Você também pode gostar

- Regenerative Agriculture: Farming with Benefits. Profitable Farms. Healthy Food. Greener Planet. Foreword by Nicolette Hahn Niman.No EverandRegenerative Agriculture: Farming with Benefits. Profitable Farms. Healthy Food. Greener Planet. Foreword by Nicolette Hahn Niman.Ainda não há avaliações

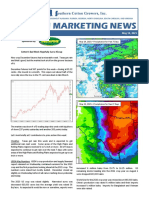

- Cotton Marketing NewsDocumento1 páginaCotton Marketing NewsBrittany EtheridgeAinda não há avaliações

- Focus On Ag (7-22-19)Documento2 páginasFocus On Ag (7-22-19)FluenceMediaAinda não há avaliações

- Cotton Marketing NewsDocumento1 páginaCotton Marketing NewsBrittany EtheridgeAinda não há avaliações

- Focus On Ag (7-23-18)Documento2 páginasFocus On Ag (7-23-18)FluenceMediaAinda não há avaliações

- Cotton Marketing NewsDocumento1 páginaCotton Marketing NewsBrittany EtheridgeAinda não há avaliações

- Cotton Marketing NewsDocumento1 páginaCotton Marketing NewsBrittany EtheridgeAinda não há avaliações

- Focus On Ag (7-08-19)Documento2 páginasFocus On Ag (7-08-19)FluenceMediaAinda não há avaliações

- Focus On Ag: August 26, 2019 2019 Crop Yields Remain A Big QuestionDocumento2 páginasFocus On Ag: August 26, 2019 2019 Crop Yields Remain A Big QuestionFluenceMediaAinda não há avaliações

- Cotton Marketing NewsDocumento1 páginaCotton Marketing NewsBrittany EtheridgeAinda não há avaliações

- Focus On Ag (10-21-19)Documento2 páginasFocus On Ag (10-21-19)FluenceMediaAinda não há avaliações

- Focus On Ag (9-23-19)Documento2 páginasFocus On Ag (9-23-19)FluenceMediaAinda não há avaliações

- South America To Dominate SoybeansDocumento2 páginasSouth America To Dominate SoybeansSamyakAinda não há avaliações

- Cotton Marketing NewsDocumento1 páginaCotton Marketing NewsBrittany EtheridgeAinda não há avaliações

- Cotton Marketing NewsDocumento1 páginaCotton Marketing NewsBrittany EtheridgeAinda não há avaliações

- Cotton Marketing NewsDocumento1 páginaCotton Marketing NewsBrittany EtheridgeAinda não há avaliações

- Focus On Ag (4-15-19)Documento2 páginasFocus On Ag (4-15-19)FluenceMediaAinda não há avaliações

- PEANUT MARKETING NEWS - August 17, 2020 - Tyron Spearman, EditorDocumento1 páginaPEANUT MARKETING NEWS - August 17, 2020 - Tyron Spearman, EditorBrittany EtheridgeAinda não há avaliações

- Focus On Ag: Written by Kent Thiesse Farm Management Analyst and Senior Vice President, Minnstar BankDocumento2 páginasFocus On Ag: Written by Kent Thiesse Farm Management Analyst and Senior Vice President, Minnstar BankFluenceMediaAinda não há avaliações

- Focus On Ag (6-28-21)Documento3 páginasFocus On Ag (6-28-21)FluenceMediaAinda não há avaliações

- Rev CM N 06282019Documento1 páginaRev CM N 06282019Brittany EtheridgeAinda não há avaliações

- Focus On Ag: Written by Kent Thiesse Farm Management Analyst and Vice President, Minnstar BankDocumento2 páginasFocus On Ag: Written by Kent Thiesse Farm Management Analyst and Vice President, Minnstar BankFluenceMediaAinda não há avaliações

- Cotton Marketing NewsDocumento1 páginaCotton Marketing NewsBrittany EtheridgeAinda não há avaliações

- Focus On Ag (6-29-20)Documento2 páginasFocus On Ag (6-29-20)FluenceMediaAinda não há avaliações

- Focus On Ag (5-23-22)Documento3 páginasFocus On Ag (5-23-22)FluenceMediaAinda não há avaliações

- Focus On Ag (6-27-22)Documento3 páginasFocus On Ag (6-27-22)FluenceMediaAinda não há avaliações

- Focus On Ag (6-07-21)Documento2 páginasFocus On Ag (6-07-21)FluenceMediaAinda não há avaliações

- Focus On Ag (8-01-22)Documento2 páginasFocus On Ag (8-01-22)FluenceMediaAinda não há avaliações

- Focus On Ag (7-31-23)Documento2 páginasFocus On Ag (7-31-23)Mike MaybayAinda não há avaliações

- Focus On Ag: October 29, 2018 Harvest Finally Progressing in Late OctoberDocumento2 páginasFocus On Ag: October 29, 2018 Harvest Finally Progressing in Late OctoberFluenceMediaAinda não há avaliações

- Focus On Ag (9-06-21)Documento3 páginasFocus On Ag (9-06-21)FluenceMediaAinda não há avaliações

- Focus On Ag: Written by Kent Thiesse Farm Management Analyst and Senior Vice President, Minnstar BankDocumento2 páginasFocus On Ag: Written by Kent Thiesse Farm Management Analyst and Senior Vice President, Minnstar BankFluenceMediaAinda não há avaliações

- Spring 2020 Agronomy Outlook Mar2020Documento5 páginasSpring 2020 Agronomy Outlook Mar2020Brittany EtheridgeAinda não há avaliações

- Cotton Marketing NewsDocumento1 páginaCotton Marketing NewsBrittany EtheridgeAinda não há avaliações

- Cotton Marketing NewsDocumento1 páginaCotton Marketing NewsBrittany EtheridgeAinda não há avaliações

- Focus On Ag (8-09-21)Documento3 páginasFocus On Ag (8-09-21)FluenceMediaAinda não há avaliações

- Cotton Marketing NewsDocumento1 páginaCotton Marketing NewsBrittany EtheridgeAinda não há avaliações

- Focus On Ag (7-20-20)Documento2 páginasFocus On Ag (7-20-20)FluenceMediaAinda não há avaliações

- Cotton Marketing NewsDocumento1 páginaCotton Marketing NewsBrittany EtheridgeAinda não há avaliações

- Cotton Marketing NewsDocumento1 páginaCotton Marketing NewsBrittany EtheridgeAinda não há avaliações

- Focus On Ag (8-30-21)Documento2 páginasFocus On Ag (8-30-21)FluenceMediaAinda não há avaliações

- Focus On Ag: October 8, 2018 Harvest Season Progressing Slowly in Many AreasDocumento2 páginasFocus On Ag: October 8, 2018 Harvest Season Progressing Slowly in Many AreasFluenceMediaAinda não há avaliações

- Focus On Ag (4-16-18)Documento2 páginasFocus On Ag (4-16-18)FluenceMediaAinda não há avaliações

- Kantar FMCG Pulse March 2023Documento9 páginasKantar FMCG Pulse March 2023ChinmayAinda não há avaliações

- Weekly Cotton Market Review: Vol. 103 No. 26 February 4, 2022Documento9 páginasWeekly Cotton Market Review: Vol. 103 No. 26 February 4, 2022Abbas BananiAinda não há avaliações

- Focus On Ag (8-12-19)Documento2 páginasFocus On Ag (8-12-19)FluenceMediaAinda não há avaliações

- Cotton Marketing NewsDocumento2 páginasCotton Marketing NewsBrittany EtheridgeAinda não há avaliações

- Cotton Marketing NewsDocumento1 páginaCotton Marketing NewsMorgan IngramAinda não há avaliações

- Focus On Ag (6-08-20)Documento2 páginasFocus On Ag (6-08-20)FluenceMediaAinda não há avaliações

- Focus On Ag (7-10-23)Documento2 páginasFocus On Ag (7-10-23)Mike MaybayAinda não há avaliações

- Cotton Marketing NewsDocumento1 páginaCotton Marketing NewsMorgan IngramAinda não há avaliações

- CMN08242020Documento1 páginaCMN08242020Morgan IngramAinda não há avaliações

- Weeklyagreport Weeklyagreport Weeklyagreport Weeklyagreport: Week Ended On Jun. 27, 2013Documento2 páginasWeeklyagreport Weeklyagreport Weeklyagreport Weeklyagreport: Week Ended On Jun. 27, 2013api-164524372Ainda não há avaliações

- Cotton Marketing NewsDocumento2 páginasCotton Marketing NewsMorgan IngramAinda não há avaliações

- 30 Sfu 07 24 19Documento8 páginas30 Sfu 07 24 19nwberryfoundationAinda não há avaliações

- Weeklyagreport Weeklyagreport Weeklyagreport Weeklyagreport: Week Ended On Sep.06, 2012Documento3 páginasWeeklyagreport Weeklyagreport Weeklyagreport Weeklyagreport: Week Ended On Sep.06, 2012api-164524372Ainda não há avaliações

- Ag Puts Up Trade Surplus, But Industry Not Immune To Global Economic WoesDocumento8 páginasAg Puts Up Trade Surplus, But Industry Not Immune To Global Economic Woesapi-26109205Ainda não há avaliações

- USDA Commodity OutlookDocumento28 páginasUSDA Commodity OutlookprasoonragAinda não há avaliações

- Focus On Ag (7-06-20)Documento2 páginasFocus On Ag (7-06-20)FluenceMediaAinda não há avaliações

- PEANUT MARKETING NEWS - September 17, 2020 - Tyron Spearman, EditorDocumento1 páginaPEANUT MARKETING NEWS - September 17, 2020 - Tyron Spearman, EditorMorgan IngramAinda não há avaliações

- Said Jeremy Mayes, General Manager For American Peanut Growers IngredientsDocumento1 páginaSaid Jeremy Mayes, General Manager For American Peanut Growers IngredientsBrittany EtheridgeAinda não há avaliações

- Cotton Marketing NewsDocumento2 páginasCotton Marketing NewsBrittany EtheridgeAinda não há avaliações

- October 17, 2021Documento1 páginaOctober 17, 2021Brittany EtheridgeAinda não há avaliações

- October 24, 2021Documento1 páginaOctober 24, 2021Brittany Etheridge100% (1)

- Cotton Marketing NewsDocumento1 páginaCotton Marketing NewsBrittany EtheridgeAinda não há avaliações

- U.S. PEANUT EXPORTS - TOP 10 - From USDA/Foreign Agricultural Service (American Peanut Council)Documento1 páginaU.S. PEANUT EXPORTS - TOP 10 - From USDA/Foreign Agricultural Service (American Peanut Council)Brittany EtheridgeAinda não há avaliações

- 1,000 Acres Pounds/Acre TonsDocumento1 página1,000 Acres Pounds/Acre TonsBrittany EtheridgeAinda não há avaliações

- Sept. 26, 2021Documento1 páginaSept. 26, 2021Brittany EtheridgeAinda não há avaliações

- Dairy Market Report - September 2021Documento5 páginasDairy Market Report - September 2021Brittany EtheridgeAinda não há avaliações

- World Agricultural Supply and Demand EstimatesDocumento40 páginasWorld Agricultural Supply and Demand EstimatesBrittany EtheridgeAinda não há avaliações

- Shelled MKT Price Weekly Prices: Same As Last Week 7-08-2021 (2020 Crop) 3,318,000 Tons, Up 8.2 % DOWN - $0.4ct/lbDocumento1 páginaShelled MKT Price Weekly Prices: Same As Last Week 7-08-2021 (2020 Crop) 3,318,000 Tons, Up 8.2 % DOWN - $0.4ct/lbBrittany EtheridgeAinda não há avaliações

- Cotton Marketing NewsDocumento1 páginaCotton Marketing NewsBrittany EtheridgeAinda não há avaliações

- October 10, 2021Documento1 páginaOctober 10, 2021Brittany EtheridgeAinda não há avaliações

- Shelled MKT Price Weekly Prices: Same As Last WeekDocumento1 páginaShelled MKT Price Weekly Prices: Same As Last WeekBrittany EtheridgeAinda não há avaliações

- October 3, 2021Documento1 páginaOctober 3, 2021Brittany EtheridgeAinda não há avaliações

- Sept. 12, 2021Documento1 páginaSept. 12, 2021Brittany EtheridgeAinda não há avaliações

- YieldDocumento1 páginaYieldBrittany EtheridgeAinda não há avaliações

- 2021 Export Update - Chinese Future Prices Have Gotten Weaker. This Is Not SurprisingDocumento1 página2021 Export Update - Chinese Future Prices Have Gotten Weaker. This Is Not SurprisingBrittany EtheridgeAinda não há avaliações

- Sept. 19, 2021Documento1 páginaSept. 19, 2021Brittany EtheridgeAinda não há avaliações

- Export Raw-Shelled Peanuts (MT) In-Shell Peanuts (MT) : Down - 11.8 % Down - 16.1%Documento1 páginaExport Raw-Shelled Peanuts (MT) In-Shell Peanuts (MT) : Down - 11.8 % Down - 16.1%Brittany EtheridgeAinda não há avaliações

- Shelled MKT Price Weekly Prices: Same As Last Week 7-08-2021 (2020 Crop) 3,174,075 Tons, Up 3.0 % UP-$01. CT/LBDocumento1 páginaShelled MKT Price Weekly Prices: Same As Last Week 7-08-2021 (2020 Crop) 3,174,075 Tons, Up 3.0 % UP-$01. CT/LBBrittany EtheridgeAinda não há avaliações

- NicholasDocumento1 páginaNicholasBrittany EtheridgeAinda não há avaliações

- August 22, 2021Documento1 páginaAugust 22, 2021Brittany EtheridgeAinda não há avaliações

- Sept. 5, 2021Documento1 páginaSept. 5, 2021Brittany EtheridgeAinda não há avaliações

- World Agricultural Supply and Demand EstimatesDocumento40 páginasWorld Agricultural Supply and Demand EstimatesBrittany EtheridgeAinda não há avaliações

- Shelled MKT Price Weekly Prices: Same As Last Week 7-08-2021 (2020 Crop) 3,318,000 Tons, Up 8.2 % DOWN - $0.4ct/lbDocumento1 páginaShelled MKT Price Weekly Prices: Same As Last Week 7-08-2021 (2020 Crop) 3,318,000 Tons, Up 8.2 % DOWN - $0.4ct/lbBrittany EtheridgeAinda não há avaliações

- FPAC Honeybee Brochure August2021Documento4 páginasFPAC Honeybee Brochure August2021Brittany EtheridgeAinda não há avaliações

- Shelled MKT Price Weekly Prices: Same As Last Week 7-08-2021 (2020 Crop) 3,318,000 Tons, Up 8.2 % DOWN - $0.6ct/lbDocumento1 páginaShelled MKT Price Weekly Prices: Same As Last Week 7-08-2021 (2020 Crop) 3,318,000 Tons, Up 8.2 % DOWN - $0.6ct/lbBrittany EtheridgeAinda não há avaliações

- August 29, 2021Documento1 páginaAugust 29, 2021Brittany EtheridgeAinda não há avaliações

- Export Raw-Shelled Peanuts (MT) In-Shell Peanuts (MT) : Down - 10.8 % Down - 15.0%Documento1 páginaExport Raw-Shelled Peanuts (MT) In-Shell Peanuts (MT) : Down - 10.8 % Down - 15.0%Brittany EtheridgeAinda não há avaliações

- 35 Childrens BooksDocumento4 páginas35 Childrens Booksapi-710628938Ainda não há avaliações

- Internship Final Students CircularDocumento1 páginaInternship Final Students CircularAdi TyaAinda não há avaliações

- Sencor-Scooter-One-App-EN YeaaDocumento7 páginasSencor-Scooter-One-App-EN Yeaaeh smrdimAinda não há avaliações

- Students and Sports Betting in Nigeria (2020)Documento57 páginasStudents and Sports Betting in Nigeria (2020)Nwaozuru JOHNMAJOR Chinecherem100% (1)

- (Digest) Marcos II V CADocumento7 páginas(Digest) Marcos II V CAGuiller C. MagsumbolAinda não há avaliações

- Deadlands - Hell On Earth - BrainburnersDocumento129 páginasDeadlands - Hell On Earth - BrainburnersKS100% (1)

- G.R. No. L-6393 January 31, 1955 A. MAGSAYSAY INC., Plaintiff-Appellee, ANASTACIO AGAN, Defendant-AppellantDocumento64 páginasG.R. No. L-6393 January 31, 1955 A. MAGSAYSAY INC., Plaintiff-Appellee, ANASTACIO AGAN, Defendant-AppellantAerylle GuraAinda não há avaliações

- CrackJPSC Mains Paper III Module A HistoryDocumento172 páginasCrackJPSC Mains Paper III Module A HistoryL S KalundiaAinda não há avaliações

- ObliconDocumento3 páginasObliconMonica Medina100% (2)

- David - sm15 - Inppt - 01Documento33 páginasDavid - sm15 - Inppt - 01ibeAinda não há avaliações

- Determinate and GenericDocumento5 páginasDeterminate and GenericKlara Alcaraz100% (5)

- Ebook4Expert Ebook CollectionDocumento42 páginasEbook4Expert Ebook CollectionSoumen Paul0% (1)

- Alcpt 27R (Script)Documento21 páginasAlcpt 27R (Script)Matt Dahiam RinconAinda não há avaliações

- Dax CowartDocumento26 páginasDax CowartAyu Anisa GultomAinda não há avaliações

- Assignment 10Documento2 páginasAssignment 10Kristina KittyAinda não há avaliações

- Politics of BelgiumDocumento19 páginasPolitics of BelgiumSaksham AroraAinda não há avaliações

- Walt DisneyDocumento56 páginasWalt DisneyDaniela Denisse Anthawer Luna100% (6)

- Nivea Case StudyDocumento15 páginasNivea Case StudyShreyas LigadeAinda não há avaliações

- FY2011 Sked CDocumento291 páginasFY2011 Sked CSunnyside PostAinda não há avaliações

- Faith in GenesisDocumento5 páginasFaith in Genesischris iyaAinda não há avaliações

- A Comparison of The Manual Electoral System and The Automated Electoral System in The PhilippinesDocumento42 páginasA Comparison of The Manual Electoral System and The Automated Electoral System in The PhilippineschaynagirlAinda não há avaliações

- Player's Guide: by Patrick RenieDocumento14 páginasPlayer's Guide: by Patrick RenieDominick Bryant100% (4)

- BPM at Hindustan Coca Cola Beverages - NMIMS, MumbaiDocumento10 páginasBPM at Hindustan Coca Cola Beverages - NMIMS, MumbaiMojaAinda não há avaliações

- Social Inequality and ExclusionDocumento3 páginasSocial Inequality and ExclusionAnurag Agrawal0% (1)

- Motion To Compel Further Discovery Responses From Fannie MaeDocumento71 páginasMotion To Compel Further Discovery Responses From Fannie MaeLee Perry100% (4)

- Boone Pickens' Leadership PlanDocumento2 páginasBoone Pickens' Leadership PlanElvie PradoAinda não há avaliações

- Forn VännenDocumento14 páginasForn VännenDana KoopAinda não há avaliações

- Grandparents 2Documento13 páginasGrandparents 2api-288503311Ainda não há avaliações

- Randy C de Lara 2.1Documento2 páginasRandy C de Lara 2.1Jane ParaisoAinda não há avaliações

- Lea3 Final ExamDocumento4 páginasLea3 Final ExamTfig Fo EcaepAinda não há avaliações