Você também pode gostar

- Project Gul UBLDocumento71 páginasProject Gul UBLShabnam NazAinda não há avaliações

- Ankita's Summer Project ReportDocumento29 páginasAnkita's Summer Project ReportKamal More100% (7)

- Dedicated: To My Loving Parents, Family AND Respectable TeachersDocumento39 páginasDedicated: To My Loving Parents, Family AND Respectable TeachersTalha Iftekhar Khan SwatiAinda não há avaliações

- The Bank of KhyberDocumento83 páginasThe Bank of Khybernocent_dvil88% (8)

- Introduction To Report Background of The StudyDocumento42 páginasIntroduction To Report Background of The StudyMuhammad ShahzadAinda não há avaliações

- Assignment On NCC BankDocumento44 páginasAssignment On NCC Bankhasan633100% (1)

- UBL Internship ReportDocumento43 páginasUBL Internship ReportWasif JamalAinda não há avaliações

- NCC Bank ReportDocumento54 páginasNCC Bank ReportSumon Shopnil100% (1)

- Study of NPA in UCO BankDocumento63 páginasStudy of NPA in UCO BankSunil Shekhar Nayak0% (1)

- INTERNSHIP REPORT On UBLDocumento22 páginasINTERNSHIP REPORT On UBLNour E HuddaAinda não há avaliações

- HBL Final ReportDocumento31 páginasHBL Final ReportAamir KhanAinda não há avaliações

- Internship Report On NBP, Civil Line Branch, Sargodha, (2010)Documento69 páginasInternship Report On NBP, Civil Line Branch, Sargodha, (2010)Malik AyaanAinda não há avaliações

- UBL ReportDocumento86 páginasUBL ReportadnanirshadAinda não há avaliações

- Project Report ON "To Study of Npa Management"Documento64 páginasProject Report ON "To Study of Npa Management"Dhiraj KokareAinda não há avaliações

- United Bank Limited Layyah Branch, Layyah: Bzu Bahadur Sub Campus LayyahDocumento22 páginasUnited Bank Limited Layyah Branch, Layyah: Bzu Bahadur Sub Campus LayyahZIA UL REHMANAinda não há avaliações

- Project Report ON "To Study of Npa Management": Rode Santosh FakiraDocumento67 páginasProject Report ON "To Study of Npa Management": Rode Santosh FakiraTejashree GadhaveAinda não há avaliações

- Sir. Shabir Ahmad Tariq Aziz: Supervised byDocumento52 páginasSir. Shabir Ahmad Tariq Aziz: Supervised byMohib Ullah YousafzaiAinda não há avaliações

- A Research Report ON Service Quality AND Customer Satisfaction of Kotak Mahindra BankDocumento88 páginasA Research Report ON Service Quality AND Customer Satisfaction of Kotak Mahindra BankchaudharinitinAinda não há avaliações

- Chapter-1 Internship Report On Bank of KhyberDocumento37 páginasChapter-1 Internship Report On Bank of KhyberAhmad AliAinda não há avaliações

- 1.0 Introduction To The StudyDocumento63 páginas1.0 Introduction To The StudySharifMahmud100% (1)

- Introduction To Report: 1.1. Background of StudyDocumento40 páginasIntroduction To Report: 1.1. Background of StudyTalha Iftekhar Khan SwatiAinda não há avaliações

- "General Banking in Bangladesh" - A Study Based On First Security Islami Bank Ltd.Documento53 páginas"General Banking in Bangladesh" - A Study Based On First Security Islami Bank Ltd.SharifMahmudAinda não há avaliações

- Ayesha Internship 2 PDFDocumento59 páginasAyesha Internship 2 PDFAisha rashidAinda não há avaliações

- Chapter-1: 1.2 Background of The Study 1.3 Objective of The Study 1.4 Methodology of The Report 1.5 LimitationDocumento76 páginasChapter-1: 1.2 Background of The Study 1.3 Objective of The Study 1.4 Methodology of The Report 1.5 LimitationZoheb21Ainda não há avaliações

- 11111report 4 BankDocumento51 páginas11111report 4 BankSarmad PirzadaAinda não há avaliações

- Credit Analysis of Rupali Bank Ltd.Documento61 páginasCredit Analysis of Rupali Bank Ltd.Emran Haidar NiloyAinda não há avaliações

- DBBL Mobile BankingDocumento32 páginasDBBL Mobile BankingSha SAinda não há avaliações

- Project Report On "Net Banking System" Post GraduateDocumento15 páginasProject Report On "Net Banking System" Post Graduateeafat shahinAinda não há avaliações

- MCB ReportDocumento80 páginasMCB ReportAminullah DawarAinda não há avaliações

- Executive SummaryDocumento59 páginasExecutive SummarywaqarAinda não há avaliações

- General Banking Activities of Sonali BanDocumento56 páginasGeneral Banking Activities of Sonali BanKazi Abu SayeedAinda não há avaliações

- Comparative Analysis of Non Performing AssetsDocumento64 páginasComparative Analysis of Non Performing Assetsagoyal88100% (1)

- NBP by A SaboorDocumento69 páginasNBP by A SaboorAta Ullah MukhlisAinda não há avaliações

- Introduction To The ReportDocumento34 páginasIntroduction To The ReportTalha Iftekhar Khan SwatiAinda não há avaliações

- Chapter 1: Introduction: 1.1 Origin of The ReportDocumento43 páginasChapter 1: Introduction: 1.1 Origin of The ReportHossain Mohammad NeaziAinda não há avaliações

- Internship Report On IFIC BankDocumento85 páginasInternship Report On IFIC BankMonjurul AlamAinda não há avaliações

- Origin of Report:: Chapter-1Documento81 páginasOrigin of Report:: Chapter-1Pushpa BaruaAinda não há avaliações

- General Banking and Loan System of IFIC Bank LimitedDocumento40 páginasGeneral Banking and Loan System of IFIC Bank LimitedFaquir Sanoar SanyAinda não há avaliações

- Internship Report 2Documento20 páginasInternship Report 2Ahmad AliAinda não há avaliações

- ReportDocumento74 páginasReportShaukat KhanAinda não há avaliações

- Internship ReportDocumento43 páginasInternship ReportsakibarsAinda não há avaliações

- Ahmer Report FinaldsfdfDocumento55 páginasAhmer Report FinaldsfdfZaheer Ahmed SwatiAinda não há avaliações

- Mustafa AhmadDocumento70 páginasMustafa Ahmadwaqar ahmadAinda não há avaliações

- NBL Internship ReportDocumento129 páginasNBL Internship ReportMohammad Anamul HoqueAinda não há avaliações

- Mansoor Ihsan ReportDocumento70 páginasMansoor Ihsan ReportSherzada KhanAinda não há avaliações

- Corporation Bank Report FinalDocumento61 páginasCorporation Bank Report FinalJasmandeep brarAinda não há avaliações

- NBL Export-Import ContributionDocumento41 páginasNBL Export-Import Contributionrezwan_haque_2Ainda não há avaliações

- HBL Report 1Documento83 páginasHBL Report 1Muhammad RiazAinda não há avaliações

- Albaraka ReportDocumento54 páginasAlbaraka ReportMoon StarAinda não há avaliações

- Chapter - 1 Introduction of The ReportDocumento57 páginasChapter - 1 Introduction of The Reportfr.faisal8265Ainda não há avaliações

- Chapter-1: 1.1 Introduction of The ReportDocumento24 páginasChapter-1: 1.1 Introduction of The Reportbany_dhakaAinda não há avaliações

- Part 3Documento50 páginasPart 3himelAinda não há avaliações

- Lucknow Model Institute of Management, Lucknow: Summer Training Project Report ONDocumento88 páginasLucknow Model Institute of Management, Lucknow: Summer Training Project Report ONManjeet SinghAinda não há avaliações

- Final Report of NBPDocumento92 páginasFinal Report of NBPGulEFarisFarisAinda não há avaliações

- Regional Rural Banks of India: Evolution, Performance and ManagementNo EverandRegional Rural Banks of India: Evolution, Performance and ManagementAinda não há avaliações

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)No EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)Ainda não há avaliações

- Banking India: Accepting Deposits for the Purpose of LendingNo EverandBanking India: Accepting Deposits for the Purpose of LendingAinda não há avaliações

- The role of banks in the regional economic development of Uzbekistan: lessons from the German experienceNo EverandThe role of banks in the regional economic development of Uzbekistan: lessons from the German experienceAinda não há avaliações

- Working Capital Management and FinanceNo EverandWorking Capital Management and FinanceNota: 3.5 de 5 estrelas3.5/5 (8)

- Financial Analysis: 3.1. Consolidated Statement of Financial PositionDocumento14 páginasFinancial Analysis: 3.1. Consolidated Statement of Financial PositionTalha Iftekhar Khan SwatiAinda não há avaliações

- Summer Internship Project Report: BY Sadam Rafique ROLL NO: 37443 Bba (Hons) MarketingDocumento41 páginasSummer Internship Project Report: BY Sadam Rafique ROLL NO: 37443 Bba (Hons) MarketingTalha Iftekhar Khan SwatiAinda não há avaliações

- Internship Report On Askari Bank Limited Upper Adha Branch MuzaffarabadDocumento48 páginasInternship Report On Askari Bank Limited Upper Adha Branch MuzaffarabadTalha Iftekhar Khan SwatiAinda não há avaliações

- Saji DDDD DDDDDocumento37 páginasSaji DDDD DDDDTalha Iftekhar Khan SwatiAinda não há avaliações

- Faizan KhanDocumento59 páginasFaizan KhanTalha Iftekhar Khan SwatiAinda não há avaliações

- Internship Report On Pakistan Telecommunication Company Limited, MansehraDocumento56 páginasInternship Report On Pakistan Telecommunication Company Limited, MansehraTalha Iftekhar Khan SwatiAinda não há avaliações

- Introduction To Report: 1.1. Background of StudyDocumento40 páginasIntroduction To Report: 1.1. Background of StudyTalha Iftekhar Khan SwatiAinda não há avaliações

- Kaleem Saifullah: Faculty ResumeDocumento2 páginasKaleem Saifullah: Faculty ResumeTalha Iftekhar Khan SwatiAinda não há avaliações

- Intern Feedback Form: 3/26/2018 PM Youth Internship ProgramDocumento2 páginasIntern Feedback Form: 3/26/2018 PM Youth Internship ProgramTalha Iftekhar Khan SwatiAinda não há avaliações

- Ahmed Final ReportDocumento54 páginasAhmed Final ReportTalha Iftekhar Khan SwatiAinda não há avaliações

- Internship Report On Pakistan Telecommunication Company Limited, MansehraDocumento53 páginasInternship Report On Pakistan Telecommunication Company Limited, MansehraTalha Iftekhar Khan SwatiAinda não há avaliações

- Atta Ullah Shah 35307Documento30 páginasAtta Ullah Shah 35307Talha Iftekhar Khan SwatiAinda não há avaliações

- Introduction To The ReportDocumento34 páginasIntroduction To The ReportTalha Iftekhar Khan SwatiAinda não há avaliações

- Sumera AskariDocumento33 páginasSumera AskariTalha Iftekhar Khan SwatiAinda não há avaliações

- Profile NIDA-Pakistan UpdatedDocumento8 páginasProfile NIDA-Pakistan UpdatedTalha Iftekhar Khan SwatiAinda não há avaliações

- DedicationDocumento3 páginasDedicationTalha Iftekhar Khan SwatiAinda não há avaliações

- RMIT International University VietnamDocumento32 páginasRMIT International University VietnamMahi SahanaAinda não há avaliações

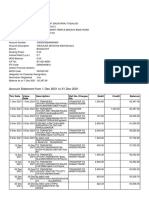

- Account Statement From 1 Mar 2023 To 31 Mar 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocumento3 páginasAccount Statement From 1 Mar 2023 To 31 Mar 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceSuresh VatipalliAinda não há avaliações

- Bank of Ireland App User GuideDocumento8 páginasBank of Ireland App User GuideMostafa HamoudaAinda não há avaliações

- TOPFLYTECH TLW1-10A (E) Vehicle GPS Tracker: User ManualDocumento16 páginasTOPFLYTECH TLW1-10A (E) Vehicle GPS Tracker: User ManualSaulius StasysAinda não há avaliações

- TR-900 ATC Guide - v1.1Documento264 páginasTR-900 ATC Guide - v1.1Emanuel Von AnkhAinda não há avaliações

- Hospital Management System Use Case Diagram ExampleDocumento10 páginasHospital Management System Use Case Diagram Examplebooks_sumi33% (3)

- Home Loan/Lap Application Form: Customer Name: Loan Agreement No.Documento16 páginasHome Loan/Lap Application Form: Customer Name: Loan Agreement No.Shashikant JoshiAinda não há avaliações

- Customer Request FormDocumento1 páginaCustomer Request Formnkmadnani2008Ainda não há avaliações

- The German eID-Card by Jens BenderDocumento42 páginasThe German eID-Card by Jens BenderPoomjit SirawongprasertAinda não há avaliações

- ATM Complaint FormDocumento1 páginaATM Complaint FormPalacio JeromeAinda não há avaliações

- Mobile Banking and Internet BankingDocumento10 páginasMobile Banking and Internet BankingNeeraj DwivediAinda não há avaliações

- Momo Terms ConditionsDocumento10 páginasMomo Terms ConditionsUWIMBABAZI AdelineAinda não há avaliações

- FASTest For ATMs Training GuideDocumento136 páginasFASTest For ATMs Training GuideSelma Citra NirmalaAinda não há avaliações

- Secure Atm Using Card Scan....... ProjectDocumento8 páginasSecure Atm Using Card Scan....... ProjectCH Abdul RahmanAinda não há avaliações

- Banking ...Documento8 páginasBanking ...Ashwani KumarAinda não há avaliações

- 3.5.7 Lab - Social Engineering - ILMDocumento2 páginas3.5.7 Lab - Social Engineering - ILMMario Alberto Saavedra MeridaAinda não há avaliações

- Automated Teller Machine Using C++Documento76 páginasAutomated Teller Machine Using C++S BOSEAinda não há avaliações

- Day-To-Day Banking Companion Booklet PDFDocumento59 páginasDay-To-Day Banking Companion Booklet PDFowen tsangAinda não há avaliações

- AUZao 3 IPv 2 LR 2 AZIDocumento7 páginasAUZao 3 IPv 2 LR 2 AZIrajarao001Ainda não há avaliações

- Siemens SITRANS LR110 ManualDocumento62 páginasSiemens SITRANS LR110 ManualThanachai TengjirathanapaAinda não há avaliações

- STAR ISO 8583 Message Format Guide 02-11Documento374 páginasSTAR ISO 8583 Message Format Guide 02-11bill_w8508140% (5)

- Account Statement From 1 Dec 2021 To 31 Dec 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocumento2 páginasAccount Statement From 1 Dec 2021 To 31 Dec 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balanceprashant tadalagiAinda não há avaliações

- NCR AtmDocumento54 páginasNCR Atmchanito0007Ainda não há avaliações

- Security and Hacking (As Time Allows) : Module: Application Development and Emerging Technologies-Cc05Documento9 páginasSecurity and Hacking (As Time Allows) : Module: Application Development and Emerging Technologies-Cc05jerico gaspanAinda não há avaliações

- Codificación para Envio de TramasDocumento149 páginasCodificación para Envio de TramasAlison VelascoAinda não há avaliações

- Banking System Case Study 1 Problem DescriptionDocumento5 páginasBanking System Case Study 1 Problem DescriptionMeAinda não há avaliações

- Sailor FBB 500 User ManualDocumento183 páginasSailor FBB 500 User ManualNikita Ryabchuk100% (1)

- User Manual: 1. Application and Basic FunctionDocumento14 páginasUser Manual: 1. Application and Basic Functionmohammad hazbehzadAinda não há avaliações

- HUAWEI Y9 2019 User Guide (JKM-LX1&LX2&LX3, EMUI8.2 - 01, English, Normal) PDFDocumento108 páginasHUAWEI Y9 2019 User Guide (JKM-LX1&LX2&LX3, EMUI8.2 - 01, English, Normal) PDFSwirtyAinda não há avaliações

- Know Your Rupay Debit CardDocumento9 páginasKnow Your Rupay Debit Cardwps gccAinda não há avaliações