Você também pode gostar

- Business Model Canvas Poster-DikonversiDocumento1 páginaBusiness Model Canvas Poster-DikonversiHana NatashamuraAinda não há avaliações

- Lakshmi Vilas Bank Initiating Coverage Dec 2015Documento14 páginasLakshmi Vilas Bank Initiating Coverage Dec 2015janmAinda não há avaliações

- Jawa Bali 500kV Grid ConfigurationDocumento205 páginasJawa Bali 500kV Grid ConfigurationekaAinda não há avaliações

- (Aiims Awantipora) Kashmir: All India Institute of Medical SciencesDocumento1 página(Aiims Awantipora) Kashmir: All India Institute of Medical SciencesAbilaash VelumaniAinda não há avaliações

- First Floor: Statue of OnenessDocumento1 páginaFirst Floor: Statue of OnenessSufyan AhmadAinda não há avaliações

- BU 2 - Organization ChartDocumento1 páginaBU 2 - Organization ChartMohammed ShebinAinda não há avaliações

- Hse Traning Need Analisys 2018: Course CodeDocumento7 páginasHse Traning Need Analisys 2018: Course Coderifki bahtiarAinda não há avaliações

- 34 AVANZA (Cont' D) (Cont. Next Page) : Engine Control (From Aug. 2015 Production)Documento1 página34 AVANZA (Cont' D) (Cont. Next Page) : Engine Control (From Aug. 2015 Production)José LuisAinda não há avaliações

- PVI-5000 - 6000-TL-OUTD-Quick Installation Guide EN-RevE PDFDocumento2 páginasPVI-5000 - 6000-TL-OUTD-Quick Installation Guide EN-RevE PDFSampath KumarAinda não há avaliações

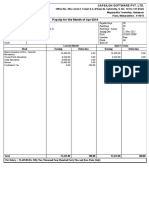

- PayslipDocumento1 páginaPayslipCA Manish BalaniAinda não há avaliações

- 2232 - dd2002 (p6) - Overall Floor PlanDocumento1 página2232 - dd2002 (p6) - Overall Floor PlanAndrew Lymn-PenningAinda não há avaliações

- S5-02 - Concrete Sections and DetailsDocumento1 páginaS5-02 - Concrete Sections and DetailsJason toraldeAinda não há avaliações

- 0452020-A-PP001.GWG (2) - Layout1Documento1 página0452020-A-PP001.GWG (2) - Layout1Yulian PolaniaAinda não há avaliações

- TOPOGRAFICO 2021 Actualizado 3 lotes-LOTIZACION 20-21-22Documento1 páginaTOPOGRAFICO 2021 Actualizado 3 lotes-LOTIZACION 20-21-22Charly Alcantara RodriguezAinda não há avaliações

- The Basic Balanced Scorecard TemplateDocumento2 páginasThe Basic Balanced Scorecard TemplateomzoerAinda não há avaliações

- Monthly Salary Statement for Giddalur BranchDocumento1 páginaMonthly Salary Statement for Giddalur Branchjabbar_irpmAinda não há avaliações

- Struktur Harvesting Per 18 Nov 2021 (Target Kiriman 10000 Ton)Documento7 páginasStruktur Harvesting Per 18 Nov 2021 (Target Kiriman 10000 Ton)Eshika PrawitasariAinda não há avaliações

- Peta Batas Ancak Afd 1 Juni-1Documento1 páginaPeta Batas Ancak Afd 1 Juni-1Muhammad Gus Razaki NstAinda não há avaliações

- 0719 Final PDFDocumento38 páginas0719 Final PDFJamie HughesAinda não há avaliações

- Proyecto 02 Localizacion y UbicacionDocumento1 páginaProyecto 02 Localizacion y UbicacionAnonymous 3Fk89WYAinda não há avaliações

- Cup-1 Cup-2 Cup-3 Cup-4 Cup-5 Cup-6 Cup-7 Cup-8 Cup-9: Cup-9 Cup-1 Cup-2 Cup-3 Cup-4 Cup-5 Cup-6 Cup-7 Cup-8Documento1 páginaCup-1 Cup-2 Cup-3 Cup-4 Cup-5 Cup-6 Cup-7 Cup-8 Cup-9: Cup-9 Cup-1 Cup-2 Cup-3 Cup-4 Cup-5 Cup-6 Cup-7 Cup-8Wongsatorn W.Ainda não há avaliações

- Structural Notes: Seaoil Filling StationDocumento1 páginaStructural Notes: Seaoil Filling StationCasmir TayagAinda não há avaliações

- BrainstomingDocumento1 páginaBrainstomingrohitthestar2003Ainda não há avaliações

- National Minimum Wage 2021Documento5 páginasNational Minimum Wage 2021CityPress0% (1)

- History and global expansion of leading LED signal manufacturer PATLITEDocumento2 páginasHistory and global expansion of leading LED signal manufacturer PATLITECamelia Petrescu100% (1)

- PKPK - Annual Report - 2015Documento42 páginasPKPK - Annual Report - 2015kun henderyAinda não há avaliações

- Datacenter Indonesia Karawang International Industrial City (KIIC) West Java Shop Drawing Review Status Approved with noteDocumento1 páginaDatacenter Indonesia Karawang International Industrial City (KIIC) West Java Shop Drawing Review Status Approved with notePhạm Quốc ViệtAinda não há avaliações

- WBHO Training Matrix 24.02.2020Documento1 páginaWBHO Training Matrix 24.02.2020Edson Mauro Thomas NobregaAinda não há avaliações

- 4TH Floor Low Zone Elev Lobby RCPDocumento1 página4TH Floor Low Zone Elev Lobby RCPArsenic DiacajoAinda não há avaliações

- Mars3 Tech 600-12000 20200805Documento6 páginasMars3 Tech 600-12000 20200805Daniel Lack PendásAinda não há avaliações

- Company ProfileDocumento4 páginasCompany ProfileMareks LezevskisAinda não há avaliações

- Deloitte Wireless Industry Value MapDocumento1 páginaDeloitte Wireless Industry Value MapDiogo Pimenta Barreiros0% (1)

- Lifting clearance and maintenance details for electric motorDocumento1 páginaLifting clearance and maintenance details for electric motorMD.Habibur RhamanAinda não há avaliações

- ISO 9001 and AQAP 160 Project Management StandardsDocumento14 páginasISO 9001 and AQAP 160 Project Management StandardsBahadır Harmancı0% (1)

- Sunday 7-11-Model - PDF Sara 1Documento1 páginaSunday 7-11-Model - PDF Sara 1Mariam Mohamed Abdo Morsy GhanemAinda não há avaliações

- Chart - Poster - PMBOK 6th Ed Data Flow DiagramDocumento1 páginaChart - Poster - PMBOK 6th Ed Data Flow DiagramPatelVKAinda não há avaliações

- Cityscape Global FloorplanDocumento1 páginaCityscape Global FloorplanregallydivineAinda não há avaliações

- LBP A3 Example Office Case StudyDocumento1 páginaLBP A3 Example Office Case StudyOsvaldo ColinAinda não há avaliações

- Estructural 1Documento1 páginaEstructural 1Sarahii RamosAinda não há avaliações

- PVI 6000 TL OUTD W Quick Installation Guide en RevADocumento2 páginasPVI 6000 TL OUTD W Quick Installation Guide en RevA王伯恩Ainda não há avaliações

- B Clave Agua Mucuro Layout1Documento1 páginaB Clave Agua Mucuro Layout1eeeAinda não há avaliações

- Iplp No: IPLP2020/DTCP-ONUDA/MRKP/000010 Ulb: Markapur Municipality Development Authority: Onuda District: PrakasamDocumento1 páginaIplp No: IPLP2020/DTCP-ONUDA/MRKP/000010 Ulb: Markapur Municipality Development Authority: Onuda District: PrakasamLakshmi LuckeyAinda não há avaliações

- RACI TemplateDocumento8 páginasRACI TemplateVanitha raoAinda não há avaliações

- SSP X Ssps Stp1 Dads Arc Lap 031223 x00cDocumento1 páginaSSP X Ssps Stp1 Dads Arc Lap 031223 x00cbadeAinda não há avaliações

- Map of The DecadeDocumento2 páginasMap of The Decadej.vanderveen100% (1)

- Swiss-Belhotel Darmo Project ManagementDocumento108 páginasSwiss-Belhotel Darmo Project ManagementRulyAinda não há avaliações

- Lamina Agua Potable 1 de 2Documento1 páginaLamina Agua Potable 1 de 2Luis ReyesAinda não há avaliações

- 093 2018 0702 WBK JV TPPD F100Documento1 página093 2018 0702 WBK JV TPPD F100陈耀Ainda não há avaliações

- 0000gf Also AsloaDocumento1 página0000gf Also AsloaAhmadjakwarAinda não há avaliações

- A2-123 Level 62 and Level 63 Floor PlanDocumento1 páginaA2-123 Level 62 and Level 63 Floor PlanRyan BacalaAinda não há avaliações

- Ohio OAKS comparison of organization functions with ITIL servicesDocumento3 páginasOhio OAKS comparison of organization functions with ITIL servicesroddickersonAinda não há avaliações

- Detailed Design 16 MAY 2022: Mandai Rainforest Park North SingaporeDocumento12 páginasDetailed Design 16 MAY 2022: Mandai Rainforest Park North SingaporeJawAinda não há avaliações

- Caterpillar 3126 PlanoDocumento2 páginasCaterpillar 3126 PlanoManuel Nicolas Sanchez100% (1)

- Makassar 1: Total Target OptimisDocumento2 páginasMakassar 1: Total Target OptimisAchaElmanAinda não há avaliações

- Star Treatment: Tranquility Base Hotel + CasinoDocumento4 páginasStar Treatment: Tranquility Base Hotel + CasinoHélène TeychenéAinda não há avaliações

- STAKING OUTDocumento1 páginaSTAKING OUTRido faturahmanAinda não há avaliações

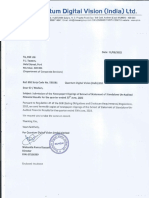

- @ Quantum Digital Vision (India) LTD.: To, BSE Ltd. P.J. Towers, Dalal Street, Fort Mumbai-400 001Documento3 páginas@ Quantum Digital Vision (India) LTD.: To, BSE Ltd. P.J. Towers, Dalal Street, Fort Mumbai-400 001Krishna Raj KAinda não há avaliações

- ST02 - FOUNDATION-Layout1Documento1 páginaST02 - FOUNDATION-Layout1Fazil RizhafAinda não há avaliações

- A2-124 Level 64 and Level 65 Floor PlanDocumento1 páginaA2-124 Level 64 and Level 65 Floor PlanRyan BacalaAinda não há avaliações

- Math Workshop, Grade 1: A Framework for Guided Math and Independent PracticeNo EverandMath Workshop, Grade 1: A Framework for Guided Math and Independent PracticeAinda não há avaliações

- Ambit Strategy 10 Minute Flipbook 23jan2024Documento17 páginasAmbit Strategy 10 Minute Flipbook 23jan2024bharat005Ainda não há avaliações

- Mage SystemDocumento290 páginasMage Systemdevulsky-1100% (17)

- GMO Equity Dislocation Strategy Review - 8-21Documento4 páginasGMO Equity Dislocation Strategy Review - 8-21bharat005Ainda não há avaliações

- PaperDocumento18 páginasPaperbharat005Ainda não há avaliações

- Zensar Technologies: Enabling Digital TransformationDocumento36 páginasZensar Technologies: Enabling Digital Transformationbharat005Ainda não há avaliações

- ExtractAlpha New Constructs White PaperDocumento11 páginasExtractAlpha New Constructs White Paperbharat005Ainda não há avaliações

- Mage SystemDocumento290 páginasMage Systemdevulsky-1100% (17)

- Population Projections for India and States 2011-2036Documento270 páginasPopulation Projections for India and States 2011-2036bharat005Ainda não há avaliações

- ExtractAlpha New Constructs White PaperDocumento11 páginasExtractAlpha New Constructs White Paperbharat005Ainda não há avaliações

- GMO Equity Dislocation Strategy Review - 8-21Documento4 páginasGMO Equity Dislocation Strategy Review - 8-21bharat005Ainda não há avaliações

- Worldwide Rig Count Jul 2017Documento13 páginasWorldwide Rig Count Jul 2017aayush007Ainda não há avaliações

- Mid-to-Mega: Industry leadership key to rapid Wealth CreationDocumento60 páginasMid-to-Mega: Industry leadership key to rapid Wealth CreationSanjeev Sadanand PatkarAinda não há avaliações

- Chaman Lal Setia Exports Ltd fundamentals remain intactDocumento18 páginasChaman Lal Setia Exports Ltd fundamentals remain intactbharat005Ainda não há avaliações

- Core Industries 2011-12Documento10 páginasCore Industries 2011-12RhytaAinda não há avaliações

- NCFM Tecnical Analusis ModuleDocumento172 páginasNCFM Tecnical Analusis ModuleDeepali Mishra83% (6)

- 7 Growth StrategiesDocumento0 página7 Growth Strategiesbharat005Ainda não há avaliações

- Karvy Value Invest June 2016 PDFDocumento14 páginasKarvy Value Invest June 2016 PDFbharat005Ainda não há avaliações

- Upl PDFDocumento44 páginasUpl PDFbharat005Ainda não há avaliações

- Venn Diagram (Problem)Documento2 páginasVenn Diagram (Problem)api-3730369Ainda não há avaliações

- Oriental Carbon Chemicals LTD Initiating Coverage 20062016Documento26 páginasOriental Carbon Chemicals LTD Initiating Coverage 20062016bharat005Ainda não há avaliações

- 2014Documento262 páginas2014bharat005Ainda não há avaliações

- Orient Refractories LTD Initiating Coverage 21062016Documento15 páginasOrient Refractories LTD Initiating Coverage 21062016Tarun MittalAinda não há avaliações

- ECI Statistical Report on Andhra Pradesh Assembly Elections, 2014Documento492 páginasECI Statistical Report on Andhra Pradesh Assembly Elections, 2014kdineshcAinda não há avaliações

- $0Rqwh&Duor&Rpsdulvrq Ehwzhhqwkh) Uhh&Dvk) Orzdqg 'LVFRXQWHG&DVK) Orz $ssurdfkhvDocumento17 páginas$0Rqwh&Duor&Rpsdulvrq Ehwzhhqwkh) Uhh&Dvk) Orzdqg 'LVFRXQWHG&DVK) Orz $ssurdfkhvbharat005Ainda não há avaliações

- Economy - Recovery - Real or Rudimentary - Sep-18-EDELDocumento46 páginasEconomy - Recovery - Real or Rudimentary - Sep-18-EDELbharat005Ainda não há avaliações

- Hypothesis Testing - Why Levene Test of Equality of Variances Rather Than F Ratio - Cross ValidatedDocumento1 páginaHypothesis Testing - Why Levene Test of Equality of Variances Rather Than F Ratio - Cross Validatedbharat005Ainda não há avaliações

- 6-Org Appraisal PDFDocumento20 páginas6-Org Appraisal PDFbharat005Ainda não há avaliações

- Assignment Efficient FrontierDocumento36 páginasAssignment Efficient Frontierbharat005Ainda não há avaliações

- Syllabi - EE 5004 - Power ElectronicsDocumento2 páginasSyllabi - EE 5004 - Power ElectronicsKalum ChandraAinda não há avaliações

- Module 6 - FormworksDocumento8 páginasModule 6 - FormworksAldrich Francis Ortiz Peñaflor100% (1)

- Lession Plan - MIDocumento21 páginasLession Plan - MINithya SannidhiAinda não há avaliações

- Booster Pump Service ManualDocumento11 páginasBooster Pump Service ManualSGI AUTOMOTIVE PVT LTDAinda não há avaliações

- Narayana Sukta MeaningDocumento4 páginasNarayana Sukta Meaningvinai.20Ainda não há avaliações

- Hart Fuller Debate: Hart Fuller Debate Is One of The Most Interesting Academic Debates of All Times That Took Place inDocumento1 páginaHart Fuller Debate: Hart Fuller Debate Is One of The Most Interesting Academic Debates of All Times That Took Place inAmishaAinda não há avaliações

- Unit explores Christian morality and conscienceDocumento1 páginaUnit explores Christian morality and conscienceRose Angela Mislang Uligan100% (1)

- Classified Advertisements from Gulf Times NewspaperDocumento6 páginasClassified Advertisements from Gulf Times NewspaperAli Naveed FarookiAinda não há avaliações

- 3 Edition February 2013: Ec2 Guide For Reinforced Concrete Design For Test and Final ExaminationDocumento41 páginas3 Edition February 2013: Ec2 Guide For Reinforced Concrete Design For Test and Final ExaminationDark StingyAinda não há avaliações

- Synopsis THESIS 2022: Aiswarya Vs Tqarebc005 S10Documento5 páginasSynopsis THESIS 2022: Aiswarya Vs Tqarebc005 S10Asna DTAinda não há avaliações

- Orrick PostedbyrequestDocumento4 páginasOrrick PostedbyrequestmungagungadinAinda não há avaliações

- S10 Electric Power PackDocumento12 páginasS10 Electric Power PackrolandAinda não há avaliações

- Prom 2Documento3 páginasProm 2arvindAinda não há avaliações

- Fundamentals of VolleyballDocumento2 páginasFundamentals of VolleyballLawrence CezarAinda não há avaliações

- Why Check Valves SlamDocumento2 páginasWhy Check Valves SlamBramJanssen76Ainda não há avaliações

- Parameters Governing Predicted and Actual RQD Estimation - FINAL - PUBLISHED - VERSIONDocumento14 páginasParameters Governing Predicted and Actual RQD Estimation - FINAL - PUBLISHED - VERSIONKristian Murfitt100% (1)

- Coley A4Documento49 páginasColey A4mfiarkeeaAinda não há avaliações

- Data Biostataplus Sbi2014-EDocumento4 páginasData Biostataplus Sbi2014-ELucila Milagros PinillosAinda não há avaliações

- Dimensions and Relations of The Dentogingival Junction in Humans. Gargiulo 1961Documento7 páginasDimensions and Relations of The Dentogingival Junction in Humans. Gargiulo 1961Linda Garcia PAinda não há avaliações

- Ex Ophtalmo Eng 1Documento4 páginasEx Ophtalmo Eng 1Roxana PascalAinda não há avaliações

- Design of Steel BeamsDocumento4 páginasDesign of Steel BeamsSankalp LamaAinda não há avaliações

- 7H17-28 Clearances and Wear Limits PDFDocumento3 páginas7H17-28 Clearances and Wear Limits PDFDimitris K100% (1)

- Ringing On A Transmission LineDocumento33 páginasRinging On A Transmission LinePrem BhaskaraAinda não há avaliações

- Earthbag House For HaitiDocumento22 páginasEarthbag House For HaitiRaymond KatabaziAinda não há avaliações

- NNDC Planning Applications 4oct - 11 OctDocumento4 páginasNNDC Planning Applications 4oct - 11 OctRichard SmithAinda não há avaliações

- Series: Mechanical Style Pressure SwitchDocumento15 páginasSeries: Mechanical Style Pressure SwitchPhúc Phan TiếnAinda não há avaliações

- DG350 ManualDocumento17 páginasDG350 ManualCareergamingAinda não há avaliações

- Rahim Acar - Talking About God and Talking About Creation. Avicennas and Thomas Aquinas Positions 2005 PDFDocumento134 páginasRahim Acar - Talking About God and Talking About Creation. Avicennas and Thomas Aquinas Positions 2005 PDFPricopi VictorAinda não há avaliações

- Chemical reactions and structuresDocumento22 páginasChemical reactions and structuresStormy StudiosAinda não há avaliações

- MACRO XII Subhash Dey All Chapters PPTs (Teaching Made Easier)Documento2.231 páginasMACRO XII Subhash Dey All Chapters PPTs (Teaching Made Easier)Vatsal HarkarAinda não há avaliações