Você também pode gostar

- Simplified Invoice: Invoice Number Date of Transaction Date of IssueDocumento1 páginaSimplified Invoice: Invoice Number Date of Transaction Date of IssueradhoinezerellyAinda não há avaliações

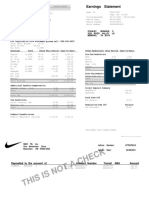

- Earnings Statement: Stanley, Monique S 3232 River Valley LN Memphis, TN 38119Documento1 páginaEarnings Statement: Stanley, Monique S 3232 River Valley LN Memphis, TN 38119Miquel JonesAinda não há avaliações

- Corporate TAX and Fin PlanningDocumento5 páginasCorporate TAX and Fin PlanningtraderescortAinda não há avaliações

- Introduction - EvidenceDocumento14 páginasIntroduction - EvidenceshanikaAinda não há avaliações

- Public FinanceDocumento38 páginasPublic FinanceRyan C. Villas100% (3)

- TDSDocumento18 páginasTDSPratik NaikAinda não há avaliações

- TdsDocumento22 páginasTdsFRANCIS JOSEPHAinda não há avaliações

- CS Professional Programme Tax NotesDocumento47 páginasCS Professional Programme Tax NotesRajey Jain100% (2)

- Direct Tax Vs Indirect TaxDocumento44 páginasDirect Tax Vs Indirect TaxShuchi BhatiaAinda não há avaliações

- E-Book On GST by CA. (DR.) G. S. Grewal - 2020Documento58 páginasE-Book On GST by CA. (DR.) G. S. Grewal - 2020Aarav DhingraAinda não há avaliações

- Topic: Page NoDocumento21 páginasTopic: Page NoAcchu BajajAinda não há avaliações

- 05 Corporate Tax Planning and ManagementDocumento34 páginas05 Corporate Tax Planning and ManagementHimanshu SharmaAinda não há avaliações

- Advance TaxDocumento11 páginasAdvance TaxAdv Aastha MakkarAinda não há avaliações

- Corporate Tax Planning Unit 1Documento26 páginasCorporate Tax Planning Unit 1Abinash PrustyAinda não há avaliações

- E-Filing of Income Tax Return: SUBMITTED BY: Nisha Ghodake Roll No: 17019. (Functional Project)Documento7 páginasE-Filing of Income Tax Return: SUBMITTED BY: Nisha Ghodake Roll No: 17019. (Functional Project)NISHA GHODAKEAinda não há avaliações

- CA Final GST and Customs Flow Charts Nov 2018Documento173 páginasCA Final GST and Customs Flow Charts Nov 2018Amar ShahAinda não há avaliações

- MSME Act 2006Documento13 páginasMSME Act 2006Ajay ChavanAinda não há avaliações

- Annual Report - PMJAY Small Version - 1Documento68 páginasAnnual Report - PMJAY Small Version - 1Saqib Faheem Kachroo100% (1)

- Tax Planning and Managerial DecisionDocumento188 páginasTax Planning and Managerial Decisionkomal_nath2375% (4)

- Only This Much For Company Secretary (CS) Executive Programme Book Updates & Amendments To Company, Economic, Labour, Securities Law 2010Documento31 páginasOnly This Much For Company Secretary (CS) Executive Programme Book Updates & Amendments To Company, Economic, Labour, Securities Law 2010Only This Much100% (5)

- CTP BooksDocumento3 páginasCTP BooksuzernaamAinda não há avaliações

- BCom Income Tax Procedure and PracticeDocumento61 páginasBCom Income Tax Procedure and PracticeUjjwal KandhaweAinda não há avaliações

- Income From SalariesDocumento19 páginasIncome From SalariesVineeta WadhwaniAinda não há avaliações

- Unit III Personal Tax Planning Bcom HonsDocumento38 páginasUnit III Personal Tax Planning Bcom Honshimanshi25gAinda não há avaliações

- Guide To CGST, SGST and IGST: Inter-State Vs Intra-StateDocumento6 páginasGuide To CGST, SGST and IGST: Inter-State Vs Intra-StateSuman IndiaAinda não há avaliações

- Non Trading OrganizationDocumento2 páginasNon Trading OrganizationPBGYB60% (5)

- CS Executive Tax Laws Suggested Answers-1Documento21 páginasCS Executive Tax Laws Suggested Answers-1nehaAinda não há avaliações

- AX Educted at Ource - I: KPPM & AssociatesDocumento67 páginasAX Educted at Ource - I: KPPM & AssociatesSaksham JoshiAinda não há avaliações

- Accounting For Bonus and Right of Issue.Documento38 páginasAccounting For Bonus and Right of Issue.Jacob SphinixAinda não há avaliações

- Dr. Shakuntala Misra National Rehabilitation University: Lucknow Faculty of LawDocumento9 páginasDr. Shakuntala Misra National Rehabilitation University: Lucknow Faculty of LawVimal SinghAinda não há avaliações

- Principles and Practice of AuditingDocumento55 páginasPrinciples and Practice of Auditingdanucandy2Ainda não há avaliações

- A Research Paper On Impact of Goods and Service Tax (GST) On Indian Gross Domestic Product (GDP)Documento8 páginasA Research Paper On Impact of Goods and Service Tax (GST) On Indian Gross Domestic Product (GDP)archerselevatorsAinda não há avaliações

- Income Tax Part 1Documento128 páginasIncome Tax Part 1Amandeep Kaur SethiAinda não há avaliações

- Income Tax Complete - E-Notes - Udesh Regular - Group 1Documento250 páginasIncome Tax Complete - E-Notes - Udesh Regular - Group 1Uday Tomar100% (1)

- GST BookDocumento100 páginasGST BookNaman ChopraAinda não há avaliações

- Basics of TaxationDocumento25 páginasBasics of TaxationAnupam BaliAinda não há avaliações

- Corporate Tax Planning and ManagemantDocumento11 páginasCorporate Tax Planning and ManagemantVijay KumarAinda não há avaliações

- IPCC - FAST TRACK MATERIAL - 35e PDFDocumento69 páginasIPCC - FAST TRACK MATERIAL - 35e PDFKunalKumarAinda não há avaliações

- GSTDocumento51 páginasGSTINDERDEEPAinda não há avaliações

- Presentation For Viva: Siddhesh Dhotre HPGD/JL20/1852Documento16 páginasPresentation For Viva: Siddhesh Dhotre HPGD/JL20/1852SIDDHESHAinda não há avaliações

- LEVY AND COLLECTION OF GST - AbhiDocumento14 páginasLEVY AND COLLECTION OF GST - AbhiAbhishek Abhi100% (1)

- TCS - in Income TaxDocumento8 páginasTCS - in Income TaxrpsinghsikarwarAinda não há avaliações

- Income Tax AY 18-19 Vol I PDFDocumento224 páginasIncome Tax AY 18-19 Vol I PDFAashish Kumar SinghAinda não há avaliações

- Income From Other SourcesDocumento29 páginasIncome From Other SourcesSatish BhadaniAinda não há avaliações

- Advance Payment of TaxDocumento4 páginasAdvance Payment of Taxparag03Ainda não há avaliações

- Income From SalaryDocumento103 páginasIncome From SalaryNAVEEN ROYAinda não há avaliações

- CH 5 Place of SupplyDocumento63 páginasCH 5 Place of SupplyManas Kumar SahooAinda não há avaliações

- Inter-Firm ComparisonDocumento5 páginasInter-Firm Comparisonanon_672065362100% (1)

- Module I - Income Tax and GSTDocumento4 páginasModule I - Income Tax and GSTMuhammed Yaseen MAinda não há avaliações

- GST Registration PPT Ver6 28042017Documento46 páginasGST Registration PPT Ver6 28042017Sonal AggarwalAinda não há avaliações

- GST Input Tax Credit NotesDocumento13 páginasGST Input Tax Credit Notesa_bc691973Ainda não há avaliações

- Indirect Tax and GSTDocumento124 páginasIndirect Tax and GSTPrasanna KumarAinda não há avaliações

- GST Assignments For B.com 6TH Sem PDFDocumento4 páginasGST Assignments For B.com 6TH Sem PDFAnujyadav Monuyadav100% (1)

- INCOME TAX AND GST. JURAZ-Module 2Documento5 páginasINCOME TAX AND GST. JURAZ-Module 2TERZO IncAinda não há avaliações

- Corporate TaxDocumento17 páginasCorporate TaxVishnupriya RameshAinda não há avaliações

- 18 GSTDocumento1.042 páginas18 GSTSwetaAinda não há avaliações

- Income Tax Summary by Sachin GuptaDocumento98 páginasIncome Tax Summary by Sachin GuptajesurajajosephAinda não há avaliações

- A STUDY OF PERCEPTION OF TAXPAYERS TOWARDS NewDocumento41 páginasA STUDY OF PERCEPTION OF TAXPAYERS TOWARDS NewsiddhantAinda não há avaliações

- Income-Tax Authorities: Dr. P. Sree Sudha, LL.D Associate Professor Damodaram Sanjivayya National Law UniversityDocumento113 páginasIncome-Tax Authorities: Dr. P. Sree Sudha, LL.D Associate Professor Damodaram Sanjivayya National Law UniversityTripathi OjAinda não há avaliações

- Old Vs New Tax Regime Comparative AnalysisDocumento11 páginasOld Vs New Tax Regime Comparative AnalysisAkchu KadAinda não há avaliações

- GST Tally ERP9 English: A Handbook for Understanding GST Implementation in TallyNo EverandGST Tally ERP9 English: A Handbook for Understanding GST Implementation in TallyNota: 5 de 5 estrelas5/5 (1)

- Investigation into the Adherence to Corporate Governance in Zimbabwe’s SME SectorNo EverandInvestigation into the Adherence to Corporate Governance in Zimbabwe’s SME SectorAinda não há avaliações

- Tds Due DatesDocumento1 páginaTds Due DatesKrishna Chaitanya DammalapatiAinda não há avaliações

- ManipurDocumento2 páginasManipurshanikaAinda não há avaliações

- SHANIKA IT LAW InterimDocumento8 páginasSHANIKA IT LAW InterimshanikaAinda não há avaliações

- Consequentialism 1Documento14 páginasConsequentialism 1shanikaAinda não há avaliações

- Law of Evidence - InterimDocumento6 páginasLaw of Evidence - InterimshanikaAinda não há avaliações

- Submitted By:: Merger and AcquisitionsDocumento7 páginasSubmitted By:: Merger and AcquisitionsshanikaAinda não há avaliações

- Scope of Work: SynopsisDocumento3 páginasScope of Work: SynopsisshanikaAinda não há avaliações

- Leader As Coach: Harold Chee Judge Business School Executive Education University of Cambridge H.chee@jbs - Cam.ac - UkDocumento25 páginasLeader As Coach: Harold Chee Judge Business School Executive Education University of Cambridge H.chee@jbs - Cam.ac - UkshanikaAinda não há avaliações

- Damodaram Sanjivayya National Law University Visakhapatnam, A.P., IndiaDocumento19 páginasDamodaram Sanjivayya National Law University Visakhapatnam, A.P., Indiashanika100% (1)

- SPICe HelpDocumento36 páginasSPICe HelpshanikaAinda não há avaliações

- Fostering A Culture of Innovation: The Role of Leadership: Jaideep Prabhu October 2018Documento90 páginasFostering A Culture of Innovation: The Role of Leadership: Jaideep Prabhu October 2018shanikaAinda não há avaliações

- Syllabus For Re - TestDocumento2 páginasSyllabus For Re - TestshanikaAinda não há avaliações

- Franking Account WorkpaperDocumento6 páginasFranking Account WorkpaperCarol YaoAinda não há avaliações

- Beer, Bourbon, & BBQDocumento3 páginasBeer, Bourbon, & BBQSunlight FoundationAinda não há avaliações

- Hwhwwjwjwjwjwjwiwiwiwkke Cpa Review School of The Philippines Manila Corporations Dela Cruz / de Vera / Lopez / LlamadoDocumento9 páginasHwhwwjwjwjwjwjwiwiwiwkke Cpa Review School of The Philippines Manila Corporations Dela Cruz / de Vera / Lopez / LlamadoSophia PerezAinda não há avaliações

- Paulsen JPL Effects Land Development Municipal Finance As PublishedDocumento21 páginasPaulsen JPL Effects Land Development Municipal Finance As PublishedMinnie.NAinda não há avaliações

- GR: Donations Inter Vivos Are Subject To Donor's Taxes While DonationsDocumento8 páginasGR: Donations Inter Vivos Are Subject To Donor's Taxes While DonationsDominic EmbodoAinda não há avaliações

- Adobe Transaction No 0991059129 20190125Documento2 páginasAdobe Transaction No 0991059129 20190125Mohamed WinnēriAinda não há avaliações

- Quiz 9 FABM 2 Income Taxation WO Answers 1Documento1 páginaQuiz 9 FABM 2 Income Taxation WO Answers 1Gelai BatadAinda não há avaliações

- 39 - 2007 Income Tax VAT Treatment Security Agencies WithholdingDocumento28 páginas39 - 2007 Income Tax VAT Treatment Security Agencies WithholdingChristy SanguyuAinda não há avaliações

- Onett Developer TemplateDocumento6 páginasOnett Developer Templatejoeye louieAinda não há avaliações

- InvoiceDocumento1 páginaInvoicemainakpati03Ainda não há avaliações

- Teamhgs 165148 Nov 2017 Payslip 165148Documento1 páginaTeamhgs 165148 Nov 2017 Payslip 165148Mohammad IrfanAinda não há avaliações

- Income Tax ReturnDocumento14 páginasIncome Tax ReturnEugene culpepperAinda não há avaliações

- Sheria Pay CHK 04-12-2019 2 PDFDocumento1 páginaSheria Pay CHK 04-12-2019 2 PDFLynn JonesAinda não há avaliações

- CIR v. Spouses Magaan, G.R. No. 232663, May 3, 2021Documento2 páginasCIR v. Spouses Magaan, G.R. No. 232663, May 3, 2021John Cyrus DangananAinda não há avaliações

- Tax Invoice: Zomato Limited Address: Pan NoDocumento1 páginaTax Invoice: Zomato Limited Address: Pan NoAshwaniAinda não há avaliações

- TAX 06.2 - Fringe Benefit TaxDocumento2 páginasTAX 06.2 - Fringe Benefit TaxMary Louise CamposanoAinda não há avaliações

- DIGEST - Reagan v. Commissioner, 30 SCRA 968 (1969)Documento1 páginaDIGEST - Reagan v. Commissioner, 30 SCRA 968 (1969)Reylland RendalAinda não há avaliações

- Did You Know That You Can Claim Tax Relief On Your RCN Subscription?Documento2 páginasDid You Know That You Can Claim Tax Relief On Your RCN Subscription?Shibu KalayilAinda não há avaliações

- Government of Andhra Pradesh Police Department:: Appco: M E N UDocumento1 páginaGovernment of Andhra Pradesh Police Department:: Appco: M E N U5532024 SAI KRISHNA.CHAinda não há avaliações

- Solved Xyz Exchanged Old Equipment For New Like Kind Equipment Xyz S AdjustedDocumento1 páginaSolved Xyz Exchanged Old Equipment For New Like Kind Equipment Xyz S AdjustedAnbu jaromiaAinda não há avaliações

- Tax 1 Case A-DDocumento96 páginasTax 1 Case A-DAn DinagaAinda não há avaliações

- Export of Services: BY PL - SubramanianDocumento31 páginasExport of Services: BY PL - SubramanianArun KennethAinda não há avaliações

- RR 08 00Documento5 páginasRR 08 00James Peter GarcesAinda não há avaliações

- BIR Ruling No. 522-2017Documento7 páginasBIR Ruling No. 522-2017liz kawiAinda não há avaliações

- Netmeds Bill 2024Documento1 páginaNetmeds Bill 2024sureshAinda não há avaliações

- DIGEST - Sitel Philippines Corp. v. CIRDocumento3 páginasDIGEST - Sitel Philippines Corp. v. CIRAgatha ApolinarioAinda não há avaliações

- IAS 8 Tutorial Question (SS)Documento2 páginasIAS 8 Tutorial Question (SS)Given RefilweAinda não há avaliações