Você também pode gostar

- Debit Note in GST: (Goods and Services Tax)Documento2 páginasDebit Note in GST: (Goods and Services Tax)Jyothi Hari PrasadAinda não há avaliações

- GST Seminar Key HighlightsDocumento40 páginasGST Seminar Key HighlightsNavneetAinda não há avaliações

- debit or credit noteDocumento6 páginasdebit or credit noteamolisrivastava8Ainda não há avaliações

- Tax Invoice: SEC 34: Credit and Debit NotesDocumento4 páginasTax Invoice: SEC 34: Credit and Debit NotesManish K JadhavAinda não há avaliações

- Mahatma Education Society's Pillai College of Arts, Commerce and Science (Autonomous) New Panvel ISO 9001:2015 CertifiedDocumento17 páginasMahatma Education Society's Pillai College of Arts, Commerce and Science (Autonomous) New Panvel ISO 9001:2015 CertifiedAbizer KachwalaAinda não há avaliações

- Tax Invoice and Other Such Instruments: Central Board of Excise & CustomsDocumento4 páginasTax Invoice and Other Such Instruments: Central Board of Excise & CustomsAvinash DangwalAinda não há avaliações

- Tax Invoice and Other NewDocumento6 páginasTax Invoice and Other NewTax NatureAinda não há avaliações

- GST Invoice Rules, GST Tax Invoice, Download GST Invoice FormatDocumento6 páginasGST Invoice Rules, GST Tax Invoice, Download GST Invoice Formatiiftgscm batch2Ainda não há avaliações

- Unit 2:GST Procedures Topic: Credit and Debit NotesDocumento20 páginasUnit 2:GST Procedures Topic: Credit and Debit NotesManada SachdevaAinda não há avaliações

- 4 GST Time and Value of Supply NotesDocumento6 páginas4 GST Time and Value of Supply NotesMurali Krishnan RAinda não há avaliações

- Important GST Amendments in Budget 2023 - Taxguru - in PDFDocumento10 páginasImportant GST Amendments in Budget 2023 - Taxguru - in PDFPawan AswaniAinda não há avaliações

- GST declaration formDocumento1 páginaGST declaration formAnanta Engineering SolutionAinda não há avaliações

- Getting Invoicing in GST rightDocumento5 páginasGetting Invoicing in GST rightNivedita DodamaniAinda não há avaliações

- Tax Invoice, Credit and Debit Notes (Section 31-34 of CGST Act)Documento16 páginasTax Invoice, Credit and Debit Notes (Section 31-34 of CGST Act)Nikhil PahariaAinda não há avaliações

- VAT Tax ReportDocumento8 páginasVAT Tax ReportMichelle Marie TablizoAinda não há avaliações

- Cbec/gst/tax Invoice Efliers PDFDocumento8 páginasCbec/gst/tax Invoice Efliers PDFRenuka KhatkarAinda não há avaliações

- Credit Note and Debit Note Under GST - Masters IndiaDocumento5 páginasCredit Note and Debit Note Under GST - Masters Indiaarun alwaysAinda não há avaliações

- Credit Note - Zoho BooksDocumento4 páginasCredit Note - Zoho Booksarun alwaysAinda não há avaliações

- Girish GSTDocumento11 páginasGirish GSTAshiAinda não há avaliações

- Tax Invoice Under GSTDocumento3 páginasTax Invoice Under GSTkoushiki mishraAinda não há avaliações

- GST DocumentationDocumento32 páginasGST DocumentationTeju PawarAinda não há avaliações

- Income tax credit for April 15 deadlineDocumento2 páginasIncome tax credit for April 15 deadlinebrainAinda não há avaliações

- EY - GST News Alert: Executive SummaryDocumento6 páginasEY - GST News Alert: Executive SummaryAmit GargAinda não há avaliações

- Casual Taxable Person Brochure - 10 November 2022Documento2 páginasCasual Taxable Person Brochure - 10 November 2022KumariAinda não há avaliações

- B4-NOV-MSDocumento13 páginasB4-NOV-MSCerealis FelicianAinda não há avaliações

- BIR FORM NO. 2550Q - Quarterly Value-Added Tax Return Guidelines and InstructionsDocumento1 páginaBIR FORM NO. 2550Q - Quarterly Value-Added Tax Return Guidelines and InstructionsdreaAinda não há avaliações

- BIR FORM NO. 2550Q - Quarterly Value-Added Tax Return Guidelines and InstructionsDocumento1 páginaBIR FORM NO. 2550Q - Quarterly Value-Added Tax Return Guidelines and InstructionsdreaAinda não há avaliações

- BIR FORM NO. 2550Q - Quarterly Value-Added Tax Return Guidelines and InstructionsDocumento1 páginaBIR FORM NO. 2550Q - Quarterly Value-Added Tax Return Guidelines and InstructionsdreaAinda não há avaliações

- GST Weekly Update - 45 - 2023-24Documento5 páginasGST Weekly Update - 45 - 2023-24guptaharshit2204Ainda não há avaliações

- Atlas Consolidated Mining and Development Corporation vs. CIRDocumento54 páginasAtlas Consolidated Mining and Development Corporation vs. CIRChristian Adrian CepilloAinda não há avaliações

- Time of Supply of ServicesDocumento10 páginasTime of Supply of ServicesShiwang AgrawalAinda não há avaliações

- 6-GST - Declaration Form For GSTDocumento1 página6-GST - Declaration Form For GSTvishal.nithamAinda não há avaliações

- 46787bosfinal p8 Part1 Cp10Documento47 páginas46787bosfinal p8 Part1 Cp10virmani123Ainda não há avaliações

- TAX-304 (VAT Compliance Requirements)Documento5 páginasTAX-304 (VAT Compliance Requirements)Edith DalidaAinda não há avaliações

- Tax Brief August 2010Documento10 páginasTax Brief August 2010jae123Ainda não há avaliações

- GST 1 Maps Buyer132Documento1 páginaGST 1 Maps Buyer132MKTG THE SALEM AEROPARKAinda não há avaliações

- Tendernotice - 1 (3) 5Documento1 páginaTendernotice - 1 (3) 5SRARAinda não há avaliações

- S. 16: Eligibility & Conditions: Receipt of Document Forward Charge Cases (FCM)Documento3 páginasS. 16: Eligibility & Conditions: Receipt of Document Forward Charge Cases (FCM)MANU SHANKARAinda não há avaliações

- P&G Vs CIR - Vat RulingDocumento7 páginasP&G Vs CIR - Vat Rulingcaren kay b. adolfoAinda não há avaliações

- GST Annexure: Timely Provision of Invoices/debit Note/Credit Note/Other Applicable DocumentsDocumento3 páginasGST Annexure: Timely Provision of Invoices/debit Note/Credit Note/Other Applicable Documentsshuklaankit704_24016Ainda não há avaliações

- Revenue and Expense Recognition ReviewDocumento7 páginasRevenue and Expense Recognition ReviewPaupauAinda não há avaliações

- GST Advance ReceiptsDocumento4 páginasGST Advance ReceiptsmanukleoAinda não há avaliações

- Atlas Consolidated Mining vs. CIRDocumento51 páginasAtlas Consolidated Mining vs. CIRCamille Yasmeen SamsonAinda não há avaliações

- Draft Invoice RulesDocumento6 páginasDraft Invoice RulesSandeep KaundinyaAinda não há avaliações

- VAT Refund Audit ProgramDocumento5 páginasVAT Refund Audit ProgramCha Gamboa De LeonAinda não há avaliações

- REMEDIES by J. DimaampaoDocumento2 páginasREMEDIES by J. DimaampaoJeninah Arriola CalimlimAinda não há avaliações

- CA Ashish Chaudhary 1Documento30 páginasCA Ashish Chaudhary 1sonapakhi nandyAinda não há avaliações

- 03 - Claims For Excise Tax Refund InquiryDocumento5 páginas03 - Claims For Excise Tax Refund InquiryAhyz DyAinda não há avaliações

- GST - Tax Invoice, Debit or Credit Notes, Returns, Payment of Tax PDFDocumento78 páginasGST - Tax Invoice, Debit or Credit Notes, Returns, Payment of Tax PDFSapna MalikAinda não há avaliações

- Reverse Charge MechanismDocumento3 páginasReverse Charge MechanismARJUNAinda não há avaliações

- Fate of "Unjust Enrichment" Principle Under GSTDocumento2 páginasFate of "Unjust Enrichment" Principle Under GSTRajula Gurva ReddyAinda não há avaliações

- Tax InvoiceDocumento52 páginasTax InvoicesidhantAinda não há avaliações

- Tax Deductions for Professional Fees Under Accrual MethodDocumento2 páginasTax Deductions for Professional Fees Under Accrual MethodRenmarc JuangcoAinda não há avaliações

- 56454bosinter p4 Maynov2020secb cp8Documento68 páginas56454bosinter p4 Maynov2020secb cp8Vijesh SoniAinda não há avaliações

- Withholding VAT Guideline (2017-18)Documento29 páginasWithholding VAT Guideline (2017-18)banglauserAinda não há avaliações

- Deductions From Gross Income 2Documento3 páginasDeductions From Gross Income 2Pilyang SweetAinda não há avaliações

- Revisiting The Rules On Claiming Withholding Tax CreditsDocumento3 páginasRevisiting The Rules On Claiming Withholding Tax Creditsarnelo sarmientoAinda não há avaliações

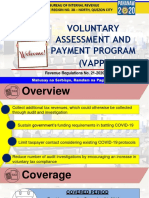

- Voluntary Assessment and Payment Program (VAPP) : Bureau of Internal Revenue Revenue Region No. 38 - North, Quezon CityDocumento29 páginasVoluntary Assessment and Payment Program (VAPP) : Bureau of Internal Revenue Revenue Region No. 38 - North, Quezon CityEdward GanAinda não há avaliações

- BIR Form 2550M - Monthly Value-Added Tax Declaration Guidelines and InstructionsDocumento1 páginaBIR Form 2550M - Monthly Value-Added Tax Declaration Guidelines and InstructionsdreaAinda não há avaliações

- The Contractor Payment Application Audit: Guidance for Auditing AIA Documents G702 & G703No EverandThe Contractor Payment Application Audit: Guidance for Auditing AIA Documents G702 & G703Ainda não há avaliações

- On Submission of SFT in Form 61A PDFDocumento36 páginasOn Submission of SFT in Form 61A PDFajinkya ghevadeAinda não há avaliações

- List of Services Under Reverse ChargeDocumento5 páginasList of Services Under Reverse ChargeMoneycontrol News100% (18)

- GST Expanse RateDocumento2 páginasGST Expanse RateSneha AgarwalAinda não há avaliações

- Draft Return Formats 26092016 PDFDocumento129 páginasDraft Return Formats 26092016 PDFBharatAinda não há avaliações

- Faq MiningDocumento10 páginasFaq MiningSneha AgarwalAinda não há avaliações

- GST Accounts & RecordsDocumento12 páginasGST Accounts & RecordsSneha AgarwalAinda não há avaliações

- GST FAQs on Handicraft SectorDocumento6 páginasGST FAQs on Handicraft SectorSneha AgarwalAinda não há avaliações

- ICDS - Trading DisclosuresDocumento3 páginasICDS - Trading DisclosuresSneha AgarwalAinda não há avaliações

- E Book On How To Get Registered Under GST 1aug2017Documento132 páginasE Book On How To Get Registered Under GST 1aug2017Sneha AgarwalAinda não há avaliações

- Annotation RubricDocumento5 páginasAnnotation RubriclearnerivanAinda não há avaliações

- Read President Trump's Fiscal Year 2019 BudgetDocumento160 páginasRead President Trump's Fiscal Year 2019 Budgetkballuck1100% (6)

- GST Revision (Marathon) Notes-May'24Documento89 páginasGST Revision (Marathon) Notes-May'24AmruthaAinda não há avaliações

- PPE Costs and ExchangesDocumento2 páginasPPE Costs and ExchangesRex AdarmeAinda não há avaliações

- Report On Financial Reporting PDFFFDocumento38 páginasReport On Financial Reporting PDFFFMohit AroraAinda não há avaliações

- Chevron PH Vs Commissioner of BOCDocumento4 páginasChevron PH Vs Commissioner of BOCTenet Manzano100% (1)

- BBC AudienceDocumento138 páginasBBC AudienceporukeslikeAinda não há avaliações

- Employment Income - Derivation, Exemptions, Types and DeductionsDocumento57 páginasEmployment Income - Derivation, Exemptions, Types and DeductionsTeh Chu Leong100% (1)

- Macro Economic Trends of Sri LankaDocumento13 páginasMacro Economic Trends of Sri LankathilangacAinda não há avaliações

- Lesson 15: TaxationDocumento2 páginasLesson 15: TaxationMa. Luisa RenidoAinda não há avaliações

- Coursera University of Melbourne Macro Economics Course Peer Assessment AssignmentDocumento7 páginasCoursera University of Melbourne Macro Economics Course Peer Assessment AssignmentpsstquestionAinda não há avaliações

- Milestone 1Documento11 páginasMilestone 1Nandish Patel100% (1)

- MayaCredit SoA 2023SEPDocumento3 páginasMayaCredit SoA 2023SEPjepoy palaruanAinda não há avaliações

- Taco 0088166061500044Documento1 páginaTaco 0088166061500044Sourav ChakrabortyAinda não há avaliações

- 11 Biggest Challenges of International BusinessDocumento8 páginas11 Biggest Challenges of International BusinesspranshuAinda não há avaliações

- Tata Dealership Form and RequirementsDocumento21 páginasTata Dealership Form and Requirementskrishnaaul100% (1)

- Estate Planning & Administration OutlineDocumento9 páginasEstate Planning & Administration OutlineSean Robertson100% (1)

- RMC No. 73-2018Documento3 páginasRMC No. 73-2018Madi KomoaAinda não há avaliações

- Bir Rao 01 03Documento3 páginasBir Rao 01 03Benedict Jonathan BermudezAinda não há avaliações

- The Effects of Education On CrimeDocumento12 páginasThe Effects of Education On CrimeMicaela FORSCHBERG CASTORINOAinda não há avaliações

- Risk Analysis ExampleDocumento8 páginasRisk Analysis ExampleRyan SooknarineAinda não há avaliações

- Cooperative Code of The PhilippinesDocumento16 páginasCooperative Code of The PhilippinesJeean BeldaAinda não há avaliações

- Patterns of Philippine ExpendituresDocumento13 páginasPatterns of Philippine ExpendituresTrisha AlmonteAinda não há avaliações

- TrustDocumento91 páginasTrustmohiuddinduo593% (14)

- 3Documento26 páginas3JDAinda não há avaliações

- Constitution of India, 1949 - Bare Acts - Law Library - AdvocateKhojDocumento12 páginasConstitution of India, 1949 - Bare Acts - Law Library - AdvocateKhojAmitKumar100% (1)

- Tax Planning With Reference To Managerial DecisionsDocumento22 páginasTax Planning With Reference To Managerial DecisionsdharuvAinda não há avaliações

- Lec 3 SalaryDocumento28 páginasLec 3 SalaryManasi PatilAinda não há avaliações

- Lass 12 Subject Economics Paper Set 1 With Solutions: (Macro Economics) Question 1: (Marks 1)Documento10 páginasLass 12 Subject Economics Paper Set 1 With Solutions: (Macro Economics) Question 1: (Marks 1)sandeep11116Ainda não há avaliações

- Correcting Erroneous Information Returns, Form #04.001Documento144 páginasCorrecting Erroneous Information Returns, Form #04.001Sovereignty Education and Defense Ministry (SEDM)50% (2)