Você também pode gostar

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Uas Bahasa InggrisDocumento2 páginasUas Bahasa InggrisKiki AfridaAinda não há avaliações

- Igcse o Level Frankwoods Business Accounting 1 by Frank Wood Alan SangsterDocumento2 páginasIgcse o Level Frankwoods Business Accounting 1 by Frank Wood Alan SangsterNasir AliAinda não há avaliações

- Paysera Statement - 2023 08 21 - 23 22 12Documento1 páginaPaysera Statement - 2023 08 21 - 23 22 12Jovica CaricicAinda não há avaliações

- PLEDGELTR11711Documento1 páginaPLEDGELTR11711MarkYamaAinda não há avaliações

- Finman2 Quiz # 1 Summer Ay 10-11Documento2 páginasFinman2 Quiz # 1 Summer Ay 10-11Pierre Capati100% (1)

- Exam Routin of 96 Banking Deploma PDFDocumento1 páginaExam Routin of 96 Banking Deploma PDFMamunur RahmanAinda não há avaliações

- CTBC App-SignedDocumento2 páginasCTBC App-SignedLloyd MoloAinda não há avaliações

- WILL FormatDocumento3 páginasWILL FormatBrig. Baldev SinghAinda não há avaliações

- EFIN 519 Lecture 01Documento8 páginasEFIN 519 Lecture 01Irfan Sadique IsmamAinda não há avaliações

- FM ReportDocumento2 páginasFM Reportcaiden dumpAinda não há avaliações

- Ahmed Manzoor-Roll No 7-Class AssignmentDocumento7 páginasAhmed Manzoor-Roll No 7-Class AssignmentMansoor AhmedAinda não há avaliações

- Debhie Cesilia - 5213418072 - TugasDocumento6 páginasDebhie Cesilia - 5213418072 - TugasFenita Yuni PratiwiAinda não há avaliações

- 1.economics Material - Tamil (2022)Documento56 páginas1.economics Material - Tamil (2022)SowmiyaAinda não há avaliações

- Fortune Guarantee BrochureDocumento7 páginasFortune Guarantee BrochureGautamAinda não há avaliações

- Module 1Documento2 páginasModule 1Unknown Engr.Ainda não há avaliações

- 2024 28 2 19 11 02 Passbookstmt - 1709127662016Documento7 páginas2024 28 2 19 11 02 Passbookstmt - 1709127662016tuhincoregymAinda não há avaliações

- Introduction To Bankruptcy Law 6Th Edition Frey Test Bank Full Chapter PDFDocumento31 páginasIntroduction To Bankruptcy Law 6Th Edition Frey Test Bank Full Chapter PDFchastescurf7btc100% (10)

- Simple Interest AssignmentDocumento3 páginasSimple Interest AssignmentMaria Jessica AboAinda não há avaliações

- AYYUB KHAN VisionEndPlus 17.09.2019 17.30.29 PDFDocumento5 páginasAYYUB KHAN VisionEndPlus 17.09.2019 17.30.29 PDFgoluAinda não há avaliações

- Session 4 Life Insurance Products: Unit Linked PlansDocumento23 páginasSession 4 Life Insurance Products: Unit Linked Plansm_dattaiasAinda não há avaliações

- WEEK 1 - TVM and GrowthDocumento32 páginasWEEK 1 - TVM and GrowthowenAinda não há avaliações

- MPL FLEX Application Form2Documento3 páginasMPL FLEX Application Form2emmanuel cantones, jr.Ainda não há avaliações

- Jeevan Kishore T - 102Documento3 páginasJeevan Kishore T - 102lalithmohan100% (2)

- Chapter 3 Practice QuestionsDocumento10 páginasChapter 3 Practice QuestionshahaheheAinda não há avaliações

- Kairos LetterDocumento2 páginasKairos LettersebeastyforeverAinda não há avaliações

- Quiz 2 - Income Tax Concepts and ComplianceDocumento3 páginasQuiz 2 - Income Tax Concepts and CompliancelcAinda não há avaliações

- Benefit Illustration For HDFC Life Sanchay Par AdvantageDocumento3 páginasBenefit Illustration For HDFC Life Sanchay Par AdvantageLaviAinda não há avaliações

- Ai TGL TXNS List-2Documento11 páginasAi TGL TXNS List-2Abduselam TayeAinda não há avaliações

- Compound InterestDocumento19 páginasCompound InterestCASANDRA LascoAinda não há avaliações

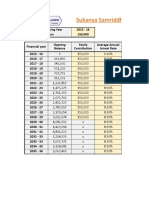

- Sukanya Samriddhi Yojana - CalculatorDocumento4 páginasSukanya Samriddhi Yojana - CalculatorIndiran100% (1)