Você também pode gostar

- 3-SIB Infy TemplateDocumento8 páginas3-SIB Infy TemplateKunal ChawlaAinda não há avaliações

- Cover Letter InternshipDocumento1 páginaCover Letter InternshipKunal ChawlaAinda não há avaliações

- Gst-Act: Goods and Services Tax. One Nation-One TaxDocumento63 páginasGst-Act: Goods and Services Tax. One Nation-One TaxKunal ChawlaAinda não há avaliações

- HPCL ValuationDocumento6 páginasHPCL ValuationKunal ChawlaAinda não há avaliações

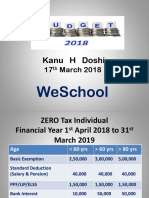

- Kanu H Doshi: 17 March 2018Documento16 páginasKanu H Doshi: 17 March 2018Kunal ChawlaAinda não há avaliações

- Presentation by - Hitaksha Gambhir - Archana Ramesh - Kushal Shah - Harshil Bhadra - Suyog KandiDocumento25 páginasPresentation by - Hitaksha Gambhir - Archana Ramesh - Kushal Shah - Harshil Bhadra - Suyog KandiKunal ChawlaAinda não há avaliações

- GCL PresentationDocumento18 páginasGCL PresentationKunal ChawlaAinda não há avaliações

- ﳷवदेश मं낰ालय भारत सरकार Ministry of External Affairs Government of India Online Appointment ReceiptDocumento3 páginasﳷवदेश मं낰ालय भारत सरकार Ministry of External Affairs Government of India Online Appointment ReceiptKunal ChawlaAinda não há avaliações

- Flare Case StudyDocumento9 páginasFlare Case StudySatish Kumar BurraAinda não há avaliações

- GCL PresentationDocumento18 páginasGCL PresentationKunal ChawlaAinda não há avaliações

- JJJDocumento5 páginasJJJKunal ChawlaAinda não há avaliações

- LeadsDocumento1 páginaLeadsKunal ChawlaAinda não há avaliações

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Chapter 04 Corporate GovernDocumento48 páginasChapter 04 Corporate GovernLiaAinda não há avaliações

- Making The Trend Your FriendDocumento4 páginasMaking The Trend Your FriendACasey101Ainda não há avaliações

- 3rd Sem Finance True and False - pdf112958630Documento28 páginas3rd Sem Finance True and False - pdf112958630Lee So Min100% (2)

- Kotak Mahindra BankDocumento47 páginasKotak Mahindra BankRazaali MukadamAinda não há avaliações

- Andhra Bank Account Opening FormDocumento2 páginasAndhra Bank Account Opening FormSanthosh Reddy BAinda não há avaliações

- Exposure To Currency Risk, Definition and MeasurementDocumento12 páginasExposure To Currency Risk, Definition and MeasurementGustavo Adolfo Leyva LópezAinda não há avaliações

- LT R Guidebook 053112Documento99 páginasLT R Guidebook 053112MarketsWikiAinda não há avaliações

- Caltex Vs COADocumento2 páginasCaltex Vs COAVladimir Sabarez LinawanAinda não há avaliações

- Introduction To: Forex TradingDocumento22 páginasIntroduction To: Forex TradingLESVIN SUGUMARANAinda não há avaliações

- What Are The Four Basic Areas of FinanceDocumento1 páginaWhat Are The Four Basic Areas of FinanceHaris Hafeez100% (5)

- CFA Level III in 2 Months - KonvexityDocumento6 páginasCFA Level III in 2 Months - Konvexityvishh8580Ainda não há avaliações

- Ra 7653Documento17 páginasRa 7653Sherna Adil100% (2)

- New Associate Checklist: Complete at OrientationDocumento20 páginasNew Associate Checklist: Complete at OrientationJeremyAinda não há avaliações

- Tradeoff Theory of Capital StructureDocumento10 páginasTradeoff Theory of Capital StructureSyed Peer Muhammad ShahAinda não há avaliações

- Motus GI Holdings, Inc.Documento142 páginasMotus GI Holdings, Inc.vicr100Ainda não há avaliações

- PSC 2013 Annual Report 17 A PSE For WebsiteDocumento157 páginasPSC 2013 Annual Report 17 A PSE For WebsitedendenliberoAinda não há avaliações

- Capital Structure - Perfect WorldDocumento37 páginasCapital Structure - Perfect Worldphilmore0% (1)

- Stock and Commodity MarketDocumento13 páginasStock and Commodity MarketEti Prince BajajAinda não há avaliações

- Beams10e Ch11Documento27 páginasBeams10e Ch11Leo Joko PurnomoAinda não há avaliações

- English Ratio Analysis For Real-Estate CompanyDocumento14 páginasEnglish Ratio Analysis For Real-Estate CompanyMohamad RizwanAinda não há avaliações

- FaxForm en UsDocumento1 páginaFaxForm en UsEjah ChyslcAinda não há avaliações

- PBU0054 Chapter 14 Financing SourcesDocumento36 páginasPBU0054 Chapter 14 Financing SourcesMUHAMMAD AQIL BIN KHAIRUL AZHARAinda não há avaliações

- Cryptocurrency - Taming The Volatility Through Fund-InvestingDocumento14 páginasCryptocurrency - Taming The Volatility Through Fund-InvestingPatrick Kiragu Mwangi BA, BSc., MA, ACSIAinda não há avaliações

- MOA of Actuarial Societ of BangladeshDocumento22 páginasMOA of Actuarial Societ of BangladeshActuarial Society of BangladeshAinda não há avaliações

- The Foreign Exchange Management ActDocumento19 páginasThe Foreign Exchange Management Actsaksham ahujaAinda não há avaliações

- PHILEX MINING Vs REYESDocumento2 páginasPHILEX MINING Vs REYESMariz GalangAinda não há avaliações

- Financial StatementDocumento17 páginasFinancial StatementNaveen AggarwalAinda não há avaliações

- 25soirepar PDFDocumento407 páginas25soirepar PDFAnonymous iLdSaAAinda não há avaliações

- Itc Limited: Corporate GovernanceDocumento7 páginasItc Limited: Corporate Governancekavitha kalasudhanAinda não há avaliações

- Ministry of Corporate Affairs - MCA ServicesDocumento2 páginasMinistry of Corporate Affairs - MCA ServicesMeiyappan MAinda não há avaliações