Você também pode gostar

- Anglo US ModelDocumento12 páginasAnglo US ModelArjay De Luna100% (1)

- Business EnvironmentDocumento25 páginasBusiness Environmenthasb97Ainda não há avaliações

- Benefits of Joint Stock CompanyDocumento2 páginasBenefits of Joint Stock CompanyMaria ShahidAinda não há avaliações

- OB Tutorial Question TopicsDocumento12 páginasOB Tutorial Question TopicsAnnalisa PatrickAinda não há avaliações

- Job Analysis Is Conducted To Determine TheDocumento14 páginasJob Analysis Is Conducted To Determine TheMarkmarilynAinda não há avaliações

- Regulatory Framework of AuditingDocumento18 páginasRegulatory Framework of AuditingSohaib BilalAinda não há avaliações

- Chapter 7 Liabilities of AuditorsDocumento25 páginasChapter 7 Liabilities of AuditorsVinamra AgrawalAinda não há avaliações

- Accounting SummaryDocumento12 páginasAccounting SummarysaraAinda não há avaliações

- 1.strategic Management - The Traditional ApproachDocumento3 páginas1.strategic Management - The Traditional ApproachMuhammad Usman Ashraf0% (1)

- Accounting Standard (As) 21Documento13 páginasAccounting Standard (As) 21Ajay GhotiaAinda não há avaliações

- Qualification of An Auditor 2Documento8 páginasQualification of An Auditor 2sidraayaz_84Ainda não há avaliações

- Sample Performance AppraisalDocumento6 páginasSample Performance AppraisalReeces EwartAinda não há avaliações

- HR Audit SMU MU0013Documento8 páginasHR Audit SMU MU0013Abdullah AzadAinda não há avaliações

- ch11 - Fundamentals of Organizing - 50Documento40 páginasch11 - Fundamentals of Organizing - 50Rand Qatawneh100% (1)

- Sunaina Ratio AnalysisDocumento90 páginasSunaina Ratio AnalysisGaurav SharmaAinda não há avaliações

- Auditing NotesDocumento65 páginasAuditing NotesTushar GaurAinda não há avaliações

- Business Environment Lecture Notes 1 5 PDFDocumento10 páginasBusiness Environment Lecture Notes 1 5 PDFPoudel SathiAinda não há avaliações

- AUDIT BasicDocumento10 páginasAUDIT BasicKingo StreamAinda não há avaliações

- Edp NotesDocumento48 páginasEdp NotesSantosh SunnyAinda não há avaliações

- Role of Auditors in Corporate GovernanceDocumento9 páginasRole of Auditors in Corporate GovernanceDevansh SrivastavaAinda não há avaliações

- The History of Origin and Growth of Merchant Banking Throughout The WorldDocumento18 páginasThe History of Origin and Growth of Merchant Banking Throughout The WorldJeegar Shah0% (1)

- Chapter 8 Lecture NotesDocumento7 páginasChapter 8 Lecture NotesnightdazeAinda não há avaliações

- Factors Influencing BEDocumento10 páginasFactors Influencing BEcecilAinda não há avaliações

- Aging and Its Effect On The Teaching-Learning ProcessDocumento25 páginasAging and Its Effect On The Teaching-Learning ProcessnangungunaAinda não há avaliações

- Advisor Recruitment in Icici PrudentialDocumento23 páginasAdvisor Recruitment in Icici PrudentialIsrar MahiAinda não há avaliações

- Audit Case Study AGODocumento5 páginasAudit Case Study AGOAlifah SalwaAinda não há avaliações

- Factors Influencing Corporate GovernanceDocumento5 páginasFactors Influencing Corporate GovernanceShariq Ansari MAinda não há avaliações

- Bonus Plan HypothesisDocumento2 páginasBonus Plan HypothesisShamsinaz Mat IsaAinda não há avaliações

- 11 Business Studies Notes Ch02 Forms of Business Organisation 2Documento10 páginas11 Business Studies Notes Ch02 Forms of Business Organisation 2Srishti SoniAinda não há avaliações

- MCS-Responsibility Centres & Profit CentresDocumento24 páginasMCS-Responsibility Centres & Profit CentresAnand KansalAinda não há avaliações

- Week 7Documento7 páginasWeek 7SanjeevParajuliAinda não há avaliações

- Colleg Factors On Assessment of Non PerfoDocumento67 páginasColleg Factors On Assessment of Non Perfodaniel nugusieAinda não há avaliações

- Title of The Paper:: Mergers and Acquisitions Financial ManagementDocumento25 páginasTitle of The Paper:: Mergers and Acquisitions Financial ManagementfatinAinda não há avaliações

- Eab30903 - Acounting Theory and Practices Assignment 3 REPORT - ONLINE SUBMISSION (30/12/2020)Documento3 páginasEab30903 - Acounting Theory and Practices Assignment 3 REPORT - ONLINE SUBMISSION (30/12/2020)Muhd ArifAinda não há avaliações

- Unit - 4 Study Material ACGDocumento21 páginasUnit - 4 Study Material ACGAbhijeet UpadhyayAinda não há avaliações

- The Theory and Practice of Corporate GovernanceDocumento25 páginasThe Theory and Practice of Corporate GovernanceMadihaBhatti100% (1)

- Lecture 6 Strategic Analysis and Choice ImportantDocumento34 páginasLecture 6 Strategic Analysis and Choice ImportantSarsal6067Ainda não há avaliações

- 1.2 Corporate Accounting PDFDocumento6 páginas1.2 Corporate Accounting PDFRech MJAinda não há avaliações

- Definition of Joint Stock CompanyDocumento2 páginasDefinition of Joint Stock CompanyGhalib HussainAinda não há avaliações

- ForecastingDocumento81 páginasForecastingangelica joyce caballesAinda não há avaliações

- PPM-Notes-Unit II-Evolution of Management ThoughtDocumento23 páginasPPM-Notes-Unit II-Evolution of Management ThoughtNilabjo Kanti PaulAinda não há avaliações

- Auditing Notes.18Documento37 páginasAuditing Notes.18sasikumarthanus100% (1)

- Key Aspects of Corporate Organization, Operating PoliciesDocumento25 páginasKey Aspects of Corporate Organization, Operating PoliciesHanz E. Bollozos88% (8)

- Company Incorporation JapanDocumento4 páginasCompany Incorporation JapanParas MittalAinda não há avaliações

- Competitive AdvantageDocumento16 páginasCompetitive AdvantageakashAinda não há avaliações

- Tutorial 1 Regulatory & Conceptual FrameworkDocumento11 páginasTutorial 1 Regulatory & Conceptual FrameworkLAVINNYA NAIR A P PARBAKARANAinda não há avaliações

- Solved - United Technologies Corporation (UTC), Based in Hartfor...Documento4 páginasSolved - United Technologies Corporation (UTC), Based in Hartfor...Saad ShafiqAinda não há avaliações

- Factoring Advantages and Dis AdvantagesDocumento1 páginaFactoring Advantages and Dis AdvantagesSiva RockAinda não há avaliações

- Managing The Finance FunctionDocumento17 páginasManaging The Finance FunctionMa-marts OfilandaAinda não há avaliações

- Presentation Audit Auditors ChallengesDocumento11 páginasPresentation Audit Auditors ChallengesghazieAinda não há avaliações

- Stakeholder Theory: Chapter Two: Theories of NgosDocumento20 páginasStakeholder Theory: Chapter Two: Theories of NgoswubeAinda não há avaliações

- Book Multiple Choice QuestionsDocumento10 páginasBook Multiple Choice Questionszitorocksmyheart0% (1)

- Answers of Assignment Questions of Compensation ManagementDocumento16 páginasAnswers of Assignment Questions of Compensation ManagementBaqirZarAinda não há avaliações

- Topic 1 Introduction To Corporate FinanceDocumento26 páginasTopic 1 Introduction To Corporate FinancelelouchAinda não há avaliações

- Role and Responsibilities of Independent DirectorsDocumento31 páginasRole and Responsibilities of Independent DirectorsLavina ChandwaniAinda não há avaliações

- International Strategic Management A Complete Guide - 2020 EditionNo EverandInternational Strategic Management A Complete Guide - 2020 EditionAinda não há avaliações

- Risk Based Internal Audit A Complete Guide - 2020 EditionNo EverandRisk Based Internal Audit A Complete Guide - 2020 EditionAinda não há avaliações

- Investigation into the Adherence to Corporate Governance in Zimbabwe’s SME SectorNo EverandInvestigation into the Adherence to Corporate Governance in Zimbabwe’s SME SectorAinda não há avaliações

- Value Chain Management Capability A Complete Guide - 2020 EditionNo EverandValue Chain Management Capability A Complete Guide - 2020 EditionAinda não há avaliações

- Models of Corporate GovernanceDocumento27 páginasModels of Corporate Governancekristine valerie BonghanoyAinda não há avaliações

- The Negotiable Instruments Law PDFDocumento29 páginasThe Negotiable Instruments Law PDFJesterAinda não há avaliações

- Quatech 123Documento38 páginasQuatech 123JesterAinda não há avaliações

- Quatech 123Documento38 páginasQuatech 123JesterAinda não há avaliações

- Models of Corporate GovernanceDocumento5 páginasModels of Corporate GovernanceJesterAinda não há avaliações

- QuatechDocumento19 páginasQuatechJesterAinda não há avaliações

- Institutional Investors, Governance Organizations & Legal InitiativesDocumento10 páginasInstitutional Investors, Governance Organizations & Legal InitiativesJesterAinda não há avaliações

- Sast Regulations, 2011Documento28 páginasSast Regulations, 2011Ekansh TiwariAinda não há avaliações

- Quiz in ELEC 01 (Inventory Estimation)Documento3 páginasQuiz in ELEC 01 (Inventory Estimation)djanine cardinalesAinda não há avaliações

- Gray Company S Financial Statements Showed Income Before Income Taxes ofDocumento1 páginaGray Company S Financial Statements Showed Income Before Income Taxes ofFreelance WorkerAinda não há avaliações

- Tax Return of Individuals AssesseDocumento19 páginasTax Return of Individuals AssesseShahidul IslamAinda não há avaliações

- Corporate Liquidation DisDocumento4 páginasCorporate Liquidation DisRenelyn DavidAinda não há avaliações

- Guide To Private EquityDocumento68 páginasGuide To Private Equityarundalk100% (14)

- Mutual Fund AssignmentDocumento7 páginasMutual Fund AssignmentBhargav PathakAinda não há avaliações

- Financial Forecasting SCI PDFDocumento29 páginasFinancial Forecasting SCI PDFMa. Lou Erika BALITEAinda não há avaliações

- Ulip Multimeter: Power House of Information For All ULIP PLANSDocumento33 páginasUlip Multimeter: Power House of Information For All ULIP PLANSjay18Ainda não há avaliações

- 2024 Training Calendarpdf - 1706278302Documento86 páginas2024 Training Calendarpdf - 1706278302ojopaulkehindeAinda não há avaliações

- 54940bosmtpsr2 Inter p1 QDocumento6 páginas54940bosmtpsr2 Inter p1 QAryan GurjarAinda não há avaliações

- Ross 12e PPT Ch08Documento37 páginasRoss 12e PPT Ch08Qusai BassamAinda não há avaliações

- My ProjectDocumento99 páginasMy Projectmosee geeAinda não há avaliações

- Account StatementDocumento12 páginasAccount StatementRAJU KISHAN LALAinda não há avaliações

- EBA Recommendation On The Creation and Supervisory Oversight of Temporary Capital Buffers To Restore Market Confidence (EBA/REC/2011/1)Documento22 páginasEBA Recommendation On The Creation and Supervisory Oversight of Temporary Capital Buffers To Restore Market Confidence (EBA/REC/2011/1)EKAI CenterAinda não há avaliações

- Swisstek (Ceylon) PLC Swisstek (Ceylon) PLCDocumento7 páginasSwisstek (Ceylon) PLC Swisstek (Ceylon) PLCkasun witharanaAinda não há avaliações

- Accounting For Corporation - Activity AssignmentDocumento12 páginasAccounting For Corporation - Activity AssignmentXiu MinAinda não há avaliações

- Laporan Keuangan TA 2021Documento225 páginasLaporan Keuangan TA 2021Ahmad subAinda não há avaliações

- Case Analysis FinanlDocumento7 páginasCase Analysis FinanlTasnova AalamAinda não há avaliações

- Questions 2Documento12 páginasQuestions 2venice cambryAinda não há avaliações

- CH 11Documento94 páginasCH 11JesussAinda não há avaliações

- Accounting Standards in The East Asia Region: By: M. Zubaidur RahmanDocumento16 páginasAccounting Standards in The East Asia Region: By: M. Zubaidur Rahmanemerson deasisAinda não há avaliações

- Corporate Governance All Exam Papers QSDocumento6 páginasCorporate Governance All Exam Papers QSAdnan Karim33% (3)

- Worksheet To Principle of Acc. II. AregaDocumento4 páginasWorksheet To Principle of Acc. II. AregaEtiel Films / ኢትኤል ፊልሞች100% (3)

- Case Study Capital BudgetingDocumento13 páginasCase Study Capital BudgetingHazellethAinda não há avaliações

- Quiz 2 SolDocumento56 páginasQuiz 2 SolVikram GulatiAinda não há avaliações

- Examiner's Report: F9 Financial Management December 2011Documento5 páginasExaminer's Report: F9 Financial Management December 2011Saad HassanAinda não há avaliações

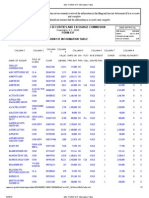

- SEC FORM 13-F Information TableDocumento7 páginasSEC FORM 13-F Information TableBecket AdamsAinda não há avaliações

- ACCO 30023 - Accounting For Business Combination (IM)Documento74 páginasACCO 30023 - Accounting For Business Combination (IM)rachel banana hammockAinda não há avaliações

- LUYONG - 3rd Periodical - FABM1Documento4 páginasLUYONG - 3rd Periodical - FABM1Jonavi Luyong100% (2)