Você também pode gostar

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- BCA DetailsDocumento30 páginasBCA DetailsNip ChenAinda não há avaliações

- Bidding Zone Screen ShotsDocumento17 páginasBidding Zone Screen ShotsNip ChenAinda não há avaliações

- Online Bidding ReportDocumento85 páginasOnline Bidding ReportNip ChenAinda não há avaliações

- Online Auction System: Software RequirementsDocumento2 páginasOnline Auction System: Software RequirementsSusan RainAinda não há avaliações

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (119)

- GSK Patient Assistance Program Non-Vaccine Application: For Questions On How To Complete This Form, Call 1-866-728-4368Documento4 páginasGSK Patient Assistance Program Non-Vaccine Application: For Questions On How To Complete This Form, Call 1-866-728-4368Jhoanna MonterolaAinda não há avaliações

- Acct Statement XX5581 01062023Documento2 páginasAcct Statement XX5581 01062023Desai AbhishekAinda não há avaliações

- Supplier Invoice To Payment Flow ModelDocumento1 páginaSupplier Invoice To Payment Flow ModelSweater GeekAinda não há avaliações

- Manage Cash Flow with a Two-Column Cash BookDocumento5 páginasManage Cash Flow with a Two-Column Cash BookAdika Denish0% (1)

- Starter Activity Digi Tech Year 10 PresentationDocumento24 páginasStarter Activity Digi Tech Year 10 Presentationevdokiiatolluman77Ainda não há avaliações

- Audit Plan Tests Financial StatementsDocumento27 páginasAudit Plan Tests Financial StatementsAbdul Malik FajriAinda não há avaliações

- Travel Demand Forecasting I. Trip GenerationDocumento5 páginasTravel Demand Forecasting I. Trip GenerationJaper WeakAinda não há avaliações

- Data Aadt Car 2018Documento5 páginasData Aadt Car 2018HUBERT FILOGAinda não há avaliações

- This Study Resource Was: Audit Test 3 Study Guide HW 5 Cash ArDocumento5 páginasThis Study Resource Was: Audit Test 3 Study Guide HW 5 Cash ArheyAinda não há avaliações

- Audit MeheheDocumento4 páginasAudit Mehehejamaira haridAinda não há avaliações

- Hotel Pre Opening Full ChecklistDocumento24 páginasHotel Pre Opening Full ChecklistDeo Patria HerdriantoAinda não há avaliações

- HW On Cash BDocumento6 páginasHW On Cash BAngelo123Ainda não há avaliações

- PTIT 2022 Mobile NetworkDocumento54 páginasPTIT 2022 Mobile NetworkTuân Nguyễn XuânAinda não há avaliações

- University of Santo Tomas Alfredo M. Velayo College of AccountancyDocumento4 páginasUniversity of Santo Tomas Alfredo M. Velayo College of AccountancyChni Gals0% (1)

- Libby Chap 5Documento13 páginasLibby Chap 5hatanolove100% (1)

- Updated HBL-Gauri-AqsaDocumento6 páginasUpdated HBL-Gauri-AqsaAbdul Moiz YousfaniAinda não há avaliações

- Inventory and Purchase Order ReceiptsDocumento51 páginasInventory and Purchase Order ReceiptsPriya NimmagaddaAinda não há avaliações

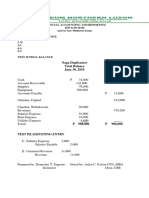

- Financial Accounting and Reporting Midterm Exam KeyDocumento4 páginasFinancial Accounting and Reporting Midterm Exam KeyDonita Joy T. EugenioAinda não há avaliações

- Big BazaarDocumento19 páginasBig BazaarAlok RanjanAinda não há avaliações

- Lect - 9: Migrating Into A Cloud (Broad Approaches To Migrating Into The Cloud)Documento17 páginasLect - 9: Migrating Into A Cloud (Broad Approaches To Migrating Into The Cloud)JayeshS CS:CZ GamingAinda não há avaliações

- Bill GazDocumento1 páginaBill GazNawfal RakrakiAinda não há avaliações

- PDFDocumento7 páginasPDFJitendra KumarAinda não há avaliações

- Royal G 11 IDocumento6 páginasRoyal G 11 IScribd UserAinda não há avaliações

- St. Mary's University: E-Marketing Term Paper E-DistributionDocumento6 páginasSt. Mary's University: E-Marketing Term Paper E-DistributionSovii BehablaAinda não há avaliações

- Unit 7 Channels of DistributionDocumento14 páginasUnit 7 Channels of DistributionKritika RajAinda não há avaliações

- tpdv100 Trading Places International Brendan Bucks OfferDocumento2 páginastpdv100 Trading Places International Brendan Bucks Offerapi-232026023Ainda não há avaliações

- KONUS-Flyer+2017 EnglischDocumento2 páginasKONUS-Flyer+2017 EnglischSoumi Bandyopadhyay SBAinda não há avaliações

- Curriculum Vitae: Shaikh Mohammed AdnanDocumento4 páginasCurriculum Vitae: Shaikh Mohammed AdnanSHAIKH MOHD ADNANAinda não há avaliações

- Quiz #2 Accounting FundamentalsDocumento3 páginasQuiz #2 Accounting FundamentalsJohn Rey Bantay RodriguezAinda não há avaliações

- 13A074Documento15 páginas13A074Naveen MeenaAinda não há avaliações