Você também pode gostar

- Foreclosure Secrets Ebook - 2008Documento127 páginasForeclosure Secrets Ebook - 2008scribe1111Ainda não há avaliações

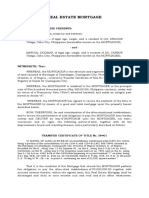

- Real Estate Mortgage SampleDocumento2 páginasReal Estate Mortgage SampleMacky Cid83% (29)

- CredTrans Q&ADocumento23 páginasCredTrans Q&AAshAngeLAinda não há avaliações

- Chattel Mortgage Report MCQsDocumento2 páginasChattel Mortgage Report MCQsMonefah Mulok100% (1)

- Doj NPS ManualDocumento40 páginasDoj NPS Manualed flores92% (13)

- Prefinals With Answer Quiz 1Documento7 páginasPrefinals With Answer Quiz 1Loi Gacho100% (1)

- Meetings, Stocks and Stockholders, Corporate Books and Records Under The Civil Code of The PhilippinesDocumento73 páginasMeetings, Stocks and Stockholders, Corporate Books and Records Under The Civil Code of The PhilippinesMimi VargasAinda não há avaliações

- Law and Practice of BankingDocumento106 páginasLaw and Practice of BankingArvind RaviAinda não há avaliações

- Fulfilling obligations faithfullyDocumento18 páginasFulfilling obligations faithfullyDiane Uy100% (2)

- VSA-IRS Obligations Part 1 ReviewDocumento32 páginasVSA-IRS Obligations Part 1 ReviewjpbluejnAinda não há avaliações

- Regulatory Framework For Business Transaction-SIR SALVADocumento248 páginasRegulatory Framework For Business Transaction-SIR SALVASofia SanchezAinda não há avaliações

- Agency Test Bank Soriano 2016Documento21 páginasAgency Test Bank Soriano 2016jillianAinda não há avaliações

- Business Law Quiz ObligationsDocumento17 páginasBusiness Law Quiz ObligationsDanica PelenioAinda não há avaliações

- Statutory Construction Agpalo PDFDocumento70 páginasStatutory Construction Agpalo PDFYan Lean Dollison67% (3)

- 1 - Social Media Use Integration Scale PDFDocumento13 páginas1 - Social Media Use Integration Scale PDFYelnats Datsima100% (2)

- Oblicon and SalesDocumento12 páginasOblicon and SalesHyman Jay Blanco100% (2)

- LABOR by Poquiz PDFDocumento23 páginasLABOR by Poquiz PDFAnonymous 7BpT9OWP100% (3)

- Credit Transactions (Digested Cases)Documento23 páginasCredit Transactions (Digested Cases)Marie Antoinette Espadilla75% (4)

- People V Villalon DigestDocumento2 páginasPeople V Villalon DigestevgciikAinda não há avaliações

- Estate Tax Dispute of Late President MarcosDocumento13 páginasEstate Tax Dispute of Late President MarcosYelnats DatsimaAinda não há avaliações

- Civil Law 1 Finals Compilation of Quizzes 1-29Documento96 páginasCivil Law 1 Finals Compilation of Quizzes 1-29Yelnats DatsimaAinda não há avaliações

- Bl.m-1402.Law On ContractsDocumento23 páginasBl.m-1402.Law On ContractsCharry RamosAinda não há avaliações

- Contracts QuestionsDocumento2 páginasContracts QuestionsFranz MarcosAinda não há avaliações

- Case Digest - Transportation LawDocumento14 páginasCase Digest - Transportation LawAiko DalaganAinda não há avaliações

- Regulatory Framework For Business Transactions Law On Sales and PartnershipDocumento13 páginasRegulatory Framework For Business Transactions Law On Sales and PartnershipAngelo IvanAinda não há avaliações

- Special Proceedings Memory AidDocumento36 páginasSpecial Proceedings Memory AidJoan DelatadoAinda não há avaliações

- ContractsDocumento21 páginasContractsDea Lyn BaculaAinda não há avaliações

- Tax Lecture Estate Tax Part 2Documento7 páginasTax Lecture Estate Tax Part 2Kathreen Aya ExcondeAinda não há avaliações

- Chapter 18 Anemia HematologyDocumento30 páginasChapter 18 Anemia HematologyYelnats DatsimaAinda não há avaliações

- Beda Bar Questions in SalesDocumento9 páginasBeda Bar Questions in SalesalbemartAinda não há avaliações

- Credit Transactions MCQDocumento3 páginasCredit Transactions MCQeinsteinspy100% (1)

- DONE - Homework Law1301 - Topic Credit Transaction NADocumento3 páginasDONE - Homework Law1301 - Topic Credit Transaction NAJosh JoshAinda não há avaliações

- Law On Sales HandoutsDocumento16 páginasLaw On Sales HandoutsRhejean LozanoAinda não há avaliações

- Development Agreement Draft for Sukhshanti Co-op Housing SocietyDocumento27 páginasDevelopment Agreement Draft for Sukhshanti Co-op Housing SocietyAniket Parikh100% (1)

- Contracts ReviewerDocumento6 páginasContracts ReviewerMark Noel SanteAinda não há avaliações

- 1st HandoutDocumento23 páginas1st HandoutMary Therese FloresAinda não há avaliações

- Final Format For Credit MidtermDocumento8 páginasFinal Format For Credit MidtermCloieRjAinda não há avaliações

- Pledge ReportingDocumento8 páginasPledge ReportingRosette G. ReynoAinda não há avaliações

- Pledge, Mortgage Difference TableDocumento2 páginasPledge, Mortgage Difference TablePatricia Mae AmoresAinda não há avaliações

- Credit Transactions MCQDocumento4 páginasCredit Transactions MCQdaylojerome100% (2)

- BL SorianoDocumento42 páginasBL SorianoMina MyouiAinda não há avaliações

- LOAN, PLEDGE & MORTGAGE - MCQs SY 16-17 2ND SEM-2Documento9 páginasLOAN, PLEDGE & MORTGAGE - MCQs SY 16-17 2ND SEM-2Judy De La CruzAinda não há avaliações

- BE 301 - Attempt ReviewDocumento34 páginasBE 301 - Attempt ReviewPolinar Paul MarbenAinda não há avaliações

- cREDIT tRANSACTIONS1Documento6 páginascREDIT tRANSACTIONS1Janil Jay EquizaAinda não há avaliações

- Obligations and Contracts ExamDocumento7 páginasObligations and Contracts ExamJovito ReyesAinda não há avaliações

- LawDocumento5 páginasLawJhunnel LangubanAinda não há avaliações

- ACTIVITY Learners GuideDocumento2 páginasACTIVITY Learners GuideRhean ScottAinda não há avaliações

- 4 TH AssignmentDocumento8 páginas4 TH AssignmentUmbina GesceryAinda não há avaliações

- Pre WeekDocumento15 páginasPre Weekchowchow123Ainda não há avaliações

- Multiple choice questions on negotiable instruments, contracts, corporations and partnershipsDocumento11 páginasMultiple choice questions on negotiable instruments, contracts, corporations and partnershipsJinx Cyrus RodilloAinda não há avaliações

- Nego 1Documento16 páginasNego 1Wil G. Binuya Jr.Ainda não há avaliações

- Drills Exercises 18-Jan-2020Documento2 páginasDrills Exercises 18-Jan-2020MCPS Operations BranchAinda não há avaliações

- Pledge and MortgageDocumento5 páginasPledge and MortgageMhiletAinda não há avaliações

- RFBTDocumento19 páginasRFBTJin Hee AhnAinda não há avaliações

- Obligation quiz answers and legal conceptsDocumento14 páginasObligation quiz answers and legal conceptsRen EyAinda não há avaliações

- Business Law - Sales MCQ Reviewer PDFDocumento2 páginasBusiness Law - Sales MCQ Reviewer PDFastra_per_asperaAinda não há avaliações

- Special Commercial LawsDocumento17 páginasSpecial Commercial Lawsgeelyka marquez100% (1)

- LawDocumento1 páginaLawRhap SodyAinda não há avaliações

- Credit MCQ (Real Mortgage)Documento2 páginasCredit MCQ (Real Mortgage)Monefah Mulok100% (1)

- Q1Q2 MendozaDocumento40 páginasQ1Q2 MendozaMojan VianaAinda não há avaliações

- Negotiable InstrumentsDocumento4 páginasNegotiable Instrumentslaura santosAinda não há avaliações

- Rights of Antichretic CreditorDocumento2 páginasRights of Antichretic CreditorKyo Pneuma100% (1)

- Contributor: Atty. Mendoza, B. Date Contributed: March 2011Documento8 páginasContributor: Atty. Mendoza, B. Date Contributed: March 2011Darynn LinggonAinda não há avaliações

- Understanding NovationDocumento47 páginasUnderstanding NovationNeb GarcAinda não há avaliações

- Case Digest Double Sale CasesDocumento2 páginasCase Digest Double Sale Casesjetzon2022Ainda não há avaliações

- Exer LawDocumento8 páginasExer LawRed MendozaAinda não há avaliações

- Nego MCQDocumento13 páginasNego MCQwainie_deroAinda não há avaliações

- KEY Level 2 QuestionsDocumento5 páginasKEY Level 2 QuestionsDarelle Hannah MarquezAinda não há avaliações

- Law 1Documento14 páginasLaw 1Park Min Eun100% (1)

- RFBT CHALLENGE questionsDocumento7 páginasRFBT CHALLENGE questionsRegine YbañezAinda não há avaliações

- NEGOTIABLE INSTRUMENTS REVIEWERDocumento12 páginasNEGOTIABLE INSTRUMENTS REVIEWERGrace AustriaAinda não há avaliações

- This Study Resource Was: Contributor: Atty. Mendoza, B. Date Contributed: March 2011Documento7 páginasThis Study Resource Was: Contributor: Atty. Mendoza, B. Date Contributed: March 2011Jan Christopher CabadingAinda não há avaliações

- Midterm Examination AccDocumento3 páginasMidterm Examination AccJoseph LittleAinda não há avaliações

- Fria QuizDocumento2 páginasFria QuizdavidgollaAinda não há avaliações

- Second PB Acctg 203BDocumento12 páginasSecond PB Acctg 203BBella AyabAinda não há avaliações

- A3 Topic 3 Part 2 - Cost of CapitalDocumento2 páginasA3 Topic 3 Part 2 - Cost of CapitalJoshua BautistaAinda não há avaliações

- Bonnevie vs. Ca 3. Rosepacking Co. vs. Ca 4.bpi Investment Corp. vs. CaDocumento4 páginasBonnevie vs. Ca 3. Rosepacking Co. vs. Ca 4.bpi Investment Corp. vs. CaLea Angelica RiofloridoAinda não há avaliações

- Barcellano v. BañasDocumento9 páginasBarcellano v. BañasVeen Galicinao FernandezAinda não há avaliações

- Some Cases For TORTS and DAMAGESDocumento1 páginaSome Cases For TORTS and DAMAGESYelnats DatsimaAinda não há avaliações

- Abalos Vs CADocumento6 páginasAbalos Vs CAYelnats DatsimaAinda não há avaliações

- Albano Civil Law Barquestions Art 1-18Documento3 páginasAlbano Civil Law Barquestions Art 1-18Yelnats DatsimaAinda não há avaliações

- The Story of Atlantis and The Lost Lemuria PDFDocumento61 páginasThe Story of Atlantis and The Lost Lemuria PDFYelnats DatsimaAinda não há avaliações

- Sec 37 Exceptions To Dying DecDocumento18 páginasSec 37 Exceptions To Dying DecYelnats DatsimaAinda não há avaliações

- Cases For Quiz No 21 CivilDocumento1 páginaCases For Quiz No 21 CivilYelnats DatsimaAinda não há avaliações

- Bar QA Civil Law Art 1-18Documento4 páginasBar QA Civil Law Art 1-18Yelnats DatsimaAinda não há avaliações

- Sample Decision Legal WritingDocumento6 páginasSample Decision Legal WritingYelnats DatsimaAinda não há avaliações

- Psychology 101Documento36 páginasPsychology 101Yelnats DatsimaAinda não há avaliações

- Evidence Cases 2-11Documento49 páginasEvidence Cases 2-11Yelnats DatsimaAinda não há avaliações

- Phil Health Care Vs CIRDocumento15 páginasPhil Health Care Vs CIRYelnats DatsimaAinda não há avaliações

- Practice of Law CasesDocumento54 páginasPractice of Law CasesYelnats DatsimaAinda não há avaliações

- CogPsych Chapter 7Documento15 páginasCogPsych Chapter 7Yelnats DatsimaAinda não há avaliações

- UP08 Labor Law 02Documento62 páginasUP08 Labor Law 02jojitus100% (1)

- Pambansang Coalition Vs Exec SecretaryDocumento15 páginasPambansang Coalition Vs Exec SecretaryYelnats DatsimaAinda não há avaliações

- Election Law ReportDocumento24 páginasElection Law ReportYelnats DatsimaAinda não há avaliações

- Labrel Case DigestsDocumento16 páginasLabrel Case DigestsYelnats DatsimaAinda não há avaliações

- Sharia court rules on land title disputeDocumento6 páginasSharia court rules on land title disputeTina TorresAinda não há avaliações

- Oblicon List of CasesDocumento3 páginasOblicon List of CasesRea Jane B. MalcampoAinda não há avaliações

- Belo VS PNBDocumento2 páginasBelo VS PNBGladys Bustria OrlinoAinda não há avaliações

- Research - Civil - Agency Coupled With Interest Basis in Civil CodeDocumento9 páginasResearch - Civil - Agency Coupled With Interest Basis in Civil CodeJunnieson BonielAinda não há avaliações

- 2021 SALES Syllabus-RAR RevisedDocumento57 páginas2021 SALES Syllabus-RAR RevisedJONAH MAE SAMPANGAinda não há avaliações

- Remedial Law Bar Questions 2006-2013Documento38 páginasRemedial Law Bar Questions 2006-2013Ramir FamorcanAinda não há avaliações

- Texas Principles of Real Estate II Final ExamDocumento23 páginasTexas Principles of Real Estate II Final Examandrew kasaineAinda não há avaliações

- Registration of Documents Act SummaryDocumento16 páginasRegistration of Documents Act SummaryJohn kagandaAinda não há avaliações

- ACT NO. 1508: A Collection of Philippine Laws, Statutes and Codes Not Included or Cited in The of TheDocumento4 páginasACT NO. 1508: A Collection of Philippine Laws, Statutes and Codes Not Included or Cited in The of TheRene ValentosAinda não há avaliações

- PCSO Vs New Dagupan (Short Ver)Documento1 páginaPCSO Vs New Dagupan (Short Ver)Von Trotskei PerturbosAinda não há avaliações

- Cred Trans Cases Batch 1Documento131 páginasCred Trans Cases Batch 1Ryan BalladaresAinda não há avaliações

- Requirements and Regulations for Banks and Financial Institutions in the PhilippinesDocumento4 páginasRequirements and Regulations for Banks and Financial Institutions in the PhilippinesJia FriasAinda não há avaliações

- 02 Lopez v. OrosaDocumento2 páginas02 Lopez v. OrosapdasilvaAinda não há avaliações

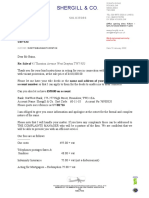

- S00101 Shergill and Co. Client Care Letter 19jul2021 12 38Documento4 páginasS00101 Shergill and Co. Client Care Letter 19jul2021 12 38Sanveer BainsAinda não há avaliações

- Uy Soo Lim Vs Benito Tan Unchuan, Francisca Pastrano and BasilioDocumento44 páginasUy Soo Lim Vs Benito Tan Unchuan, Francisca Pastrano and BasilioNikko ValenzonaAinda não há avaliações

- Metrobank vs S.F. Naguiat EnterprisesDocumento9 páginasMetrobank vs S.F. Naguiat EnterprisesAnty CastilloAinda não há avaliações

- In Re Wilson Memorandum Opinion 07 Apr 2011Documento26 páginasIn Re Wilson Memorandum Opinion 07 Apr 2011William A. Roper Jr.Ainda não há avaliações

- Rule.68.Forem - Movido vs. RFCDocumento1 páginaRule.68.Forem - Movido vs. RFCapple_doctoleroAinda não há avaliações

- China Banking Corp. v. Court of AppealsDocumento6 páginasChina Banking Corp. v. Court of AppealsPrincess Loyola TapiaAinda não há avaliações

- Tax Clearance Certificate Required for Property MortgageDocumento4 páginasTax Clearance Certificate Required for Property MortgageVinod TanwaniAinda não há avaliações

- Rockville v. MirandaDocumento2 páginasRockville v. MirandaDominique Pobe100% (1)

- October 2022 RFBT Preweek Handout Number 1 With Answer Final VersionDocumento16 páginasOctober 2022 RFBT Preweek Handout Number 1 With Answer Final VersionNot ConradAinda não há avaliações

- 5 Navarra Vs Planters BankDocumento15 páginas5 Navarra Vs Planters BankJerric CristobalAinda não há avaliações