Você também pode gostar

- A Comparative Analysis of Tax Administration in Asia and the Pacific: 2016 EditionNo EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: 2016 EditionAinda não há avaliações

- A. B. C. D. E.: Capital Costs, Operating Costs, Revenue, Depreciation, and Residual ValueDocumento30 páginasA. B. C. D. E.: Capital Costs, Operating Costs, Revenue, Depreciation, and Residual ValueAfroz AlamAinda não há avaliações

- BA4202 Capital Budgeting Solved ProblemsDocumento10 páginasBA4202 Capital Budgeting Solved ProblemsVasugi KumarAinda não há avaliações

- BA4202 Capital Budgeting Solved ProblemsDocumento9 páginasBA4202 Capital Budgeting Solved ProblemsVasugi KumarAinda não há avaliações

- Bora Assignment FinalDocumento12 páginasBora Assignment FinalBora AslanAinda não há avaliações

- Corporate Finance 22vaCRTlVYrpDocumento8 páginasCorporate Finance 22vaCRTlVYrpAdityaSinghAinda não há avaliações

- Solution of Tutorial 6Documento4 páginasSolution of Tutorial 6Richard MidgleyAinda não há avaliações

- Financial EvaluationDocumento5 páginasFinancial EvaluationAbebe GetanehAinda não há avaliações

- Corporate FinanceDocumento8 páginasCorporate Financedivyakashyapbharat1Ainda não há avaliações

- 9 - Chapter-7-Discounted-Cashflow-Techniques-with-AnswerDocumento15 páginas9 - Chapter-7-Discounted-Cashflow-Techniques-with-AnswerMd SaifulAinda não há avaliações

- Financial Management Session 10Documento20 páginasFinancial Management Session 10vaidehirajput03Ainda não há avaliações

- BDM AssignmentDocumento11 páginasBDM AssignmenttatualynaAinda não há avaliações

- Evaluating TechniquesDocumento13 páginasEvaluating TechniquesMario YyyyAinda não há avaliações

- Internal Assignment - Corporate FinanceDocumento9 páginasInternal Assignment - Corporate FinancePradeep KumawatAinda não há avaliações

- Financial Management Note 9Documento28 páginasFinancial Management Note 9Jonathan LimAinda não há avaliações

- Further Practice On Interim Test (Soln)Documento4 páginasFurther Practice On Interim Test (Soln)Lê ĐạtAinda não há avaliações

- Business Decision Making Payback Period and Net Present Value EvaluationDocumento6 páginasBusiness Decision Making Payback Period and Net Present Value Evaluationnawal zaheerAinda não há avaliações

- Corporate Finance LOS 36Documento26 páginasCorporate Finance LOS 36RamAinda não há avaliações

- Financial Management Session 10Documento11 páginasFinancial Management Session 10Shivangi MohpalAinda não há avaliações

- Financial Management Session 11Documento17 páginasFinancial Management Session 11vaidehirajput03Ainda não há avaliações

- 13 - Chapter4 - Capital Budgeting - Part2Documento9 páginas13 - Chapter4 - Capital Budgeting - Part2com01156499073Ainda não há avaliações

- Me 5.4 RMDocumento12 páginasMe 5.4 RMPawan NayakAinda não há avaliações

- Chapter 5Documento25 páginasChapter 5Ephrem ChernetAinda não há avaliações

- Solution: Year Cash Inflows Present Value Factor Present Value $ @10% $Documento10 páginasSolution: Year Cash Inflows Present Value Factor Present Value $ @10% $Waylee CheroAinda não há avaliações

- BBF 321Documento10 páginasBBF 321sipanjegivenAinda não há avaliações

- Corporate Finance JUNE 2022Documento7 páginasCorporate Finance JUNE 2022Rajni KumariAinda não há avaliações

- Chapter 4 Capital Budgeting Techniques 2021 - Practice ProblemsDocumento20 páginasChapter 4 Capital Budgeting Techniques 2021 - Practice ProblemsAkshat SinghAinda não há avaliações

- Fin Strategy Ass 1Documento3 páginasFin Strategy Ass 1mqondisi nkabindeAinda não há avaliações

- Girum Tsega PerfectDocumento13 páginasGirum Tsega PerfectMesi YE GIAinda não há avaliações

- Class 5 Project Selection ExerciseDocumento18 páginasClass 5 Project Selection ExerciseVinodshankar BhatAinda não há avaliações

- Credit Appraisal - Project RiskDocumento30 páginasCredit Appraisal - Project RisksabetaliAinda não há avaliações

- Capital Budgeting - NotesDocumento171 páginasCapital Budgeting - NotesSiddharth mehtaAinda não há avaliações

- Management Information CLASS (L-03 & 04) : Prepared By: A.K.M Mesbahul Karim FCADocumento28 páginasManagement Information CLASS (L-03 & 04) : Prepared By: A.K.M Mesbahul Karim FCASohag KhanAinda não há avaliações

- Ty SPM L7Documento15 páginasTy SPM L7sanilAinda não há avaliações

- Topic 8 - Inv App 1 Ans 2019-20Documento4 páginasTopic 8 - Inv App 1 Ans 2019-20Gaba RieleAinda não há avaliações

- Final Mock1 - AnswerDocumento7 páginasFinal Mock1 - AnswerK58 Hà Phương LinhAinda não há avaliações

- Further Practice On Interim Test (Soln)Documento4 páginasFurther Practice On Interim Test (Soln)Lê ĐạtAinda não há avaliações

- Capital Budgeting MathDocumento3 páginasCapital Budgeting MathMD.TARIQUL ISLAM CHOWDHURYAinda não há avaliações

- Capital Budgeting: Presenting byDocumento18 páginasCapital Budgeting: Presenting bymuhammad usamaAinda não há avaliações

- Accounting and Financial Management-ProjectDocumento8 páginasAccounting and Financial Management-ProjectMelokuhle MhlongoAinda não há avaliações

- Chapter 12Documento14 páginasChapter 12Naimmul FahimAinda não há avaliações

- Discussions Updated 24.03Documento28 páginasDiscussions Updated 24.03rajawatswadheentaAinda não há avaliações

- Capital Budgeting HandoutsDocumento13 páginasCapital Budgeting HandoutsCoke Aidenry SaludoAinda não há avaliações

- Managerial Economics (Chapter 14)Documento28 páginasManagerial Economics (Chapter 14)api-3703724100% (1)

- Corporate Finance: Capital BudgetingDocumento29 páginasCorporate Finance: Capital BudgetingPigeons LoftAinda não há avaliações

- Assignment 4 - Cost of Capital and Capital BudgetiDocumento5 páginasAssignment 4 - Cost of Capital and Capital BudgetiBrian AlalaAinda não há avaliações

- Capital BudgetingDocumento25 páginasCapital BudgetingAnkit JindalAinda não há avaliações

- MA Practice Paper 1 Question 2 SolutionDocumento6 páginasMA Practice Paper 1 Question 2 SolutionRiteeka UdaniAinda não há avaliações

- Chapter 46 Investment AppraisalDocumento4 páginasChapter 46 Investment AppraisalAbdur RafayAinda não há avaliações

- Aug 2015 Question 4 - Topic 1: Introduction To FMGTDocumento4 páginasAug 2015 Question 4 - Topic 1: Introduction To FMGTSharleen ZxzAinda não há avaliações

- WACC & PaybackDocumento9 páginasWACC & PaybackBelle Dela CruzAinda não há avaliações

- FM Crash Course Material 111Documento65 páginasFM Crash Course Material 111Safwan Abdul GafoorAinda não há avaliações

- Capital Budgeting MathDocumento4 páginasCapital Budgeting MathMuhammad Akmal HossainAinda não há avaliações

- Capital Budgeting PPT2Documento24 páginasCapital Budgeting PPT2Sumit BhAinda não há avaliações

- 2 - CH 16 (ICAP Book) - Introduction To Project Appraisal - FinalDocumento93 páginas2 - CH 16 (ICAP Book) - Introduction To Project Appraisal - FinalArslanAinda não há avaliações

- Short-Term ExamDocumento6 páginasShort-Term Examymkuzangwe16Ainda não há avaliações

- Net Present Value: Time Value of MoneyDocumento4 páginasNet Present Value: Time Value of MoneyChris tine Mae MendozaAinda não há avaliações

- Solved Finance IssuesDocumento16 páginasSolved Finance IssuesrytchluvAinda não há avaliações

- Problems 7Documento4 páginasProblems 7jojAinda não há avaliações

- VND Openxmlformats-Officedocument Wordprocessingml Document&rendition 1Documento4 páginasVND Openxmlformats-Officedocument Wordprocessingml Document&rendition 1Rohit Singh RajputAinda não há avaliações

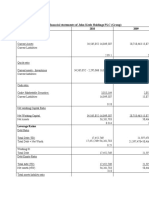

- Ratio Analysis On Financial Statements of John Keels Holdings PLC (Group)Documento11 páginasRatio Analysis On Financial Statements of John Keels Holdings PLC (Group)Shesha Nimna GamageAinda não há avaliações

- Year - Capacity Utilization (%)Documento1 páginaYear - Capacity Utilization (%)Shesha Nimna GamageAinda não há avaliações

- Correct AnswersDocumento2 páginasCorrect AnswersShesha Nimna GamageAinda não há avaliações

- Working Capital ManagementDocumento2 páginasWorking Capital ManagementShesha Nimna GamageAinda não há avaliações

- AssetsDocumento2 páginasAssetsShesha Nimna GamageAinda não há avaliações

- Higher Return of CapitalDocumento10 páginasHigher Return of CapitalShesha Nimna GamageAinda não há avaliações

- 1.1. Importance of Working Capital ManagementDocumento7 páginas1.1. Importance of Working Capital ManagementShesha Nimna GamageAinda não há avaliações

- Annual Statistics 2018Documento21 páginasAnnual Statistics 2018Shesha Nimna GamageAinda não há avaliações

- 1.1 The Importance of Working Capital Management Working Capitalit Is The Capital Used To Run The Day-To-Day Business Operations. Usually, The GapDocumento11 páginas1.1 The Importance of Working Capital Management Working Capitalit Is The Capital Used To Run The Day-To-Day Business Operations. Usually, The GapShesha Nimna GamageAinda não há avaliações

- Financial Audit Process: Terms of EngagementDocumento1 páginaFinancial Audit Process: Terms of EngagementShesha Nimna GamageAinda não há avaliações

- Blended Learning Desing For ACF 201Documento2 páginasBlended Learning Desing For ACF 201Shesha Nimna GamageAinda não há avaliações

- Machine Fault Detection Using Vibration Signal Peak DetectorDocumento31 páginasMachine Fault Detection Using Vibration Signal Peak Detectordavison coyAinda não há avaliações

- HST TrainingDocumento11 páginasHST TrainingRamesh BabuAinda não há avaliações

- HPC168 Passenger CounterDocumento9 páginasHPC168 Passenger CounterRommel GómezAinda não há avaliações

- An Experimental Analysis of Clustering Algorithms in Data Mining Using Weka ToolDocumento6 páginasAn Experimental Analysis of Clustering Algorithms in Data Mining Using Weka Toolmishranamit2211Ainda não há avaliações

- Naca 4412Documento3 páginasNaca 4412Selva KumarAinda não há avaliações

- 417 Model E Alarm Check ValvesDocumento4 páginas417 Model E Alarm Check ValvesM Kumar MarimuthuAinda não há avaliações

- Pre Calculus MIdTermsDocumento5 páginasPre Calculus MIdTermsLamette Austria Ayong0% (1)

- Research FinalDocumento29 páginasResearch FinalLaw VesperaAinda não há avaliações

- Ss 1 Further Mathematics Lesson 4Documento7 páginasSs 1 Further Mathematics Lesson 4Adio Babatunde Abiodun CabaxAinda não há avaliações

- SD02 Introduction SDBMSDocumento26 páginasSD02 Introduction SDBMSgatothp100% (2)

- Assignment - 1 Introduction of Machines and Mechanisms: TheoryDocumento23 páginasAssignment - 1 Introduction of Machines and Mechanisms: TheoryAman AmanAinda não há avaliações

- Form in MusicDocumento8 páginasForm in MusicAndri KurniawanAinda não há avaliações

- Awards Gold Medals Grade VIDocumento11 páginasAwards Gold Medals Grade VIBernadeth Escosora DolorAinda não há avaliações

- Ra 6938Documento2 páginasRa 6938GaryAinda não há avaliações

- T8 - Energetics IDocumento28 páginasT8 - Energetics II Kadek Irvan Adistha PutraAinda não há avaliações

- Javascript Html5 CanavasDocumento13 páginasJavascript Html5 CanavasmihailuAinda não há avaliações

- ElectrolysisDocumento3 páginasElectrolysisRaymond ChanAinda não há avaliações

- Computer Graphics: Overview of Graphics SystemsDocumento25 páginasComputer Graphics: Overview of Graphics Systemsshibina balakrishnanAinda não há avaliações

- Application Note Usrp and HDSDR Spectrum MonitoringDocumento14 páginasApplication Note Usrp and HDSDR Spectrum MonitoringcaraboyAinda não há avaliações

- Best Approach: Compound AngleDocumento8 páginasBest Approach: Compound AngleAbhiyanshu KumarAinda não há avaliações

- CraneDocumento71 páginasCranesunder_kumar280% (1)

- V7R3 Recovery Guide Sc415304Documento560 páginasV7R3 Recovery Guide Sc415304gort400Ainda não há avaliações

- 23AE23 DS enDocumento4 páginas23AE23 DS enBhageerathi SahuAinda não há avaliações

- Design of Helical Pier Foundations in Frozen GroundDocumento6 páginasDesign of Helical Pier Foundations in Frozen GroundCortesar ManuAinda não há avaliações

- 新型重油催化裂化催化剂RCC 1的研究开发Documento5 páginas新型重油催化裂化催化剂RCC 1的研究开发Anca DumitruAinda não há avaliações

- PR100 BrochureDocumento28 páginasPR100 Brochuregus289Ainda não há avaliações

- Leonardo Romero SR High School: Republic of The Philippines Region Xii - Soccsksargen Schools Division Office of CotabatoDocumento4 páginasLeonardo Romero SR High School: Republic of The Philippines Region Xii - Soccsksargen Schools Division Office of CotabatoDulce M. LupaseAinda não há avaliações

- Demag KBK Alu Enclosed Track SystemDocumento2 páginasDemag KBK Alu Enclosed Track SystemMAGSTAinda não há avaliações

- 6100 SQ Lcms Data SheetDocumento4 páginas6100 SQ Lcms Data Sheet王皓Ainda não há avaliações

- XG5000 Manual (2009.10.26) (Eng)Documento645 páginasXG5000 Manual (2009.10.26) (Eng)wanderly_40100% (1)

- Getting to Yes: How to Negotiate Agreement Without Giving InNo EverandGetting to Yes: How to Negotiate Agreement Without Giving InNota: 4 de 5 estrelas4/5 (652)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)No EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Nota: 4.5 de 5 estrelas4.5/5 (15)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNNo Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNNota: 4.5 de 5 estrelas4.5/5 (3)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindNo EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindNota: 5 de 5 estrelas5/5 (231)

- John D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthNo EverandJohn D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthNota: 4 de 5 estrelas4/5 (20)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaNo EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaNota: 4.5 de 5 estrelas4.5/5 (14)

- A Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineNo EverandA Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineAinda não há avaliações

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsNo EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsNota: 5 de 5 estrelas5/5 (1)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!No EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Nota: 4.5 de 5 estrelas4.5/5 (14)

- SAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsNo EverandSAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsAinda não há avaliações

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)No EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Nota: 4.5 de 5 estrelas4.5/5 (5)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisNo EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisNota: 5 de 5 estrelas5/5 (6)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaNo EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaNota: 3.5 de 5 estrelas3.5/5 (8)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingNo EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingNota: 4.5 de 5 estrelas4.5/5 (17)

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)No EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Nota: 4 de 5 estrelas4/5 (33)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesAinda não há avaliações

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNo EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialAinda não há avaliações

- Ready, Set, Growth hack:: A beginners guide to growth hacking successNo EverandReady, Set, Growth hack:: A beginners guide to growth hacking successNota: 4.5 de 5 estrelas4.5/5 (93)

- Accounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCNo EverandAccounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCNota: 5 de 5 estrelas5/5 (1)

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsNo EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsNota: 4 de 5 estrelas4/5 (7)

- An easy approach to trading with bollinger bands: How to learn how to use Bollinger bands to trade online successfullyNo EverandAn easy approach to trading with bollinger bands: How to learn how to use Bollinger bands to trade online successfullyNota: 3 de 5 estrelas3/5 (1)

- Overcoming Underearning(TM): A Simple Guide to a Richer LifeNo EverandOvercoming Underearning(TM): A Simple Guide to a Richer LifeNota: 4 de 5 estrelas4/5 (21)