Você também pode gostar

- Sugar Annual Brussels USEU European Union 04-15-2021Documento16 páginasSugar Annual Brussels USEU European Union 04-15-2021Leonardo Moreno - ChacónAinda não há avaliações

- Interim Report For The 4 Quarter and Year-End 2020: 1 January To 31 December 2020Documento9 páginasInterim Report For The 4 Quarter and Year-End 2020: 1 January To 31 December 2020Elias TalaniAinda não há avaliações

- The State of European Food-Tech 2019Documento23 páginasThe State of European Food-Tech 2019selcukAinda não há avaliações

- LCD European Quarterly 1Q16Documento11 páginasLCD European Quarterly 1Q16Shawn PantophletAinda não há avaliações

- Angler Gaming PLC Q1 Report 2021 FINALDocumento9 páginasAngler Gaming PLC Q1 Report 2021 FINALAnton HenrikssonAinda não há avaliações

- Full Year 2020: 1. Agri-Food Sector Trade - ExportsDocumento4 páginasFull Year 2020: 1. Agri-Food Sector Trade - Exportsaisyaham02Ainda não há avaliações

- 2020 2022 Spain Retail Market Insights - UpdatedDocumento20 páginas2020 2022 Spain Retail Market Insights - Updatedهادی طاهریAinda não há avaliações

- Angler Gaming PLC Q3 Report 2020 FINALDocumento9 páginasAngler Gaming PLC Q3 Report 2020 FINALEmil Elias TalaniAinda não há avaliações

- Dried Fruits Market ResearchDocumento44 páginasDried Fruits Market Researchkshitija GhongadiAinda não há avaliações

- EU Beer Statistics 2018 WebDocumento36 páginasEU Beer Statistics 2018 WebamfipolitisAinda não há avaliações

- European Beer Trends: Statistics Report - 2019 EditionDocumento36 páginasEuropean Beer Trends: Statistics Report - 2019 EditionDanna Rubio100% (1)

- What Is The Demand For Cocoa On The European Market - CBIDocumento10 páginasWhat Is The Demand For Cocoa On The European Market - CBITaio RogersAinda não há avaliações

- How To Web Romanian Venture Report 2021Documento20 páginasHow To Web Romanian Venture Report 2021start-up.roAinda não há avaliações

- Assignment (With Ratios)Documento20 páginasAssignment (With Ratios)Muhammad Umair KhanAinda não há avaliações

- AssignmentDocumento18 páginasAssignmentMuhammad Umair KhanAinda não há avaliações

- PalgraveHandbookofWineEconomicsIndustry - French Wine IndustryDocumento24 páginasPalgraveHandbookofWineEconomicsIndustry - French Wine IndustrygambhirsinghbartwarAinda não há avaliações

- Trade Bulletin Q2 2019: Highlights ImportsDocumento9 páginasTrade Bulletin Q2 2019: Highlights Imports温洁胜Ainda não há avaliações

- The Angolan Agro IndustryDocumento10 páginasThe Angolan Agro IndustrySumit SainiAinda não há avaliações

- Eyedropper Clinic: Accounting Equation: Current Assets Non Current AssetsDocumento5 páginasEyedropper Clinic: Accounting Equation: Current Assets Non Current AssetsSofía MargaritaAinda não há avaliações

- The State of European Food Tech 2021Documento27 páginasThe State of European Food Tech 2021Clifton Mathias YeoAinda não há avaliações

- European - United States Defence Expenditure in 2009: Date: 21.12.2010Documento16 páginasEuropean - United States Defence Expenditure in 2009: Date: 21.12.2010wavijunkAinda não há avaliações

- Indonesia Sugar Annual Indonesia Sugar Annual Report 2019: Date: GAIN Report NumberDocumento10 páginasIndonesia Sugar Annual Indonesia Sugar Annual Report 2019: Date: GAIN Report NumberRSTAinda não há avaliações

- Fruit and Vegetables Market Situation Report 2021 03 en 0Documento21 páginasFruit and Vegetables Market Situation Report 2021 03 en 0Dr. HeleAinda não há avaliações

- Financial Results - First Half 2021: Investors' and Analysts' PresentationDocumento24 páginasFinancial Results - First Half 2021: Investors' and Analysts' PresentationMiguel Couto RamosAinda não há avaliações

- Kelompok 3 - Tugas 3 - Bab 'Persediaan'Documento3 páginasKelompok 3 - Tugas 3 - Bab 'Persediaan'Elsi NonnyAinda não há avaliações

- Honey in Germany: Market ResearchDocumento42 páginasHoney in Germany: Market ResearchArjun Ahuja100% (1)

- Lychee Is A Traditional Fruit of Vietnam, Which First Occurred inDocumento4 páginasLychee Is A Traditional Fruit of Vietnam, Which First Occurred inAn DoAinda não há avaliações

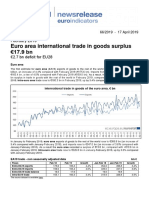

- Euro Area International Trade in Goods Surplus 17.9 BN: February 2019Documento6 páginasEuro Area International Trade in Goods Surplus 17.9 BN: February 2019Valter SilveiraAinda não há avaliações

- Percentage Increase and DecreaseDocumento1 páginaPercentage Increase and Decreaseapi-287224366Ainda não há avaliações

- Romanian Venture Report 2020Documento11 páginasRomanian Venture Report 2020ClaudiuAinda não há avaliações

- Spices ProcessingDocumento28 páginasSpices Processingyenealem Abebe100% (1)

- Case 1 (Accounting Equation)Documento7 páginasCase 1 (Accounting Equation)friti anifaAinda não há avaliações

- Etrangerr I: Frais Scolarite ANDocumento2 páginasEtrangerr I: Frais Scolarite ANdaisyAinda não há avaliações

- Sugar Quarterly Q1 2020Documento18 páginasSugar Quarterly Q1 2020Ahmed OuhniniAinda não há avaliações

- Imt Covid19Documento9 páginasImt Covid19vnv servicesAinda não há avaliações

- Vegan 2Documento10 páginasVegan 2Esther PraveenaAinda não há avaliações

- Overgangstarieven23 24 v3 21022023Documento1 páginaOvergangstarieven23 24 v3 21022023onestop.mediceAinda não há avaliações

- Could We See $2 Gas in Europe in 2020?: October 2019Documento6 páginasCould We See $2 Gas in Europe in 2020?: October 2019IkhsanSolikhuddinAinda não há avaliações

- Wine and ChampagneDocumento19 páginasWine and ChampagneyenealemAinda não há avaliações

- Exercise Chapter 5 For Operations and Supply Chain Management For The 21st CenturyDocumento15 páginasExercise Chapter 5 For Operations and Supply Chain Management For The 21st CenturyTobias Tambo RavnAinda não há avaliações

- Note On The Accounting Treatment of Promissory NotesDocumento2 páginasNote On The Accounting Treatment of Promissory NotesirishpoliticsAinda não há avaliações

- Germany: Merchandise TradeDocumento2 páginasGermany: Merchandise Tradericardo adolfoAinda não há avaliações

- Edpb Report 2021 Overviewsaressourcesandenforcement v3 en 0Documento31 páginasEdpb Report 2021 Overviewsaressourcesandenforcement v3 en 0DuckifiyAinda não há avaliações

- Project Budget MonthlyDocumento8 páginasProject Budget MonthlyIvanGeorgievAinda não há avaliações

- Seychelles: Merchandise TradeDocumento2 páginasSeychelles: Merchandise TradestevenAinda não há avaliações

- Eyedropper Clinic IndividualDocumento2 páginasEyedropper Clinic IndividualSofía MargaritaAinda não há avaliações

- 2021 - The Caviar MarketDocumento43 páginas2021 - The Caviar Marketjuanma950311Ainda não há avaliações

- Chapter 5Documento39 páginasChapter 5dukeee158Ainda não há avaliações

- Summary:! 2 Details:! 6: Group 7Documento17 páginasSummary:! 2 Details:! 6: Group 7Morgan KalifaAinda não há avaliações

- Comparative Advantage EssayDocumento3 páginasComparative Advantage EssayDaniel Signorile100% (1)

- 2011 Fresh Grapes in The United KingdomDocumento5 páginas2011 Fresh Grapes in The United KingdomOmar Santamaría CastilloAinda não há avaliações

- Excise Duty Tables: Part I - Alcoholic BeveragesDocumento45 páginasExcise Duty Tables: Part I - Alcoholic BeveragesMădălinaAinda não há avaliações

- Glovo Customer Service Market ResearchDocumento13 páginasGlovo Customer Service Market ResearchALBERTO MARIO CHAMORRO PACHECOAinda não há avaliações

- Assignment 1: Holiday Summer Park: A. Prepare An Income Statement For HSPDocumento7 páginasAssignment 1: Holiday Summer Park: A. Prepare An Income Statement For HSPZahra HussainAinda não há avaliações

- European Statistics Handbook 2021Documento23 páginasEuropean Statistics Handbook 2021Coringa HotmartAinda não há avaliações

- Fair Trade and The Lao PDR - English VersionDocumento4 páginasFair Trade and The Lao PDR - English VersionFair Trade LaosAinda não há avaliações

- Economics For Managers: External Sector/Open EconomyDocumento63 páginasEconomics For Managers: External Sector/Open EconomyRomit BanerjeeAinda não há avaliações

- Chap 6Documento20 páginasChap 6api-3729903Ainda não há avaliações

- Amount Consumed (8-Ounce Glasses) Total Utility Marginal UtilityDocumento2 páginasAmount Consumed (8-Ounce Glasses) Total Utility Marginal UtilityKriszia Jean Mangubat TingubanAinda não há avaliações

- Session 6 (A) - Puzzling Times (Macro Currencies) - Jan Lambregts Rabobank - Original.1550055484 PDFDocumento31 páginasSession 6 (A) - Puzzling Times (Macro Currencies) - Jan Lambregts Rabobank - Original.1550055484 PDFiljanAinda não há avaliações

- Workshop 4 (B) - Algos For Humans Dev Gill Marex Spectron - Original.1550055327Documento7 páginasWorkshop 4 (B) - Algos For Humans Dev Gill Marex Spectron - Original.1550055327iljanAinda não há avaliações

- Session 5 - India - Policy Crop Ethanol - Siddharth Amin DR Amin Controllers - Original.1550055423Documento12 páginasSession 5 - India - Policy Crop Ethanol - Siddharth Amin DR Amin Controllers - Original.1550055423iljanAinda não há avaliações

- Nikon Photographers Handbook 2016 Uk1129Documento224 páginasNikon Photographers Handbook 2016 Uk1129iljan100% (2)

- Straightforward 2e Upp TBDocumento213 páginasStraightforward 2e Upp TBiljanAinda não há avaliações

- WB PDFDocumento70 páginasWB PDFiljan100% (2)

- Notice: Constable (Driver) - Male in Delhi Police Examination, 2022Documento50 páginasNotice: Constable (Driver) - Male in Delhi Police Examination, 2022intzar aliAinda não há avaliações

- PropertycasesforfinalsDocumento40 páginasPropertycasesforfinalsRyan Christian LuposAinda não há avaliações

- Internal Rules of Procedure Sangguniang BarangayDocumento37 páginasInternal Rules of Procedure Sangguniang Barangayhearty sianenAinda não há avaliações

- LR 7833Documento11 páginasLR 7833Trung ĐinhAinda não há avaliações

- Mendoza - Kyle Andre - BSEE-1A (STS ACTIVITY 5)Documento1 páginaMendoza - Kyle Andre - BSEE-1A (STS ACTIVITY 5)Kyle Andre MendozaAinda não há avaliações

- Simplified Electronic Design of The Function : ARMTH Start & Stop SystemDocumento6 páginasSimplified Electronic Design of The Function : ARMTH Start & Stop SystembadrAinda não há avaliações

- 1INDEA2022001Documento90 páginas1INDEA2022001Renata SilvaAinda não há avaliações

- The Rise of Political Fact CheckingDocumento17 páginasThe Rise of Political Fact CheckingGlennKesslerWPAinda não há avaliações

- Ict - chs9 Lesson 5 - Operating System (Os) ErrorsDocumento8 páginasIct - chs9 Lesson 5 - Operating System (Os) ErrorsOmengMagcalasAinda não há avaliações

- Ob AssignmntDocumento4 páginasOb AssignmntOwais AliAinda não há avaliações

- Demand and SupplyDocumento61 páginasDemand and SupplyGirish PremchandranAinda não há avaliações

- Pharmaniaga Paracetamol Tablet: What Is in This LeafletDocumento2 páginasPharmaniaga Paracetamol Tablet: What Is in This LeafletWei HangAinda não há avaliações

- Final Test General English TM 2021Documento2 páginasFinal Test General English TM 2021Nenden FernandesAinda não há avaliações

- Manhole DetailDocumento1 páginaManhole DetailchrisAinda não há avaliações

- August 2023 Asylum ProcessingDocumento14 páginasAugust 2023 Asylum ProcessingHenyiali RinconAinda não há avaliações

- A List of Run Commands For Wind - Sem AutorDocumento6 páginasA List of Run Commands For Wind - Sem AutorJoão José SantosAinda não há avaliações

- DE1734859 Central Maharashtra Feb'18Documento39 páginasDE1734859 Central Maharashtra Feb'18Adesh NaharAinda não há avaliações

- Fix Problems in Windows SearchDocumento2 páginasFix Problems in Windows SearchSabah SalihAinda não há avaliações

- Feng Shui GeneralDocumento36 páginasFeng Shui GeneralPia SalvadorAinda não há avaliações

- Chemical BondingDocumento7 páginasChemical BondingSanaa SamkoAinda não há avaliações

- NI 43-101 Technical Report - Lithium Mineral Resource Estimate Zeus Project, Clayton Valley, USADocumento71 páginasNI 43-101 Technical Report - Lithium Mineral Resource Estimate Zeus Project, Clayton Valley, USAGuillaume De SouzaAinda não há avaliações

- Img - Oriental Magic by Idries Shah ImageDocumento119 páginasImg - Oriental Magic by Idries Shah ImageCarolos Strangeness Eaves100% (2)

- Weird Tales v14 n03 1929Documento148 páginasWeird Tales v14 n03 1929HenryOlivr50% (2)

- Chapter 6 Bone Tissue 2304Documento37 páginasChapter 6 Bone Tissue 2304Sav Oli100% (1)

- Advanced Financial Accounting and Reporting Accounting For PartnershipDocumento6 páginasAdvanced Financial Accounting and Reporting Accounting For PartnershipMaria BeatriceAinda não há avaliações

- Post Cold WarDocumento70 páginasPost Cold WarZainab WaqarAinda não há avaliações

- Manalili v. CA PDFDocumento3 páginasManalili v. CA PDFKJPL_1987100% (1)

- VIII and IXDocumento56 páginasVIII and IXTinn ApAinda não há avaliações

- Slides 99 Netslicing Georg Mayer 3gpp Network Slicing 04Documento13 páginasSlides 99 Netslicing Georg Mayer 3gpp Network Slicing 04malli gaduAinda não há avaliações

- Packing List Night at Starlodge Adventure SuitesDocumento2 páginasPacking List Night at Starlodge Adventure SuitesArturo PerezAinda não há avaliações