Você também pode gostar

- Financial Accounting 2Documento89 páginasFinancial Accounting 2Colince johnson0% (1)

- 2022 - 05 - Bad and Doubtful DebtsDocumento39 páginas2022 - 05 - Bad and Doubtful DebtsSafi UllahAinda não há avaliações

- Chapter 8 - Receivables Lecture Notes - StudentsDocumento43 páginasChapter 8 - Receivables Lecture Notes - StudentsKy Anh NguyễnAinda não há avaliações

- SOF Questions - With - AnswersDocumento33 páginasSOF Questions - With - AnswersКамиль БайбуринAinda não há avaliações

- Reviewer in Abc Costing: Cost Accounting AND Control (B. Activity-Based Cost System)Documento14 páginasReviewer in Abc Costing: Cost Accounting AND Control (B. Activity-Based Cost System)justine reine cornicoAinda não há avaliações

- CH 6 Classpack With SolutionsDocumento20 páginasCH 6 Classpack With SolutionsjimenaAinda não há avaliações

- Chapter 11 Testbank QuestionsDocumento34 páginasChapter 11 Testbank QuestionsFami FamzAinda não há avaliações

- Chapter 4 Analysis of Financial StatementsDocumento2 páginasChapter 4 Analysis of Financial StatementsSamantha Siau100% (1)

- ch17 Investment PDFDocumento21 páginasch17 Investment PDFJoan Marah Langit JovesAinda não há avaliações

- Debt Securities PDFDocumento7 páginasDebt Securities PDFChin-Chin Alvarez SabinianoAinda não há avaliações

- Chap2 PDFDocumento50 páginasChap2 PDFKhalid AhmedAinda não há avaliações

- ACCT233 Midterm Exam Multichoice QuestionsDocumento7 páginasACCT233 Midterm Exam Multichoice QuestionsDominic Robinson0% (1)

- International Business Chapter 16 Exporting, Importing and Countertrade SummaryDocumento19 páginasInternational Business Chapter 16 Exporting, Importing and Countertrade Summarywasiul hoqueAinda não há avaliações

- Ifrs 13 Fair Value MeasurementDocumento9 páginasIfrs 13 Fair Value Measurementapi-292644739Ainda não há avaliações

- Chapter 1 BrighamDocumento18 páginasChapter 1 BrighamJude GuzmanAinda não há avaliações

- Accounting Textbook Solutions - 35Documento19 páginasAccounting Textbook Solutions - 35acc-expertAinda não há avaliações

- Why Are Ratios UsefulDocumento11 páginasWhy Are Ratios UsefulKriza Sevilla Matro100% (3)

- IAS-37 Provisions, Contingent Liabilities and Assets SummaryDocumento29 páginasIAS-37 Provisions, Contingent Liabilities and Assets SummaryAbdul SamiAinda não há avaliações

- Calculating Incremental ROIC's: Corner of Berkshire & Fairfax - NYC Meetup October 14, 2017Documento19 páginasCalculating Incremental ROIC's: Corner of Berkshire & Fairfax - NYC Meetup October 14, 2017Anil GowdaAinda não há avaliações

- JPIA Financial Accounting 1 (Prelims)Documento20 páginasJPIA Financial Accounting 1 (Prelims)Kristienalyn De AsisAinda não há avaliações

- Chapter 27 Leases (Student)Documento29 páginasChapter 27 Leases (Student)Kelvin Chu JYAinda não há avaliações

- MAS Practice GuideDocumento4 páginasMAS Practice GuideDivine CuasayAinda não há avaliações

- MiniscribeDocumento14 páginasMiniscribeImadAinda não há avaliações

- Test Bank Ch6 ACCTDocumento89 páginasTest Bank Ch6 ACCTMajed100% (1)

- An Information Systems FrameworkDocumento30 páginasAn Information Systems FrameworkDr. Mohammad Noor AlamAinda não há avaliações

- Debt RatioDocumento7 páginasDebt RatioAamir BilalAinda não há avaliações

- Concept Map (Garcia, Plata, Villamin) PDFDocumento6 páginasConcept Map (Garcia, Plata, Villamin) PDFMinji OhAinda não há avaliações

- Answer FIN 081 P1 - C1Documento4 páginasAnswer FIN 081 P1 - C1marvinAinda não há avaliações

- Receivable Management KanchanDocumento12 páginasReceivable Management KanchanSanchita NaikAinda não há avaliações

- Strategic Cost Management Chap007Documento49 páginasStrategic Cost Management Chap007Arini Thiyasza50% (2)

- FIN 515 Midterm ExamDocumento4 páginasFIN 515 Midterm ExamDeVryHelpAinda não há avaliações

- CompExam D AcceptedDocumento10 páginasCompExam D Acceptedrahul shahAinda não há avaliações

- Porter Fuve Analysis by Jpmorgan ChaseDocumento3 páginasPorter Fuve Analysis by Jpmorgan Chaseekta kriplaniAinda não há avaliações

- MAS 7 Exercises For UploadDocumento9 páginasMAS 7 Exercises For UploadChristine Joy Duterte RemorozaAinda não há avaliações

- Practice Exam 1gdfgdfDocumento49 páginasPractice Exam 1gdfgdfredearth2929100% (1)

- Final Exam: Fall 1997 This Exam Is Worth 30% and You Have 2 HoursDocumento84 páginasFinal Exam: Fall 1997 This Exam Is Worth 30% and You Have 2 HoursJatin PanchiAinda não há avaliações

- Theory of Working Capital ManagementDocumento16 páginasTheory of Working Capital Managementaffamijazi81% (16)

- Additional topics in variance analysisDocumento33 páginasAdditional topics in variance analysisAnthony MaloneAinda não há avaliações

- Auditing Problems Review: Key Equity and Bond CalculationsDocumento2 páginasAuditing Problems Review: Key Equity and Bond CalculationsgbenjielizonAinda não há avaliações

- Long Term Fin v3Documento56 páginasLong Term Fin v3Mark christianAinda não há avaliações

- Preliminary Judgement About MaterialityDocumento1 páginaPreliminary Judgement About MaterialityYanna Bacosa100% (1)

- Calculate Materiality: Assignment 2Documento3 páginasCalculate Materiality: Assignment 2ge baijingAinda não há avaliações

- Geometric Mean Applications in FinanceDocumento5 páginasGeometric Mean Applications in FinanceCalvin E. AmosAinda não há avaliações

- Ms14e Case Chapter 03 FinalDocumento10 páginasMs14e Case Chapter 03 FinalOfelia Ragpa100% (1)

- Cash and RecDocumento30 páginasCash and RecChiara OlivoAinda não há avaliações

- Chapter Five Decision Making and Relevant Information Information and The Decision ProcessDocumento10 páginasChapter Five Decision Making and Relevant Information Information and The Decision ProcesskirosAinda não há avaliações

- Contemporary Strategy Analysis Ch1Documento3 páginasContemporary Strategy Analysis Ch1Beta AccAinda não há avaliações

- Chapter 16 QuizDocumento3 páginasChapter 16 Quizbeckkl05Ainda não há avaliações

- ABC 01 Accounting For Business Combination 20230123121552Documento18 páginasABC 01 Accounting For Business Combination 20230123121552Joshuji LaneAinda não há avaliações

- Scanner CAP II Financial ManagementDocumento195 páginasScanner CAP II Financial ManagementEdtech NepalAinda não há avaliações

- ACCO30053-AACA1 Final-Examination 1st-Semester AY2021-2022 QUESTIONNAIREDocumento12 páginasACCO30053-AACA1 Final-Examination 1st-Semester AY2021-2022 QUESTIONNAIREKabalaAinda não há avaliações

- K17405CA Assignment Kim Huong and Nhu ThuanDocumento25 páginasK17405CA Assignment Kim Huong and Nhu Thuanthuylinh voAinda não há avaliações

- Intermediate Accounting - Final Output ReceivablesDocumento56 páginasIntermediate Accounting - Final Output ReceivablesAnitas LimmaumAinda não há avaliações

- CH 12Documento63 páginasCH 12Grace VersoniAinda não há avaliações

- ExamView - Homework CH 4Documento9 páginasExamView - Homework CH 4Brooke LevertonAinda não há avaliações

- FM - Cost of CapitalDocumento26 páginasFM - Cost of CapitalMaxine SantosAinda não há avaliações

- Puzzle of The Cash Flow StatementDocumento8 páginasPuzzle of The Cash Flow Statementqwertycvc0% (1)

- Economic and Political Weekly Economic and Political WeeklyDocumento10 páginasEconomic and Political Weekly Economic and Political WeeklyWILDER ENRIQUEZ POCOMOAinda não há avaliações

- SPECIALIZED FABM2 Module 06 Week 06 - Statement of Cash FlowDocumento11 páginasSPECIALIZED FABM2 Module 06 Week 06 - Statement of Cash Flowlams.ronaldsunigaAinda não há avaliações

- Accounting in A Nutshell 5: The Cash Flow StatementDocumento3 páginasAccounting in A Nutshell 5: The Cash Flow StatementBusiness Expert PressAinda não há avaliações

- AURA (Ritu)Documento2 páginasAURA (Ritu)Praneta ShuklaAinda não há avaliações

- MRPDocumento16 páginasMRPPraneta ShuklaAinda não há avaliações

- Atharva 10Documento2 páginasAtharva 10Praneta ShuklaAinda não há avaliações

- Solving The Puzzle of The Cash Flow StatementDocumento8 páginasSolving The Puzzle of The Cash Flow StatementPraneta ShuklaAinda não há avaliações

- ASE20104 - Mark Scheme - November 2018Documento18 páginasASE20104 - Mark Scheme - November 2018Aung Zaw Htwe100% (3)

- Project On Tax AuditDocumento125 páginasProject On Tax Auditglorydharmaraj100% (1)

- Ce Investing in Ce 2014 PDFDocumento132 páginasCe Investing in Ce 2014 PDFSomnath DasguptaAinda não há avaliações

- Contract of Lease FormDocumento3 páginasContract of Lease FormHal JordanAinda não há avaliações

- The Act Borrowers Guide To Lma Loan Documentation For Investment Grade Borrowers June 2014 SupplementDocumento20 páginasThe Act Borrowers Guide To Lma Loan Documentation For Investment Grade Borrowers June 2014 SupplementkamisyedAinda não há avaliações

- TCS Form 9 Fresher Sample FormDocumento1 páginaTCS Form 9 Fresher Sample FormPiyush Ranjan100% (4)

- BIR Ruling DA-141-99Documento3 páginasBIR Ruling DA-141-99racheltanuy6557100% (1)

- FIN202 Midterm ExerciseDocumento13 páginasFIN202 Midterm Exerciseyeeeeeqi100% (1)

- Cost Sheet FormatDocumento5 páginasCost Sheet Formatvicky3230Ainda não há avaliações

- Philippine Accounting StandardsDocumento4 páginasPhilippine Accounting StandardsEdDeTorresValino50% (2)

- Property Law PRODocumento14 páginasProperty Law PROgowthamAinda não há avaliações

- POLAND'S A2 Motorway - FinalDocumento12 páginasPOLAND'S A2 Motorway - FinalAbinash Behera100% (2)

- Demystifying Economic Terms With Maggu-Bhai Volume 22 (June)Documento10 páginasDemystifying Economic Terms With Maggu-Bhai Volume 22 (June)Mana Planet100% (1)

- Direct Tax Rates For Last 11 Assessment YearsDocumento4 páginasDirect Tax Rates For Last 11 Assessment YearsValera HardikAinda não há avaliações

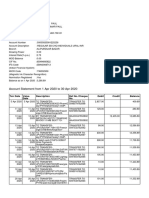

- Account Statement From 1 Apr 2020 To 30 Apr 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocumento2 páginasAccount Statement From 1 Apr 2020 To 30 Apr 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceSubham PaulAinda não há avaliações

- Sample Complaint Letter Bank Fees IIDocumento2 páginasSample Complaint Letter Bank Fees IIRoshan Khan100% (1)

- Recruitment Agency AgreementDocumento3 páginasRecruitment Agency AgreementratyuAinda não há avaliações

- SARFESI Act Enforcement ProceduresDocumento56 páginasSARFESI Act Enforcement ProcedureskannangksAinda não há avaliações

- Decentralized Operations and Segment Reporting AnalysisDocumento130 páginasDecentralized Operations and Segment Reporting AnalysisAilene QuintoAinda não há avaliações

- FM Unit 5Documento14 páginasFM Unit 5Rizwana BegumAinda não há avaliações

- RL R.% - R. N : Rga, A/"Documento4 páginasRL R.% - R. N : Rga, A/"Vince De GuzmanAinda não há avaliações

- Amalda Aulia 1810533004 Int - AccountingDocumento11 páginasAmalda Aulia 1810533004 Int - AccountingAmalda AuliaAinda não há avaliações

- CH 05Documento25 páginasCH 05Ahmed Al EkamAinda não há avaliações

- Beams - Intercom Profit Transaction - BondsDocumento12 páginasBeams - Intercom Profit Transaction - BondsAnggit Ponco100% (1)

- Computation 19-20Documento2 páginasComputation 19-20madali sivareddyAinda não há avaliações

- Venture Capital Deal Structuring PDFDocumento5 páginasVenture Capital Deal Structuring PDFmonaAinda não há avaliações

- Ind As Implementation GuideDocumento176 páginasInd As Implementation Guidevramu_caAinda não há avaliações

- Aim Student Loan Application FormDocumento3 páginasAim Student Loan Application FormCharles de belenAinda não há avaliações

- Income Tax Act Section 22Documento25 páginasIncome Tax Act Section 22Harkiran Brar100% (2)

- Sps. Mariano Z. Velarde & Avelina D. Velarde V. Ca, David A. Raymundo, & George Raymundo (Velarde V. Ca) FactsDocumento3 páginasSps. Mariano Z. Velarde & Avelina D. Velarde V. Ca, David A. Raymundo, & George Raymundo (Velarde V. Ca) Factstink echivereAinda não há avaliações