Você também pode gostar

- SPP SummarizedDocumento9 páginasSPP SummarizedLanz Castro67% (3)

- Unlawful Detainer Complaint 12.23.19Documento33 páginasUnlawful Detainer Complaint 12.23.19GeekWireAinda não há avaliações

- The Role of 'Law As Integrity' in Ronald Dworkin's ThinkingDocumento12 páginasThe Role of 'Law As Integrity' in Ronald Dworkin's Thinkingpleitch1100% (1)

- What Is Fiscal AutonomyDocumento3 páginasWhat Is Fiscal AutonomymtabcaoAinda não há avaliações

- Application Procedures and RequirementsDocumento5 páginasApplication Procedures and Requirementssui1981Ainda não há avaliações

- Araullo v. Aquino - DigestDocumento16 páginasAraullo v. Aquino - DigestFannie NagalloAinda não há avaliações

- DOCTRINE: (Standard of Care Required)Documento3 páginasDOCTRINE: (Standard of Care Required)Judy Rivera100% (2)

- Cases Civpro Rule 66Documento31 páginasCases Civpro Rule 66Gracey Sagario Dela TorreAinda não há avaliações

- Declaration of The Existence of A State of WarDocumento10 páginasDeclaration of The Existence of A State of WarAmicahAinda não há avaliações

- Final Exam Reviewer 7. Powers of Congress: A. General Plenary PowersDocumento55 páginasFinal Exam Reviewer 7. Powers of Congress: A. General Plenary PowersRoze JustinAinda não há avaliações

- Araullo vs. AquinoDocumento10 páginasAraullo vs. AquinoRICKY ALEGARBESAinda não há avaliações

- Constitutional Law Reviewer For FinalsDocumento55 páginasConstitutional Law Reviewer For FinalsGodofredo De Leon Sabado100% (1)

- Araullo V Aquino DigestDocumento16 páginasAraullo V Aquino Digestarmypadilla7201Ainda não há avaliações

- Belgica V Ochoa - Comprehensive DigestDocumento4 páginasBelgica V Ochoa - Comprehensive DigestMegAinda não há avaliações

- Constitutional Provisions On BudgetingDocumento6 páginasConstitutional Provisions On BudgetingJohn Dx LapidAinda não há avaliações

- Notes For Re-Enacted Budget Article Vi The Legislative DepartmentDocumento9 páginasNotes For Re-Enacted Budget Article Vi The Legislative DepartmentKitem Kadatuan Jr.Ainda não há avaliações

- Facts:: Garcia Et Al. Vs ComelecDocumento5 páginasFacts:: Garcia Et Al. Vs ComelecYnna GesiteAinda não há avaliações

- 14 DigestDocumento3 páginas14 DigestARCHIE AJIASAinda não há avaliações

- Constitutional Amendments 2010Documento22 páginasConstitutional Amendments 2010Steve TerrellAinda não há avaliações

- Notes in Legislative Department (Philippine Constitution)Documento20 páginasNotes in Legislative Department (Philippine Constitution)RyDAinda não há avaliações

- Case Digest - Maria Carolina P. Araullo v. Benigno Simeon C. Aquino IIIDocumento14 páginasCase Digest - Maria Carolina P. Araullo v. Benigno Simeon C. Aquino IIIJemiema ArroAinda não há avaliações

- Consti Digest Cases 2Documento115 páginasConsti Digest Cases 2Iligan CpoAinda não há avaliações

- Ed 1Documento25 páginasEd 1Shaira Jean SollanoAinda não há avaliações

- Abakada Guro Party List V Purisima G.R. NO. 166715, AUGUST 14, 2008 FactsDocumento5 páginasAbakada Guro Party List V Purisima G.R. NO. 166715, AUGUST 14, 2008 FactsPatatas SayoteAinda não há avaliações

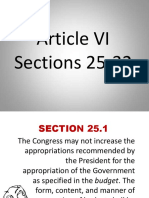

- CONSTI 1 - Article VI Sections 25-27 10272022Documento13 páginasCONSTI 1 - Article VI Sections 25-27 10272022Docefjord EncarnacionAinda não há avaliações

- Consti 4Documento5 páginasConsti 4renjomar baltazarAinda não há avaliações

- Consti Finals NotesDocumento47 páginasConsti Finals NotesCarina Amor ClaveriaAinda não há avaliações

- September 8 - ConstiDocumento19 páginasSeptember 8 - ConstiMonica Margarette Feril100% (2)

- Article VI Sections 25-32Documento66 páginasArticle VI Sections 25-32Rhison AsiaAinda não há avaliações

- Final Legal OpinionDocumento4 páginasFinal Legal OpinionAiza SaraAinda não há avaliações

- JudiciaryDocumento76 páginasJudiciaryAttydir16gmail.comAinda não há avaliações

- Review Notes/Political Science/Article VI/Finals/Cayetano Page 1 of 8Documento8 páginasReview Notes/Political Science/Article VI/Finals/Cayetano Page 1 of 8ancaye1962Ainda não há avaliações

- Abakada Vs Ermita Case DigestDocumento3 páginasAbakada Vs Ermita Case DigestSamantha ReyesAinda não há avaliações

- Araullo Vs AquinoDocumento5 páginasAraullo Vs AquinoJo S.Ainda não há avaliações

- The Origination Clause of The US Constitution: Interpretation and EnforcementDocumento20 páginasThe Origination Clause of The US Constitution: Interpretation and EnforcementJohn MalcolmAinda não há avaliações

- Param orDocumento13 páginasParam orCarina Amor ClaveriaAinda não há avaliações

- Araullo Vs AquinoDocumento14 páginasAraullo Vs AquinoJeorge Ryan MangubatAinda não há avaliações

- Constitutional Interpretation of Statutes in The Republic of South AfricaDocumento18 páginasConstitutional Interpretation of Statutes in The Republic of South Africaprudencemangena123Ainda não há avaliações

- CASE DIGEST - Belgica v. Executive Secretary (G.R. Nos. 208566, 208493 and 209251, 2013) - Emir MendozaDocumento5 páginasCASE DIGEST - Belgica v. Executive Secretary (G.R. Nos. 208566, 208493 and 209251, 2013) - Emir MendozaPatronus GoldenAinda não há avaliações

- Araullo v. Aquino DAP CaseDocumento6 páginasAraullo v. Aquino DAP CasefclalarilaAinda não há avaliações

- Law MakingDocumento41 páginasLaw MakingRohanAinda não há avaliações

- G.R. No. 209287. February 3, 2015. Araullo vs. Aquino IIIDocumento58 páginasG.R. No. 209287. February 3, 2015. Araullo vs. Aquino IIIclaudine uananAinda não há avaliações

- Arturo M Tolentino Vs Secretary of Finance Et AlDocumento4 páginasArturo M Tolentino Vs Secretary of Finance Et AlKael MarmaladeAinda não há avaliações

- Arturo M Tolentino Vs Secretary of Finance Et AlDocumento4 páginasArturo M Tolentino Vs Secretary of Finance Et AlKhian JamerAinda não há avaliações

- The Branches of Philippine Government Lesson OutcomesDocumento13 páginasThe Branches of Philippine Government Lesson OutcomesInaAinda não há avaliações

- Liwanag NG LangitDocumento24 páginasLiwanag NG LangitDustin Joseph Fetalino Mazo33% (3)

- Philippine Constitutional Association Vs EnriquezDocumento1 páginaPhilippine Constitutional Association Vs Enriquezmaginoo69Ainda não há avaliações

- Lecture Notes/Guide Article VI, VII, VIII of The Philippine ConstitutionDocumento3 páginasLecture Notes/Guide Article VI, VII, VIII of The Philippine ConstitutionWehn TengAinda não há avaliações

- Forms of StatutesDocumento17 páginasForms of StatutesMiguel CastricionesAinda não há avaliações

- Case Digest: Bengzon vs. Drilon G.R. No. 103524 (15 April 1992) FactsDocumento4 páginasCase Digest: Bengzon vs. Drilon G.R. No. 103524 (15 April 1992) FactsCatherine Joy CataminAinda não há avaliações

- Araullo vs. AquinoDocumento2 páginasAraullo vs. AquinoSantos Kharl MenesAinda não há avaliações

- Roles of CADocumento17 páginasRoles of CAREJAY89Ainda não há avaliações

- B. PLANAS VS. GIL, 67 Phil. 62 C. Luzon Stevedoring vs. SSS, 34 Scra 178 D. Garcia vs. Macaraig, 39 Scra 106Documento18 páginasB. PLANAS VS. GIL, 67 Phil. 62 C. Luzon Stevedoring vs. SSS, 34 Scra 178 D. Garcia vs. Macaraig, 39 Scra 106Hana Danische ElliotAinda não há avaliações

- Valentin Tio Vs Videogram Regulatory BoardDocumento9 páginasValentin Tio Vs Videogram Regulatory BoardErick Jay InokAinda não há avaliações

- Part V DigestsDocumento35 páginasPart V DigestsTamara Claudette BautistaAinda não há avaliações

- Philippine Constitution Association (PHILCONSA) Et Al Vs Salvador Enriquez 235 SCRA 506Documento7 páginasPhilippine Constitution Association (PHILCONSA) Et Al Vs Salvador Enriquez 235 SCRA 506Aubrey Mae VargasAinda não há avaliações

- Araullo-V-AquinoDocumento10 páginasAraullo-V-AquinoRay Joshua ValdezAinda não há avaliações

- Sanchez vs. Commission On Audit 552 SCRA 471 2008 Facts: (I Just Copied This From The Net Hehe Taas Kaayo Na Kaso Man Gud NiDocumento3 páginasSanchez vs. Commission On Audit 552 SCRA 471 2008 Facts: (I Just Copied This From The Net Hehe Taas Kaayo Na Kaso Man Gud NiDawn Jessa GoAinda não há avaliações

- Araullo v. Aquino G.R. 209287 July 1, 2014 Bersamin JDocumento5 páginasAraullo v. Aquino G.R. 209287 July 1, 2014 Bersamin JMarkee Nepomuceno AngelesAinda não há avaliações

- Public Policy MODULE 3Documento5 páginasPublic Policy MODULE 3Darren GarciaAinda não há avaliações

- Separation, Delegation, and The LegislativeDocumento30 páginasSeparation, Delegation, and The LegislativeYosef_d100% (1)

- Political Law Cases - Local Givernment UnitsDocumento52 páginasPolitical Law Cases - Local Givernment UnitsPrinting Panda100% (1)

- Module 2 Case Digest StatconDocumento14 páginasModule 2 Case Digest StatconMama AnjongAinda não há avaliações

- Fit and Proper RuleDocumento2 páginasFit and Proper RuleNicole PTAinda não há avaliações

- IRR RA 11057 RRD Pages 35 42Documento8 páginasIRR RA 11057 RRD Pages 35 42Nicole PTAinda não há avaliações

- 1 - BOI-Advisory - Dated March 20 20Documento2 páginas1 - BOI-Advisory - Dated March 20 20Nicole PTAinda não há avaliações

- FishBowl SectionsDocumento8 páginasFishBowl SectionsNicole PTAinda não há avaliações

- Evidence CAse Matrix 2Documento17 páginasEvidence CAse Matrix 2Nicole PTAinda não há avaliações

- Corp Gov - Class HandoutsDocumento9 páginasCorp Gov - Class HandoutsNicole PTAinda não há avaliações

- Evidence CAse Matrix 2Documento16 páginasEvidence CAse Matrix 2Nicole PTAinda não há avaliações

- Political Law Review Doctrines 2 Art. VI Secs. 13 17Documento28 páginasPolitical Law Review Doctrines 2 Art. VI Secs. 13 17Nicole PTAinda não há avaliações

- 2C 2019 Part 2-2Documento26 páginas2C 2019 Part 2-2Nicole PTAinda não há avaliações

- Crim II Title X NotesDocumento10 páginasCrim II Title X NotesNicole PTAinda não há avaliações

- Political Law Review Doctrines 2 Art. VI Secs. 13 17Documento28 páginasPolitical Law Review Doctrines 2 Art. VI Secs. 13 17Nicole PTAinda não há avaliações

- Comm Emergency DigestsDocumento7 páginasComm Emergency DigestsNicole PTAinda não há avaliações

- Civ NotesDocumento20 páginasCiv NotesNicole PTAinda não há avaliações

- Corp Gov Presentation - TorresDocumento12 páginasCorp Gov Presentation - TorresNicole PTAinda não há avaliações

- Political Law Review Doctrines 8 Arts. VIII Secs. 55 11 and IX A Secs. 5 7Documento23 páginasPolitical Law Review Doctrines 8 Arts. VIII Secs. 55 11 and IX A Secs. 5 7Nicole PTAinda não há avaliações

- Poli DoctrinesDocumento13 páginasPoli DoctrinesNicole PTAinda não há avaliações

- Political Law Review Doctrines 1 Arts. I II and VI Secs. 1 11Documento27 páginasPolitical Law Review Doctrines 1 Arts. I II and VI Secs. 1 11Nicole PTAinda não há avaliações

- Tax I Digest CompilationDocumento9 páginasTax I Digest CompilationNicole PTAinda não há avaliações

- Ang Paghahanap Sa Tamang Tama Ni Buddhadasa BikkhuDocumento3 páginasAng Paghahanap Sa Tamang Tama Ni Buddhadasa BikkhuNicole PTAinda não há avaliações

- CLVDocumento11 páginasCLVNicole PTAinda não há avaliações

- Assailed Provisions Petitioner's Contentions Ruling of The CourtDocumento3 páginasAssailed Provisions Petitioner's Contentions Ruling of The CourtNicole PTAinda não há avaliações

- Tax I Digest CompilationDocumento2 páginasTax I Digest CompilationNicole PTAinda não há avaliações

- Pp. 764 To 777Documento3 páginasPp. 764 To 777Nicole PTAinda não há avaliações

- 1 OutlineDocumento4 páginas1 OutlineNicole PTAinda não há avaliações

- SpecPro Doctrines 7 Rules 103 and 108Documento17 páginasSpecPro Doctrines 7 Rules 103 and 108Nicole PTAinda não há avaliações

- P L P: J V: Hilippine Aw and Ractice On Oint Entures I. N J V P S 1. J V A P G C L PDocumento16 páginasP L P: J V: Hilippine Aw and Ractice On Oint Entures I. N J V P S 1. J V A P G C L PNicole PTAinda não há avaliações

- Finals 2c ReviewerDocumento60 páginasFinals 2c ReviewerIya AnonasAinda não há avaliações

- 1 OutlineDocumento4 páginas1 OutlineNicole PTAinda não há avaliações

- Labor Cases March 2018Documento3 páginasLabor Cases March 2018Nicole PTAinda não há avaliações

- Henry Foyal PrincipleDocumento10 páginasHenry Foyal PrincipleAmit JaiswalAinda não há avaliações

- Fidel Ramos1Documento20 páginasFidel Ramos1MCDABCAinda não há avaliações

- Ensayo ASTM E84 Panel RocaDocumento5 páginasEnsayo ASTM E84 Panel RocaToniHospitalerAinda não há avaliações

- EPG Construction Vs CA (Digest)Documento2 páginasEPG Construction Vs CA (Digest)カルリー カヒミAinda não há avaliações

- United States v. David Valadez-Gallegos, 162 F.3d 1256, 10th Cir. (1998)Documento12 páginasUnited States v. David Valadez-Gallegos, 162 F.3d 1256, 10th Cir. (1998)Scribd Government DocsAinda não há avaliações

- Consultant For Development and Operation of National Data and Analytics Platform (NDAP)Documento157 páginasConsultant For Development and Operation of National Data and Analytics Platform (NDAP)antara choudhury khannaAinda não há avaliações

- Notes Ilw1501 Introduction To LawDocumento11 páginasNotes Ilw1501 Introduction To Lawunderstand ingAinda não há avaliações

- United States v. Dominic Santarelli, in Re United States of America, 729 F.2d 1388, 11th Cir. (1984)Documento5 páginasUnited States v. Dominic Santarelli, in Re United States of America, 729 F.2d 1388, 11th Cir. (1984)Scribd Government DocsAinda não há avaliações

- Pre Test Takko - TUV Rheinland India Textile Testing 2046567-00Documento3 páginasPre Test Takko - TUV Rheinland India Textile Testing 2046567-00Sabeeh Ul HassanAinda não há avaliações

- Percentage Distribution of CICL by Sex: Age No. Percent 10 11 12 13 14 15 16 17 18 TotalDocumento8 páginasPercentage Distribution of CICL by Sex: Age No. Percent 10 11 12 13 14 15 16 17 18 TotalShefferd BernalesAinda não há avaliações

- PLM vs. IAC PDFDocumento17 páginasPLM vs. IAC PDFAivan Charles TorresAinda não há avaliações

- Legal Ethics Duty To Clients CasesDocumento66 páginasLegal Ethics Duty To Clients CasesJongAtmosferaAinda não há avaliações

- I. What Is Taxation?Documento4 páginasI. What Is Taxation?gheljoshAinda não há avaliações

- How A Bill Becomes A Law (Ushistory - Org)Documento1 páginaHow A Bill Becomes A Law (Ushistory - Org)GlennAinda não há avaliações

- Title: Document/Drawing Approval/Comment Transmittal: Comments On 132kV Cable Termination Frame DrawingDocumento2 páginasTitle: Document/Drawing Approval/Comment Transmittal: Comments On 132kV Cable Termination Frame DrawingPritom AhmedAinda não há avaliações

- CS Form No. 212 Personal Data Sheet NOLLADocumento4 páginasCS Form No. 212 Personal Data Sheet NOLLAShenna AllonAinda não há avaliações

- Taxation Law ProjectDocumento20 páginasTaxation Law ProjectJain Rajat ChopraAinda não há avaliações

- United States v. Briceno, 1st Cir. (2014)Documento7 páginasUnited States v. Briceno, 1st Cir. (2014)Scribd Government DocsAinda não há avaliações

- EMEA Groupon Goods Marketplace ContractDocumento11 páginasEMEA Groupon Goods Marketplace Contractcoach djunaediAinda não há avaliações

- Notice of Claim Senate FinalDocumento44 páginasNotice of Claim Senate FinalDanny Shapiro0% (1)

- Maintenance Muslim Law ProjectDocumento13 páginasMaintenance Muslim Law ProjectCharit MudgilAinda não há avaliações

- 05 Imperial V CADocumento1 página05 Imperial V CAFrances Lipnica PabilaneAinda não há avaliações

- Randi ZurenkoDocumento4 páginasRandi ZurenkoChrisAinda não há avaliações

- United States V Halliburton and NL Industries 2009 WL 3260540 (SD Texas 2009) (Hon. J. Nancy F. Atlas)Documento17 páginasUnited States V Halliburton and NL Industries 2009 WL 3260540 (SD Texas 2009) (Hon. J. Nancy F. Atlas)polluterwatchAinda não há avaliações

- Dilip Chhabria v. Minda Capital PVT LTDDocumento3 páginasDilip Chhabria v. Minda Capital PVT LTDvarshiniAinda não há avaliações

- Cynthia Vela PDFDocumento7 páginasCynthia Vela PDFRecordTrac - City of OaklandAinda não há avaliações