 páginasPayfirma Ebook PaymentProcessing101Bruck FikreAinda não há avaliações

- Medical Student Loans - Ben WhiteDocumento129 páginasMedical Student Loans - Ben WhiteAndrew EricksonAinda não há avaliações

- Bret Broaddus Tips To Avoid Mistakes That Home Buyers MakeDocumento3 páginasBret Broaddus Tips To Avoid Mistakes That Home Buyers MakeBret broaddusAinda não há avaliações

- HDFC Bank - Wire Transfer DetailsDocumento2 páginasHDFC Bank - Wire Transfer Detailsanon_193130758Ainda não há avaliações

- SV90483973000 2023 06Documento11 páginasSV90483973000 2023 06Alina DinuAinda não há avaliações

- Gate Ies Psu: New Batches For Gate & Psus 2021Documento4 páginasGate Ies Psu: New Batches For Gate & Psus 2021Vijaykumar JatothAinda não há avaliações

- FA1 MOCK EXAM CHAPTER 1 To 5Documento6 páginasFA1 MOCK EXAM CHAPTER 1 To 5Haris AhnedAinda não há avaliações

- I.K. Gujral Punjab Technical University Jalandhar, KapurthalaDocumento3 páginasI.K. Gujral Punjab Technical University Jalandhar, Kapurthalaayush negiAinda não há avaliações

- Hayman July 07Documento5 páginasHayman July 07grumpyfeckerAinda não há avaliações

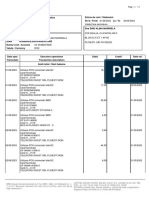

- Account Statement: Generated On Saturday, December 04, 2021 7:32:57 PMDocumento37 páginasAccount Statement: Generated On Saturday, December 04, 2021 7:32:57 PMdidiAinda não há avaliações

- Understanding RA 11057 and Its Effect With NCC and Prior LawsDocumento2 páginasUnderstanding RA 11057 and Its Effect With NCC and Prior LawsKym Algarme100% (2)

- Suncoast Bank StatementDocumento3 páginasSuncoast Bank StatementolaAinda não há avaliações

- Https Iiprd - MetavanteDocumento5 páginasHttps Iiprd - MetavanteShahab HussainAinda não há avaliações

- Resident To Nro Conversion FormDocumento3 páginasResident To Nro Conversion FormAbhiruchiAinda não há avaliações

- Implementation of Ghana Retail Payment Systems InfrastructureDocumento14 páginasImplementation of Ghana Retail Payment Systems InfrastructureGhanaWeb Editorial100% (1)

- Partner Contact MyDocumento25 páginasPartner Contact MySukri HasimAinda não há avaliações

- Introduction ToDocumento44 páginasIntroduction ToYash SoniAinda não há avaliações

- Dintle StatementDocumento3 páginasDintle StatementMANDLAAinda não há avaliações

- Senarai Permohonan Gaji-Lates 14.8.2020Documento104 páginasSenarai Permohonan Gaji-Lates 14.8.2020Aji Group Sdn BhdAinda não há avaliações

- CSS Forums - View Single Post - Posts For SBP Officers Grade-II Announced PDFDocumento5 páginasCSS Forums - View Single Post - Posts For SBP Officers Grade-II Announced PDFRahmatullah MardanviAinda não há avaliações