Você também pode gostar

- Depreciation Methods: Solutions To ProblemsDocumento28 páginasDepreciation Methods: Solutions To ProblemsCeciliaRamirezAinda não há avaliações

- SM 9Documento12 páginasSM 9wtfAinda não há avaliações

- Fundamentals of Corporate Finance Canadian 6th Edition Brealey Solutions Manual 1Documento36 páginasFundamentals of Corporate Finance Canadian 6th Edition Brealey Solutions Manual 1jillhernandezqortfpmndz100% (23)

- Fundamentals of Corporate Finance Canadian 6th Edition Brealey Solutions ManualDocumento26 páginasFundamentals of Corporate Finance Canadian 6th Edition Brealey Solutions Manualmisentrynotal6ip1lp100% (16)

- Chapter 11 Mini Case: Cash Flow EstimationDocumento60 páginasChapter 11 Mini Case: Cash Flow EstimationafiAinda não há avaliações

- Brealey 5CE Ch09 SolutionsDocumento27 páginasBrealey 5CE Ch09 SolutionsToby Tobes TobezAinda não há avaliações

- CH 12 SM AssigDocumento6 páginasCH 12 SM AssigJefferson SarmientoAinda não há avaliações

- 3 - Capital Budgeting ImplementationDocumento9 páginas3 - Capital Budgeting ImplementationoryzanoviaAinda não há avaliações

- Topic 10Documento15 páginasTopic 10SUREINTHARAAN A/L NATHAN / UPMAinda não há avaliações

- Quiz 3Documento14 páginasQuiz 3K L YEOAinda não há avaliações

- FM FinalDocumento7 páginasFM FinalStoryKingAinda não há avaliações

- Financial and Managerial Accounting 14Th Edition Warren Solutions Manual Full Chapter PDFDocumento54 páginasFinancial and Managerial Accounting 14Th Edition Warren Solutions Manual Full Chapter PDFclitusarielbeehax100% (11)

- Cap Buget ProblemsDocumento8 páginasCap Buget ProblemsramakrishnanAinda não há avaliações

- PaybackDocumento14 páginasPaybackHema LathaAinda não há avaliações

- Stock Shares Price ($) Market Value of AssetsDocumento34 páginasStock Shares Price ($) Market Value of AssetsRADHIKA BANSALAinda não há avaliações

- Solution: Year Cash Inflows Present Value Factor Present Value $ @10% $Documento10 páginasSolution: Year Cash Inflows Present Value Factor Present Value $ @10% $Waylee CheroAinda não há avaliações

- ACTG1054 Answers To Practice Exercises From Course Outline and Learning Activities On MoodleDocumento8 páginasACTG1054 Answers To Practice Exercises From Course Outline and Learning Activities On MoodleCoc AndreiAinda não há avaliações

- Chapter 11Documento10 páginasChapter 11Syed Sheraz AliAinda não há avaliações

- ACCA F3-FFA Revision Mock - Answers D15Documento12 páginasACCA F3-FFA Revision Mock - Answers D15Kiri chrisAinda não há avaliações

- Brigham Chap 11 Practice Questions Solution For Chap 11Documento11 páginasBrigham Chap 11 Practice Questions Solution For Chap 11robin.asterAinda não há avaliações

- FCF Ch10 Excel Master StudentDocumento32 páginasFCF Ch10 Excel Master StudentTosa EndrawanAinda não há avaliações

- Capital Budgeting SolutionsDocumento3 páginasCapital Budgeting SolutionsJenny BernardinoAinda não há avaliações

- Chapter 05Documento26 páginasChapter 05slee11829% (7)

- EE - Assignment Chapter 9-10 SolutionDocumento11 páginasEE - Assignment Chapter 9-10 SolutionXuân ThànhAinda não há avaliações

- Running Head: Cost Allocation ConceptsDocumento6 páginasRunning Head: Cost Allocation ConceptsjaijohnkAinda não há avaliações

- Akuntansi Keuangan Menengah 1: Kelompok 5 1. Maya Putri Wijaya (142200210) 2. Muhammad Alfarizi (142200278) Kelas EA-IDocumento14 páginasAkuntansi Keuangan Menengah 1: Kelompok 5 1. Maya Putri Wijaya (142200210) 2. Muhammad Alfarizi (142200278) Kelas EA-Imuhammad alfariziAinda não há avaliações

- 9 - Chapter-7-Discounted-Cashflow-Techniques-with-AnswerDocumento15 páginas9 - Chapter-7-Discounted-Cashflow-Techniques-with-AnswerMd SaifulAinda não há avaliações

- F7 SolutionsDocumento15 páginasF7 Solutionsnoor ul anumAinda não há avaliações

- Fa 2 1Documento8 páginasFa 2 1Quỳnh Anh NguyễnAinda não há avaliações

- Accounting ExamDocumento6 páginasAccounting Examgenn katherine gadunAinda não há avaliações

- Cash Flow Brigham SolutionDocumento14 páginasCash Flow Brigham SolutionShahid Mehmood100% (4)

- PDF Document 8Documento42 páginasPDF Document 8nancymijaresalgosoAinda não há avaliações

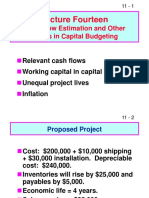

- Lecture Fourteen: Cash Flow Estimation and Other Topics in Capital BudgetingDocumento38 páginasLecture Fourteen: Cash Flow Estimation and Other Topics in Capital BudgetingHồng KhánhAinda não há avaliações

- CH 11 - CF Estimation Mini Case Sols Excel 14edDocumento36 páginasCH 11 - CF Estimation Mini Case Sols Excel 14edأثير مخوAinda não há avaliações

- Chapter 12Documento14 páginasChapter 12Naimmul FahimAinda não há avaliações

- Fundamentals of Corporate Finance 7Th Edition Brealey Solutions Manual Full Chapter PDFDocumento38 páginasFundamentals of Corporate Finance 7Th Edition Brealey Solutions Manual Full Chapter PDFcolonizeverseaat100% (10)

- P 7-15 Common Stock Value: All Growth ModelsDocumento8 páginasP 7-15 Common Stock Value: All Growth ModelsAlvira FajriAinda não há avaliações

- T 4Documento3 páginasT 4Muntasir AhmmedAinda não há avaliações

- Chapter 13 Capital Budgeting Estimating Cash Flow and Analyzing Risk Answers To End of Chapter Questions 13 3 Since The Cost of Capital Includes A Premium For Expected Inflation Failure 1Documento8 páginasChapter 13 Capital Budgeting Estimating Cash Flow and Analyzing Risk Answers To End of Chapter Questions 13 3 Since The Cost of Capital Includes A Premium For Expected Inflation Failure 1ghzAinda não há avaliações

- Wiley Chapter 9 HWDocumento4 páginasWiley Chapter 9 HWAri LeibowitzAinda não há avaliações

- Advacc 1 Answer Key Set ADocumento3 páginasAdvacc 1 Answer Key Set AA BAinda não há avaliações

- T5 - Qs and SolutionDocumento15 páginasT5 - Qs and SolutionCalvin MaAinda não há avaliações

- Solutions To Chapter 9 Using Discounted Cash-Flow Analysis To Make Investment DecisionsDocumento16 páginasSolutions To Chapter 9 Using Discounted Cash-Flow Analysis To Make Investment Decisionsmuhammad ihtishamAinda não há avaliações

- DepreciationDocumento4 páginasDepreciationMùhammad TàhaAinda não há avaliações

- Bacani HW FinalsDocumento10 páginasBacani HW FinalsKyle BacaniAinda não há avaliações

- Practice Solution 3Documento4 páginasPractice Solution 3Luigi NocitaAinda não há avaliações

- PDF PDFDocumento7 páginasPDF PDFMikey MadRatAinda não há avaliações

- Corpuz, Aily-Bsbafm2-2-Final Practice ProblemDocumento7 páginasCorpuz, Aily-Bsbafm2-2-Final Practice ProblemAily CorpuzAinda não há avaliações

- Answer Chapter11 Cash Flow EstimationDocumento3 páginasAnswer Chapter11 Cash Flow EstimationIsmah ParkAinda não há avaliações

- FM II Assignment 2 Solution W22Documento5 páginasFM II Assignment 2 Solution W22Farah ImamiAinda não há avaliações

- Intermediate Accounting 17Th Edition Kieso Solutions Manual Full Chapter PDFDocumento43 páginasIntermediate Accounting 17Th Edition Kieso Solutions Manual Full Chapter PDFDebraWhitecxgn100% (11)

- Intermediate Accounting 17th Edition Kieso Solutions ManualDocumento22 páginasIntermediate Accounting 17th Edition Kieso Solutions Manualdilysiristtes5100% (31)

- Assignment SolutionDocumento5 páginasAssignment SolutionAzmeena FezleenAinda não há avaliações

- Ch20 Guan CM Aise TBDocumento35 páginasCh20 Guan CM Aise TBHero CourseAinda não há avaliações

- Chapter 16 Problem SolutionsDocumento6 páginasChapter 16 Problem SolutionsAnila AAinda não há avaliações

- 10 Non-Current AssetsDocumento25 páginas10 Non-Current AssetsDayaan AAinda não há avaliações

- F2 - Mock A - Answers-2-11 143Documento10 páginasF2 - Mock A - Answers-2-11 143MD KaifAinda não há avaliações

- Managerial Project (Akanksha Shahi) FINALDocumento5 páginasManagerial Project (Akanksha Shahi) FINALakankshashahi1986Ainda não há avaliações

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsAinda não há avaliações

- Toward a National Eco-compensation Regulation in the People's Republic of ChinaNo EverandToward a National Eco-compensation Regulation in the People's Republic of ChinaAinda não há avaliações

- 05 - Ratio and ProportionDocumento17 páginas05 - Ratio and ProportionRupesh RoshanAinda não há avaliações

- Exempt From TaxDocumento32 páginasExempt From TaxErik KaufmanAinda não há avaliações

- RMC No 24-18 - Annexes B1-B5 - Required AttachmentsDocumento3 páginasRMC No 24-18 - Annexes B1-B5 - Required AttachmentsGil PinoAinda não há avaliações

- TRAIN Law BriefingDocumento30 páginasTRAIN Law BriefingJoselito PabatangAinda não há avaliações

- Taxation CasesDocumento296 páginasTaxation CasesshelAinda não há avaliações

- Jim Barfield Ethics ComplaintDocumento19 páginasJim Barfield Ethics ComplaintMatthew Daniel NyeAinda não há avaliações

- 1 DDocumento34 páginas1 DVholts Villa VitugAinda não há avaliações

- Overview of The Liechtenstein Foundation / Stiftung"Documento3 páginasOverview of The Liechtenstein Foundation / Stiftung"pieoiqtporetqeAinda não há avaliações

- Up Taxation Law Reviewer 2017 PDFDocumento267 páginasUp Taxation Law Reviewer 2017 PDFManny Aragones100% (3)

- MGFP BrochureDocumento26 páginasMGFP BrochureAbhinesh KumarAinda não há avaliações

- Audit Reconsideration Memorandum Baker SCRIBDDocumento7 páginasAudit Reconsideration Memorandum Baker SCRIBDMichael AlaoAinda não há avaliações

- Fact Sheet - Home Renovation Loan: MaybankDocumento2 páginasFact Sheet - Home Renovation Loan: MaybankLissa ChooAinda não há avaliações

- Zero Rated TransactionsDocumento4 páginasZero Rated Transactionssad nuAinda não há avaliações

- InvoiceDocumento1 páginaInvoiceVipin Kumar ChandelAinda não há avaliações

- Purchases + Carriage Inwards + Other Expenses Incurred On Purchase of Materials - Closing Inventory of MaterialsDocumento4 páginasPurchases + Carriage Inwards + Other Expenses Incurred On Purchase of Materials - Closing Inventory of MaterialsSiva SankariAinda não há avaliações

- LLP Notes As Per DU SyllabusDocumento39 páginasLLP Notes As Per DU SyllabusAryan GuptaAinda não há avaliações

- Provincial Employees Social Security Ordinance 1965 Doc pdf1 PDFDocumento34 páginasProvincial Employees Social Security Ordinance 1965 Doc pdf1 PDFRana Umair IsmailAinda não há avaliações

- Finanacial Ratios of HPCLDocumento10 páginasFinanacial Ratios of HPCLriyaAinda não há avaliações

- Project On HDFC LoansDocumento61 páginasProject On HDFC LoansPallavi80% (15)

- 2008-09 Citizens Budget Advisory Committee For The Betterment of PlainfieldDocumento35 páginas2008-09 Citizens Budget Advisory Committee For The Betterment of Plainfielddandamon100% (1)

- Navilyst BR 100 R12 Payables1.0Documento59 páginasNavilyst BR 100 R12 Payables1.0Bijay PaulAinda não há avaliações

- EBS - Configuration of Search String, Part 1Documento24 páginasEBS - Configuration of Search String, Part 1Bhaskar Reddy100% (1)

- GST - Unit 2 (Illustration Sums)Documento10 páginasGST - Unit 2 (Illustration Sums)subash minecraft creatorAinda não há avaliações

- Group Accounts - Subsidiaries (CSPLOCI) : Chapter Learning ObjectivesDocumento28 páginasGroup Accounts - Subsidiaries (CSPLOCI) : Chapter Learning ObjectivesKeotshepile Esrom MputleAinda não há avaliações

- Accounting Voucher 1Documento1 páginaAccounting Voucher 1Daksh BavawalaAinda não há avaliações

- Management Accountant - December 2011 PDFDocumento121 páginasManagement Accountant - December 2011 PDFSubir ChakrabartyAinda não há avaliações

- Taxation - Paper 11Documento8 páginasTaxation - Paper 11Innocent Won Aber100% (1)

- Marriot Hotel Islamabad FinalDocumento5 páginasMarriot Hotel Islamabad Finalsumaya0% (1)

- CH 13 SMDocumento31 páginasCH 13 SMNafisah MambuayAinda não há avaliações

- Stella Maris College: (Autonomous), Chennai, IndiaDocumento16 páginasStella Maris College: (Autonomous), Chennai, IndiaCasey JonesAinda não há avaliações