Você também pode gostar

- Cash in Hand Pattoki 1 To 23 Aug-21Documento18 páginasCash in Hand Pattoki 1 To 23 Aug-21Farhan Khan MarwatAinda não há avaliações

- SPPL Gen LedgerDocumento428 páginasSPPL Gen LedgerFarhan Khan MarwatAinda não há avaliações

- SPPL ConsDocumento61 páginasSPPL ConsFarhan Khan MarwatAinda não há avaliações

- Subject: Authority Letter For Collection of Bank Statement: (Authorized Signatory) (Authorized Signatory)Documento1 páginaSubject: Authority Letter For Collection of Bank Statement: (Authorized Signatory) (Authorized Signatory)Farhan Khan MarwatAinda não há avaliações

- Income Tax Notes Income Tax Notes: Income Tax Law (University of Sindh) Income Tax Law (University of Sindh)Documento44 páginasIncome Tax Notes Income Tax Notes: Income Tax Law (University of Sindh) Income Tax Law (University of Sindh)Farhan Khan MarwatAinda não há avaliações

- Forensic Psychology Lecture NotesDocumento38 páginasForensic Psychology Lecture NotesFarhan Khan Marwat100% (1)

- Mcqs For Research Methodology in PsychologyDocumento31 páginasMcqs For Research Methodology in PsychologyFarhan Khan MarwatAinda não há avaliações

- Express TribuneDocumento12 páginasExpress TribuneFarhan Khan MarwatAinda não há avaliações

- Motherboard Cpu Network Interface Card Random-Access Memory (Ram) Modules Hardware Internal (HDDS)Documento5 páginasMotherboard Cpu Network Interface Card Random-Access Memory (Ram) Modules Hardware Internal (HDDS)Farhan Khan MarwatAinda não há avaliações

- Who Is A WorkmanDocumento23 páginasWho Is A WorkmanFarhan Khan MarwatAinda não há avaliações

- Capital BudgetingDocumento6 páginasCapital BudgetingFarhan Khan MarwatAinda não há avaliações

- Abbottabad Zone: Funds Remitted by Head OfficeDocumento34 páginasAbbottabad Zone: Funds Remitted by Head OfficeFarhan Khan MarwatAinda não há avaliações

- Monday Tuesday Wednesday Change Thursday Friday Saturday: SundayDocumento4 páginasMonday Tuesday Wednesday Change Thursday Friday Saturday: SundayFarhan Khan MarwatAinda não há avaliações

- Chapter 15 Budgeting Profit Sales Cost ExpensesDocumento19 páginasChapter 15 Budgeting Profit Sales Cost ExpensesFarhan Khan MarwatAinda não há avaliações

- c6 Question Bank PDFDocumento25 páginasc6 Question Bank PDFFarhan Khan MarwatAinda não há avaliações

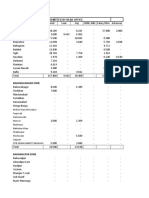

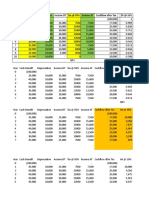

- Year Cash Benefit Depreciation Income BT Tax at 50% Income AT Cashflow After Tax DF at 10%Documento6 páginasYear Cash Benefit Depreciation Income BT Tax at 50% Income AT Cashflow After Tax DF at 10%Farhan Khan MarwatAinda não há avaliações

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5795)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- House of TataDocumento36 páginasHouse of TataHarsh Bhardwaj0% (1)

- Internship Report at PT - Lennor - FinalDocumento34 páginasInternship Report at PT - Lennor - FinalUmmu Aya SofiaAinda não há avaliações

- BCT 6.x - Business ConneCT Brochure - EnglishDocumento16 páginasBCT 6.x - Business ConneCT Brochure - Englishdavid51brAinda não há avaliações

- SCC/AQPC Webinar: SCOR Benchmarking & SCC Member Benefits: Webinar Joseph Francis - CTO Supply Chain CouncilDocumento23 páginasSCC/AQPC Webinar: SCOR Benchmarking & SCC Member Benefits: Webinar Joseph Francis - CTO Supply Chain CouncilDenny SheatsAinda não há avaliações

- Fas 142 PDFDocumento2 páginasFas 142 PDFRickAinda não há avaliações

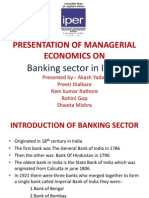

- Presentation of Managerial Economics On: Banking Sector in IndiaDocumento16 páginasPresentation of Managerial Economics On: Banking Sector in IndiaArchana PawarAinda não há avaliações

- Exam 1 OnlineDocumento2 páginasExam 1 OnlineGreg N Michelle SuddethAinda não há avaliações

- Quiz#1 MaDocumento5 páginasQuiz#1 Marayjoshua12Ainda não há avaliações

- Ebenezer Sathe: ProfileDocumento2 páginasEbenezer Sathe: ProfileRaj ShAinda não há avaliações

- 15.910 Draft SyllabusDocumento10 páginas15.910 Draft SyllabusSaharAinda não há avaliações

- CH 16Documento102 páginasCH 161asdfghjkl3Ainda não há avaliações

- WORKING CAPITAL MANAGEMENT of Axis Bank Finance Research 2014Documento112 páginasWORKING CAPITAL MANAGEMENT of Axis Bank Finance Research 2014Indu Gupta82% (11)

- 1q13 BP MM Global Sales PlaybookDocumento22 páginas1q13 BP MM Global Sales Playbookouss860Ainda não há avaliações

- Islamic Economic SystemDocumento5 páginasIslamic Economic Systemhelperforeu100% (1)

- Beekley v. Jessop Precision - ComplaintDocumento104 páginasBeekley v. Jessop Precision - ComplaintSarah BursteinAinda não há avaliações

- Case Study 7Documento2 páginasCase Study 7QinSiangAngAinda não há avaliações

- Llanera Police Station: Daily JournalDocumento5 páginasLlanera Police Station: Daily JournalLlanera Pnp NeAinda não há avaliações

- Paypal Resolution PackageDocumento46 páginasPaypal Resolution PackageTavon LewisAinda não há avaliações

- Sun Zi Art of WarDocumento12 páginasSun Zi Art of WarYeeWei TanAinda não há avaliações

- Multiple Choice Question 61Documento8 páginasMultiple Choice Question 61sweatangeAinda não há avaliações

- Report On WoodlandDocumento8 páginasReport On WoodlandAllwynThomasAinda não há avaliações

- 10 - Pdfsam - AEDITED AC3059 2013&2014 All Topics Exam Solutions Part IDocumento10 páginas10 - Pdfsam - AEDITED AC3059 2013&2014 All Topics Exam Solutions Part IEmily TanAinda não há avaliações

- Demand Forecasting in The Fashion Industry: A ReviewDocumento6 páginasDemand Forecasting in The Fashion Industry: A ReviewSamarth TuliAinda não há avaliações

- Strategic Acceleration SummaryDocumento6 páginasStrategic Acceleration SummarycoacherslandAinda não há avaliações

- Chapter 19Documento51 páginasChapter 19Yasir MehmoodAinda não há avaliações

- Ranchi Women's CollegeDocumento5 páginasRanchi Women's Collegevarsha kumariAinda não há avaliações

- Finman4e Quiz Mod18 040615Documento3 páginasFinman4e Quiz Mod18 040615Brian KangAinda não há avaliações

- 01-Sithind001b - Updated To Sit07v2.3Documento13 páginas01-Sithind001b - Updated To Sit07v2.3Samuel Fetor YaoAinda não há avaliações

- Practice Questions Chapter 4Documento26 páginasPractice Questions Chapter 4subash1111@gmail.com100% (1)

- Final Gola Ganda Marketing PlanDocumento40 páginasFinal Gola Ganda Marketing PlansamiraZehra100% (3)