Você também pode gostar

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

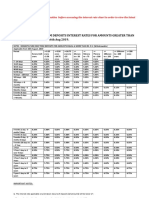

- HDFC RatesDocumento4 páginasHDFC RatesdesikanttAinda não há avaliações

- A Study of The Cost of Production of Apples in Shimla District of Himachal PradeshDocumento6 páginasA Study of The Cost of Production of Apples in Shimla District of Himachal PradeshdesikanttAinda não há avaliações

- Cub Letter of OfferDocumento145 páginasCub Letter of OfferdesikanttAinda não há avaliações

- Holy MenDocumento8 páginasHoly MendesikanttAinda não há avaliações

- British Debt PolicyDocumento36 páginasBritish Debt PolicydesikanttAinda não há avaliações

- Kashmir StruggleDocumento48 páginasKashmir StruggledesikanttAinda não há avaliações

- RBI Monetary Policy 2019Documento14 páginasRBI Monetary Policy 2019desikanttAinda não há avaliações

- Senior Citizens Free Bus PassDocumento1 páginaSenior Citizens Free Bus PassdesikanttAinda não há avaliações

- Sancharam PDFDocumento1 páginaSancharam PDFdesikanttAinda não há avaliações

- Date DAY Tamilmonth & Date Departure From Apporox Time Arrival at Approx Time RemarksDocumento3 páginasDate DAY Tamilmonth & Date Departure From Apporox Time Arrival at Approx Time RemarksdesikanttAinda não há avaliações

- Dewan Housing Finance Corporation LTD.: in Case of Debenture Holder, Other Than IndividualDocumento1 páginaDewan Housing Finance Corporation LTD.: in Case of Debenture Holder, Other Than IndividualdesikanttAinda não há avaliações

- Power FinanceDocumento2 páginasPower FinancedesikanttAinda não há avaliações

- Anbe Arule - Chapter 4Documento8 páginasAnbe Arule - Chapter 4Mahesh KrishnamoorthyAinda não há avaliações

- Best 5 Mid Cap Stocks To BuyDocumento13 páginasBest 5 Mid Cap Stocks To BuydesikanttAinda não há avaliações

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Lesson 6 Tax On Natural ResourcesDocumento43 páginasLesson 6 Tax On Natural ResourcesakpanyapAinda não há avaliações

- Cir V Cta GR No 106611, July 21, 1994 FactsDocumento39 páginasCir V Cta GR No 106611, July 21, 1994 FactsAnonymous r1cRm7FAinda não há avaliações

- The Value of Synergy: Aswath Damodaran 1Documento33 páginasThe Value of Synergy: Aswath Damodaran 1Abhishek SinhaAinda não há avaliações

- 6 Coca-Cola Vs CCBPIDocumento5 páginas6 Coca-Cola Vs CCBPINunugom SonAinda não há avaliações

- Inctax 2Documento45 páginasInctax 2janeferrarin551Ainda não há avaliações

- Module 3 Individual Taxpayers 1Documento8 páginasModule 3 Individual Taxpayers 1Chryshelle Anne Marie LontokAinda não há avaliações

- Guidelines For Investment Proof Submission 2023-2024Documento7 páginasGuidelines For Investment Proof Submission 2023-2024rajdelhi000Ainda não há avaliações

- Chapter 3 Payaroll - Wubex-2Documento8 páginasChapter 3 Payaroll - Wubex-2Birhanu FelekeAinda não há avaliações

- CIT, Kolkata V Smifs SecuritiesDocumento4 páginasCIT, Kolkata V Smifs SecuritiesBar & BenchAinda não há avaliações

- Slump SaleDocumento19 páginasSlump SaleGeetika AnandAinda não há avaliações

- Essentials of Federal Taxation 3rd Edition Spilker Test BankDocumento67 páginasEssentials of Federal Taxation 3rd Edition Spilker Test Bankdilysiristtes5Ainda não há avaliações

- PGBP NotesDocumento24 páginasPGBP NotesYogesh Aggarwal100% (2)

- Income Tax On Individuals - Ust PDFDocumento15 páginasIncome Tax On Individuals - Ust PDFKana Lou Cassandra Besana100% (1)

- Uniform System of AccountsDocumento102 páginasUniform System of Accountsashraf0% (1)

- INCOME TAX UpdatedDocumento94 páginasINCOME TAX UpdatedTrishAinda não há avaliações

- Income Taxation and Income Tax: Atty. Cleo D. Sabado-Andrada, Cpa, MbaDocumento52 páginasIncome Taxation and Income Tax: Atty. Cleo D. Sabado-Andrada, Cpa, MbaMaan0% (2)

- Vicente Madrigal and His WifeDocumento21 páginasVicente Madrigal and His WifesonskiAinda não há avaliações

- Becker CPA Review Summary of Changes Included in The V1.1 REG TextbookDocumento16 páginasBecker CPA Review Summary of Changes Included in The V1.1 REG Textbookmohit2ucAinda não há avaliações

- Salary Slip - June 2022 - UnlockedDocumento2 páginasSalary Slip - June 2022 - UnlockedRmillionsque FinserveAinda não há avaliações

- HI5020 Corporate Accounting: 12c - A Review SessionDocumento17 páginasHI5020 Corporate Accounting: 12c - A Review SessionFeku RamAinda não há avaliações

- J.B. Pritzker 2022 Federal ReturnDocumento8 páginasJ.B. Pritzker 2022 Federal ReturnRobert Garcia100% (1)

- Tax Implications of Amalgamations / Mergers / Demergers / Slump SalesDocumento54 páginasTax Implications of Amalgamations / Mergers / Demergers / Slump Salesvvikram756667% (3)

- Summary Philippine Income Tax FormulaDocumento25 páginasSummary Philippine Income Tax FormulaDonvidachiye Liwag CenaAinda não há avaliações

- Scheme of Amalgmation of GDA Technologies Limited With Larsen & Toubro InfoTech Limited (Company Update)Documento20 páginasScheme of Amalgmation of GDA Technologies Limited With Larsen & Toubro InfoTech Limited (Company Update)Shyam SunderAinda não há avaliações

- Fringe Benefit TaxDocumento9 páginasFringe Benefit TaxBusiness MatterAinda não há avaliações

- G.R. No. L-28896 February 17, 1988 Commissioner of Internal Revenue, Petitioner, ALGUE, INC., and THE COURT OF TAX APPEALS, Respondents. CRUZ, J.Documento2 páginasG.R. No. L-28896 February 17, 1988 Commissioner of Internal Revenue, Petitioner, ALGUE, INC., and THE COURT OF TAX APPEALS, Respondents. CRUZ, J.Robehgene Atud-JavinarAinda não há avaliações

- United States v. Felix Benitez Rexach, 482 F.2d 10, 1st Cir. (1973)Documento28 páginasUnited States v. Felix Benitez Rexach, 482 F.2d 10, 1st Cir. (1973)Scribd Government Docs100% (1)

- 194C - Non Deduction of TDS For TransporterDocumento1 página194C - Non Deduction of TDS For TransporterDINESH MEHTAAinda não há avaliações

- Taxation Challenge - With Answer KeyDocumento9 páginasTaxation Challenge - With Answer Keyariaseg100% (1)

- CasesDocumento24 páginasCasesXuan LieuAinda não há avaliações