Você também pode gostar

- Sem - III CA II AtktDocumento4 páginasSem - III CA II Atktabp1677Ainda não há avaliações

- Cost Accounting 3Documento3 páginasCost Accounting 3sharu SKAinda não há avaliações

- SampleproblemsDocumento5 páginasSampleproblemsCristine Joy BenitezAinda não há avaliações

- CMC-MT-PRMX-2-Q P !Documento7 páginasCMC-MT-PRMX-2-Q P !ritesh choudhuryAinda não há avaliações

- (CC-109 Cost Accounting - 2) - 2019Documento4 páginas(CC-109 Cost Accounting - 2) - 2019138 -Rajput-AdityaAinda não há avaliações

- Activity 4 Job Order CostingDocumento4 páginasActivity 4 Job Order CostingJOSCEL SYJONGTIANAinda não há avaliações

- Paper - 3: Cost Accounting and Financial Management Part I: Cost Accounting Questions MaterialDocumento38 páginasPaper - 3: Cost Accounting and Financial Management Part I: Cost Accounting Questions MaterialMinni BegumAinda não há avaliações

- Module 2 - Cost Classification and Cost BehaviorDocumento7 páginasModule 2 - Cost Classification and Cost BehaviorAlliah ArrozaAinda não há avaliações

- Bcom 5 Sem Cost Accounting 1 22100106 Jan 2022Documento4 páginasBcom 5 Sem Cost Accounting 1 22100106 Jan 2022Internet 223Ainda não há avaliações

- Paper - 3: Cost Accounting and Financial Management Part I: Cost Accounting Questions MaterialDocumento39 páginasPaper - 3: Cost Accounting and Financial Management Part I: Cost Accounting Questions MaterialAniket100% (1)

- Commerce Bba Semester 2 2022 November Basics of Cost Accounting 2019 PatternDocumento4 páginasCommerce Bba Semester 2 2022 November Basics of Cost Accounting 2019 PatternDhaval BakliwalAinda não há avaliações

- Concepts 5661fabb558e8Documento2 páginasConcepts 5661fabb558e8Allen CarlAinda não há avaliações

- 05 Financial Accounting Auditing Paper IV Cost Accounting Introduction and Basic ConceptsIDOL REV 201600037223Documento13 páginas05 Financial Accounting Auditing Paper IV Cost Accounting Introduction and Basic ConceptsIDOL REV 201600037223Mohit ParekhAinda não há avaliações

- Cost Accounting and ControlDocumento8 páginasCost Accounting and ControlJevbszen RemiendoAinda não há avaliações

- M.B.A (2019 Pattern)Documento157 páginasM.B.A (2019 Pattern)girishpawarudgirkarAinda não há avaliações

- Suggested Answer of November 2019 ExamDocumento21 páginasSuggested Answer of November 2019 ExamRakshitha VarshaAinda não há avaliações

- EXERCISECHAPTER2Documento8 páginasEXERCISECHAPTER2Bạch ThanhAinda não há avaliações

- Question Bank Paper: Cost Accounting McqsDocumento8 páginasQuestion Bank Paper: Cost Accounting McqsNikhilAinda não há avaliações

- Question Bank Paper: Cost Accounting McqsDocumento8 páginasQuestion Bank Paper: Cost Accounting McqsDarmin Kaye PalayAinda não há avaliações

- MASPDocumento3 páginasMASPSteeeeeeeephAinda não há avaliações

- ACT301 (Final), Spring-21Documento4 páginasACT301 (Final), Spring-21Papon SarkerAinda não há avaliações

- BACOSTMX Module 3 Self-ReviewerDocumento5 páginasBACOSTMX Module 3 Self-ReviewerlcAinda não há avaliações

- CMA QN November 2017Documento7 páginasCMA QN November 2017Goremushandu MungarevaniAinda não há avaliações

- Name: Score: Section: Assignment #2: Cost Concepts Identify If The Statement Is "TRUE or FALSE"Documento8 páginasName: Score: Section: Assignment #2: Cost Concepts Identify If The Statement Is "TRUE or FALSE"Karl AdreAinda não há avaliações

- Problems and Exercises in Introduction in Acctg and CVPDocumento4 páginasProblems and Exercises in Introduction in Acctg and CVPJanelleAinda não há avaliações

- Cost Grand Test 2Documento4 páginasCost Grand Test 2moniAinda não há avaliações

- Quiz 1 Intro and Cost BehaviorsDocumento3 páginasQuiz 1 Intro and Cost BehaviorsaaromeroAinda não há avaliações

- D) Ending Work in Process Is Less Than The Amount of The Beginning Work in Process InventoryDocumento9 páginasD) Ending Work in Process Is Less Than The Amount of The Beginning Work in Process InventoryPhương Thảo HoàngAinda não há avaliações

- Individual Assignment (Fall 2023) 2Documento11 páginasIndividual Assignment (Fall 2023) 2RealGenius (Carl)Ainda não há avaliações

- Manufacturing Account (With Answers) : Advanced LevelDocumento15 páginasManufacturing Account (With Answers) : Advanced LevelMomoh Kebiru0% (1)

- M.B.A (2019 Revised Pattern)Documento55 páginasM.B.A (2019 Revised Pattern)oscreators1923Ainda não há avaliações

- 09 Quiz 1Documento2 páginas09 Quiz 1ChiLL MooDAinda não há avaliações

- Answer Key To Test #1 - ACCT-312 - Fall 2019Documento8 páginasAnswer Key To Test #1 - ACCT-312 - Fall 2019Amir ContrerasAinda não há avaliações

- MGT Acc 2019 SolutionDocumento9 páginasMGT Acc 2019 SolutionSayeed AhmadAinda não há avaliações

- MGT Acc 2019 SolutionDocumento9 páginasMGT Acc 2019 SolutionSayeed AhmadAinda não há avaliações

- Final Exam Spring 2021 Orxan - 3Documento13 páginasFinal Exam Spring 2021 Orxan - 3Aydin NajafovAinda não há avaliações

- Discussion Question 2Documento6 páginasDiscussion Question 2Sadhna MaharjanAinda não há avaliações

- Mock Numerical Questions: Model Test PaperDocumento12 páginasMock Numerical Questions: Model Test PaperNaman JainAinda não há avaliações

- Accountancy Department: Preliminary Examination in MANACO 1Documento3 páginasAccountancy Department: Preliminary Examination in MANACO 1Gracelle Mae Oraller0% (1)

- Introduction To Management AccountingDocumento10 páginasIntroduction To Management AccountingPatrick Panlilio RetuyaAinda não há avaliações

- Absorbtion Costing MCQDocumento21 páginasAbsorbtion Costing MCQMuhammad Shabbar BukhariAinda não há avaliações

- Team PRTC May 2023 1st PBDocumento46 páginasTeam PRTC May 2023 1st PBEpfie SanchesAinda não há avaliações

- Orca Share Media1646571581803 6906221771846243726Documento12 páginasOrca Share Media1646571581803 6906221771846243726LACONSAY, Nathalie B.Ainda não há avaliações

- AFAR Set BDocumento11 páginasAFAR Set BRence Gonzales0% (2)

- Answer The Following Questions and Provide The Necessary RequirementsDocumento12 páginasAnswer The Following Questions and Provide The Necessary RequirementsKervin Rey JacksonAinda não há avaliações

- Week 1 Activity Cost Classification and BehaviorDocumento4 páginasWeek 1 Activity Cost Classification and BehaviorJosh YuuAinda não há avaliações

- 102.COAP - .L I Question CMA Special Examination 2021novemberDocumento4 páginas102.COAP - .L I Question CMA Special Examination 2021novemberleyaketjnuAinda não há avaliações

- Form Two Cost AccountingDocumento6 páginasForm Two Cost AccountingBernard DarkwahAinda não há avaliações

- Mba (2019 Pattern) - 230212 - 181328Documento171 páginasMba (2019 Pattern) - 230212 - 181328ManavAinda não há avaliações

- Wa0025Documento5 páginasWa0025Anggari SaputraAinda não há avaliações

- Manufacturing A LevelDocumento21 páginasManufacturing A LevelSheraz AhmadAinda não há avaliações

- Individual Assignment (Fall 2023) 2.docx2Documento10 páginasIndividual Assignment (Fall 2023) 2.docx2RealGenius (Carl)Ainda não há avaliações

- (New Account Titles and Financial Statements) : Module 8: Introduction To Manufacturing OperationDocumento4 páginas(New Account Titles and Financial Statements) : Module 8: Introduction To Manufacturing OperationAshitero YoAinda não há avaliações

- Test Series: March, 2022 Mock Test Paper - 1 Intermediate: Group - I Paper - 3: Cost and Management AccountingDocumento7 páginasTest Series: March, 2022 Mock Test Paper - 1 Intermediate: Group - I Paper - 3: Cost and Management AccountingMusic WorldAinda não há avaliações

- Managerial Accounting ProjectDocumento5 páginasManagerial Accounting ProjectAyaz AbroAinda não há avaliações

- T R S A: HE Eview Chool of CcountancyDocumento12 páginasT R S A: HE Eview Chool of CcountancyNamnam KimAinda não há avaliações

- BusinessManagement MidtermDocumento6 páginasBusinessManagement MidtermHoàng Thị Phương TrinhAinda não há avaliações

- Cma Final 2018 19Documento3 páginasCma Final 2018 19BrijmohanAinda não há avaliações

- Schaum's Outline of Principles of Accounting I, Fifth EditionNo EverandSchaum's Outline of Principles of Accounting I, Fifth EditionNota: 5 de 5 estrelas5/5 (3)

- Maharashtra State Board of Secondary and Higher Secondary Education, PuneDocumento20 páginasMaharashtra State Board of Secondary and Higher Secondary Education, PunePranjali GhodkeAinda não há avaliações

- SYBCOM ACCOUNTS SEM IV Syllabus PDFDocumento8 páginasSYBCOM ACCOUNTS SEM IV Syllabus PDFshrikantAinda não há avaliações

- Class Slide1 - Infosys Wealth Maximization PDFDocumento1 páginaClass Slide1 - Infosys Wealth Maximization PDFshrikantAinda não há avaliações

- OPAm 8 GNYATz 4 W P9 MMH IPDocumento12 páginasOPAm 8 GNYATz 4 W P9 MMH IPshrikantAinda não há avaliações

- Intoduction To Financial AccountsDocumento6 páginasIntoduction To Financial AccountsshrikantAinda não há avaliações

- Intro To Cost AccountingDocumento3 páginasIntro To Cost AccountingshrikantAinda não há avaliações

- Commercial Studies (Sem-2) 2022 Set - 2Documento7 páginasCommercial Studies (Sem-2) 2022 Set - 2shrikantAinda não há avaliações

- Company and IPR PPT of Adv - Dr. Sandip Yadav PDFDocumento87 páginasCompany and IPR PPT of Adv - Dr. Sandip Yadav PDFshrikantAinda não há avaliações

- Mathematics Coursebook Solution Grade7 Week: 3 & 4 Topic: Decimals Session: 1Documento14 páginasMathematics Coursebook Solution Grade7 Week: 3 & 4 Topic: Decimals Session: 1shrikantAinda não há avaliações

- Fybbi (Sem 1) : 1 Financial AccountingDocumento4 páginasFybbi (Sem 1) : 1 Financial AccountingshrikantAinda não há avaliações

- 68 Practical Questions of House PropertyDocumento14 páginas68 Practical Questions of House PropertyshrikantAinda não há avaliações

- Fresher CV 1Documento2 páginasFresher CV 1shrikantAinda não há avaliações

- ABT - BK Question Bank22-23Documento8 páginasABT - BK Question Bank22-23shrikantAinda não há avaliações

- V1 a17ZdcWGgjTMhDocumento3 páginasV1 a17ZdcWGgjTMhshrikantAinda não há avaliações

- Revision SheetsDocumento4 páginasRevision SheetsshrikantAinda não há avaliações

- Fybbi (Sem 1) : 1 Financial AccountingDocumento4 páginasFybbi (Sem 1) : 1 Financial AccountingshrikantAinda não há avaliações

- TYBCom Sem VI Financial Accounting MCQs PDFDocumento16 páginasTYBCom Sem VI Financial Accounting MCQs PDFshrikantAinda não há avaliações

- Maths I SSC Board Paper and Practice Papers PDFDocumento155 páginasMaths I SSC Board Paper and Practice Papers PDFshrikantAinda não há avaliações

- Meaning of Investment: MonetaryDocumento4 páginasMeaning of Investment: MonetaryshrikantAinda não há avaliações

- POGADocumento1 páginaPOGAshrikantAinda não há avaliações

- Your Company Name: StatementDocumento1 páginaYour Company Name: StatementshrikantAinda não há avaliações

- Fybbi (Sem 1) : 1 Financial AccountingDocumento2 páginasFybbi (Sem 1) : 1 Financial AccountingshrikantAinda não há avaliações

- Sanskrit Alhad PDFDocumento132 páginasSanskrit Alhad PDFshrikantAinda não há avaliações

- Smart Academy PDFDocumento14 páginasSmart Academy PDFshrikantAinda não há avaliações

- Shrikant New ResumeDocumento2 páginasShrikant New ResumeshrikantAinda não há avaliações

- Shrikant New ResumeDocumento2 páginasShrikant New ResumeshrikantAinda não há avaliações

- Work PlanDocumento1 páginaWork PlanshrikantAinda não há avaliações

- Semester III and IV PDFDocumento122 páginasSemester III and IV PDFAtmaram PawarAinda não há avaliações

- Tax CalenderDocumento1 páginaTax CalendershrikantAinda não há avaliações

- Project Report On Paper Bags ManufacturingDocumento8 páginasProject Report On Paper Bags ManufacturingEIRI Board of Consultants and Publishers100% (2)

- Assignment V - Short Run Decision MakingDocumento3 páginasAssignment V - Short Run Decision Makinganurag raoAinda não há avaliações

- Test Bank Transfer PricingDocumento11 páginasTest Bank Transfer PricingFerl Elardo100% (2)

- Disposition of VariancesDocumento12 páginasDisposition of VariancesNors PataytayAinda não há avaliações

- Jeans Manufacturing Industry-759387 PDFDocumento73 páginasJeans Manufacturing Industry-759387 PDFAmaan KhanAinda não há avaliações

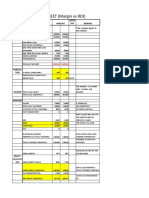

- Expenses Sheet (Margin Vs Roi) : MBA Chai Wala Set Up CostDocumento2 páginasExpenses Sheet (Margin Vs Roi) : MBA Chai Wala Set Up Cost1021210665 158220Ainda não há avaliações

- DPWH - Preparation of Approved Budget For The ContractDocumento6 páginasDPWH - Preparation of Approved Budget For The ContractELMERAinda não há avaliações

- Chapter 6 - Job Order CostingDocumento63 páginasChapter 6 - Job Order CostingXyne FernandezAinda não há avaliações

- Budgeting For Planning and ControlDocumento43 páginasBudgeting For Planning and ControlRica Yzabelle DoloresAinda não há avaliações

- Full Download Test Bank For Managerial Accounting For Managers 4th Edition PDF Full ChapterDocumento14 páginasFull Download Test Bank For Managerial Accounting For Managers 4th Edition PDF Full Chapterlutation.liddedrztjn100% (22)

- Introduction To Quantity SurveyingDocumento41 páginasIntroduction To Quantity SurveyingJohn MofireAinda não há avaliações

- AKMDocumento2 páginasAKMAsti EristiasaAinda não há avaliações

- Costing ExerciseDocumento4 páginasCosting ExerciseKien WahAinda não há avaliações

- Profit CenterDocumento3 páginasProfit CenterMAHENDRA SHIVAJI DHENAKAinda não há avaliações

- Vodafone Target CostingDocumento10 páginasVodafone Target CostingGopalAinda não há avaliações

- Full Download Developing Management Skills 10th Edition Whetten Test BankDocumento36 páginasFull Download Developing Management Skills 10th Edition Whetten Test Bankgdopaboyg100% (25)

- AccountingDocumento11 páginasAccountingβασιλης παυλος αρακαςAinda não há avaliações

- Nama: Andra Sulthan Thayyib Mantjanegara NIM: 041811233200 Tugas Akuntansi BiayaDocumento3 páginasNama: Andra Sulthan Thayyib Mantjanegara NIM: 041811233200 Tugas Akuntansi BiayaAda DapiAinda não há avaliações

- Test Bank Chapter 8 ABC For Decision Making PDFDocumento44 páginasTest Bank Chapter 8 ABC For Decision Making PDFMarvin AquinoAinda não há avaliações

- SMChap 015Documento40 páginasSMChap 015zoomblue200100% (2)

- 340 - Resource - 10 (F) Learning CurveDocumento19 páginas340 - Resource - 10 (F) Learning Curvebaby0310100% (2)

- Final Report Sarang Ujawane NicmarDocumento79 páginasFinal Report Sarang Ujawane NicmarMayank GhaiwatkarAinda não há avaliações

- Job OrderDocumento7 páginasJob OrderShannon Mojica100% (2)

- Cost Accounting Vol-IDocumento48 páginasCost Accounting Vol-ImanoAinda não há avaliações

- Cost and Management Accounting MCQDocumento14 páginasCost and Management Accounting MCQsasikumarthanus100% (2)

- AF 3112 Management Accounting 2: AgendaDocumento12 páginasAF 3112 Management Accounting 2: AgendaRoseAinda não há avaliações

- Questionnaires BSA SubjectsDocumento27 páginasQuestionnaires BSA SubjectsJamila Mae FabiaAinda não há avaliações

- ACC 311 - Week2 - 2-1 MyAccountingLab Homework - Chapter 4Documento18 páginasACC 311 - Week2 - 2-1 MyAccountingLab Homework - Chapter 4Lilian LAinda não há avaliações

- What Is Cost of Goods SoldDocumento19 páginasWhat Is Cost of Goods SoldRanaAinda não há avaliações

- Variable Costing V Absorption CostingDocumento16 páginasVariable Costing V Absorption CostingJane DizonAinda não há avaliações