Você também pode gostar

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (120)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- EEOC v. CostcoDocumento5 páginasEEOC v. CostcoFortuneAinda não há avaliações

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Test Final ExamDocumento17 páginasTest Final ExambedollaprincessAinda não há avaliações

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Evidence Outline (Harthill)Documento66 páginasEvidence Outline (Harthill)beezy23100% (3)

- Deed of Extrajudicial Settlement of Estate With Absolute SaleDocumento5 páginasDeed of Extrajudicial Settlement of Estate With Absolute SalealbycadavisAinda não há avaliações

- Good Governance CompleteDocumento19 páginasGood Governance CompleteKaleem MarwatAinda não há avaliações

- BA Finance Corp V. CA (ATP)Documento2 páginasBA Finance Corp V. CA (ATP)k santosAinda não há avaliações

- Whitney v. RobertsonDocumento4 páginasWhitney v. RobertsonTessa TacataAinda não há avaliações

- JURIS BELLA - Impacts of Multinational Corporations On The StateDocumento5 páginasJURIS BELLA - Impacts of Multinational Corporations On The StateSyazana JamalAinda não há avaliações

- Working OverseasDocumento1 páginaWorking OverseasSyazana JamalAinda não há avaliações

- Substantial PerformanceDocumento1 páginaSubstantial PerformanceSyazana JamalAinda não há avaliações

- Similarities and Differences of The Issue in Malaysian Law and Common LawDocumento2 páginasSimilarities and Differences of The Issue in Malaysian Law and Common LawSyazana JamalAinda não há avaliações

- Kartinee's Part. You Have To Tell The Tribunal About The Strike That Happened at Your MineDocumento6 páginasKartinee's Part. You Have To Tell The Tribunal About The Strike That Happened at Your MineSyazana JamalAinda não há avaliações

- PBLDocumento1 páginaPBLSyazana JamalAinda não há avaliações

- TestDocumento15 páginasTestSyazana JamalAinda não há avaliações

- TestDocumento15 páginasTestSyazana JamalAinda não há avaliações

- TestDocumento15 páginasTestSyazana JamalAinda não há avaliações

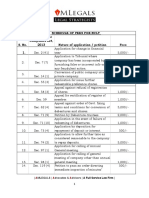

- Schedule of Fees in NCLT 1Documento4 páginasSchedule of Fees in NCLT 1Lavkesh BhambhaniAinda não há avaliações

- Code of Conduct - MetvyDocumento5 páginasCode of Conduct - MetvyCherryberryAinda não há avaliações

- Special Power of AttorneyDocumento6 páginasSpecial Power of AttorneyPdean DeanAinda não há avaliações

- AIPPMDocumento15 páginasAIPPMNaman ShahAinda não há avaliações

- Eo Badac Reorganization 2018Documento2 páginasEo Badac Reorganization 2018Rolando Lagat50% (2)

- SSR Case EvidenceDocumento3 páginasSSR Case EvidenceLourd SandeshAinda não há avaliações

- Loadstar Shipping Co., Inc., Petitioner, vs. Court of Appeals and The Manila INSURANCE CO., INC., RespondentsDocumento10 páginasLoadstar Shipping Co., Inc., Petitioner, vs. Court of Appeals and The Manila INSURANCE CO., INC., RespondentsJoan ChristineAinda não há avaliações

- Gujarat Victim Compensation Scheme 2013Documento5 páginasGujarat Victim Compensation Scheme 2013Latest Laws TeamAinda não há avaliações

- Tax Mates - 10. Concurrence by A Majority of All The Members of Congress Fo160134 PDFDocumento2 páginasTax Mates - 10. Concurrence by A Majority of All The Members of Congress Fo160134 PDFSandyAinda não há avaliações

- Guidelines and Updates On The Registration of TSCDocumento57 páginasGuidelines and Updates On The Registration of TSCAr-Ar ToledoAinda não há avaliações

- AADocumento10 páginasAAChristopher PerazAinda não há avaliações

- History ReportDocumento3 páginasHistory ReportJustin BalicatAinda não há avaliações

- Frivaldo Vs ComelecDocumento28 páginasFrivaldo Vs ComelecCzarina Victoria L. CominesAinda não há avaliações

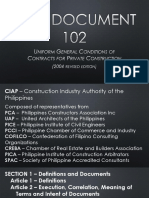

- 5 Ciap Document 102Documento8 páginas5 Ciap Document 102Kessler BiatingoAinda não há avaliações

- Luzon Brokerage v. Maritime Building, 43 SCRA 93, January 21, 1972Documento18 páginasLuzon Brokerage v. Maritime Building, 43 SCRA 93, January 21, 1972Eszle Ann L. ChuaAinda não há avaliações

- Case Doctrines Evidence Ni RedeemDocumento10 páginasCase Doctrines Evidence Ni RedeempulithepogiAinda não há avaliações

- Hunter Brittain AffidavitDocumento3 páginasHunter Brittain AffidavitTHV11 DigitalAinda não há avaliações

- Final Supplementary Report 4Documento33 páginasFinal Supplementary Report 4Upamanyu HazarikaAinda não há avaliações

- Northside V Anthem Legal Dispute April 13 RulingDocumento7 páginasNorthside V Anthem Legal Dispute April 13 RulingJonathan Raymond100% (1)

- Exhibit A-3Documento7 páginasExhibit A-3IR Tribunal - vexatious 3Ainda não há avaliações

- Diane Neal Ruling 9-18-18 PDFDocumento3 páginasDiane Neal Ruling 9-18-18 PDFDaily FreemanAinda não há avaliações

- Caltex vs. Sulpicio LinesDocumento6 páginasCaltex vs. Sulpicio LinesaudreyAinda não há avaliações

- Token Option Plan ( (Draft) )Documento20 páginasToken Option Plan ( (Draft) )Luigi FelicianoAinda não há avaliações