Você também pode gostar

- Capital Budgeting Decisions A Clear and Concise ReferenceNo EverandCapital Budgeting Decisions A Clear and Concise ReferenceAinda não há avaliações

- Chapter 7Documento53 páginasChapter 7Baby KhorAinda não há avaliações

- Chapter Five: The Financial Statements of Banks and Their Principal CompetitorsDocumento58 páginasChapter Five: The Financial Statements of Banks and Their Principal CompetitorsYoussef Youssef Ahmed Abdelmeguid Abdel LatifAinda não há avaliações

- Lecture 5: Interest Rate Risk (Part I) : DR Lixiong Guo Semester 2, 2015Documento31 páginasLecture 5: Interest Rate Risk (Part I) : DR Lixiong Guo Semester 2, 2015studentAinda não há avaliações

- Module IV - Working Capital ManagementDocumento50 páginasModule IV - Working Capital ManagementAshwin DholeAinda não há avaliações

- Finance Assignment InstructionDocumento7 páginasFinance Assignment InstructionJe-Ta CllAinda não há avaliações

- 3.sales Variance AnalysisDocumento38 páginas3.sales Variance Analysiskamasuke hegdeAinda não há avaliações

- CH 8Documento16 páginasCH 8emanmamdouh596Ainda não há avaliações

- Lecture 2: Exchange Rates and The Foreign Exchange Market: TopicsDocumento79 páginasLecture 2: Exchange Rates and The Foreign Exchange Market: TopicsSalvio MachaAinda não há avaliações

- Standard Costing and Variance Analysis: Fall 2007 CrossonDocumento20 páginasStandard Costing and Variance Analysis: Fall 2007 CrossonBernard SalongaAinda não há avaliações

- CH 13Documento28 páginasCH 13ReneeAinda não há avaliações

- International FInanceDocumento3 páginasInternational FInanceJemma JadeAinda não há avaliações

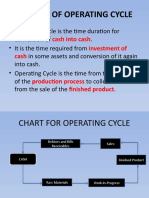

- Concept of Operating Cycle: Cash Into Cash Investment of CashDocumento6 páginasConcept of Operating Cycle: Cash Into Cash Investment of CashVenket RamanaAinda não há avaliações

- Cost ManagementDocumento18 páginasCost ManagementGeo Rublico ManilaAinda não há avaliações

- Overhead VariancesDocumento11 páginasOverhead VariancesDanica VillaganteAinda não há avaliações

- MCS Assignment - 3Documento13 páginasMCS Assignment - 3MIRAL PATELAinda não há avaliações

- Part Seven: THE Management of Financial InstitutionsDocumento40 páginasPart Seven: THE Management of Financial InstitutionsIrakli SaliaAinda não há avaliações

- Duration GAP AnalysisDocumento5 páginasDuration GAP AnalysisShubhash ShresthaAinda não há avaliações

- International Finance Lecture SlidesDocumento27 páginasInternational Finance Lecture Slidesmaryam ashfaqAinda não há avaliações

- PPT-4 Parity Conditions and Currency ForecastingDocumento42 páginasPPT-4 Parity Conditions and Currency ForecastingKamal KantAinda não há avaliações

- Transfer PricingDocumento57 páginasTransfer PricingbijoyendasAinda não há avaliações

- KOCH6Documento63 páginasKOCH6Swati SoniAinda não há avaliações

- 324 - International Parity ConditionsDocumento49 páginas324 - International Parity ConditionsTamuna BibiluriAinda não há avaliações

- Financial Derivatives: Prof. Scott JoslinDocumento49 páginasFinancial Derivatives: Prof. Scott Joslinarnav100% (2)

- Chapter10 Investment Function in BankDocumento38 páginasChapter10 Investment Function in BankTừ Lê Lan HươngAinda não há avaliações

- CHP 12 - Strategy, Balanced Scorecard, and Strategic Profitability (With Answers)Documento54 páginasCHP 12 - Strategy, Balanced Scorecard, and Strategic Profitability (With Answers)kenchong7150% (1)

- Basel 3Documento32 páginasBasel 3Venkat SaiAinda não há avaliações

- Chapter Twenty-Two: Managing Interest Rate Risk and Insolvency Risk On The Balance SheetDocumento23 páginasChapter Twenty-Two: Managing Interest Rate Risk and Insolvency Risk On The Balance SheetSagheer MuhammadAinda não há avaliações

- QuestionsDocumento10 páginasQuestionsYat Kunt ChanAinda não há avaliações

- Target Costing Presentation FinalDocumento57 páginasTarget Costing Presentation FinalMr Dampha100% (1)

- GAP Management Managing Interest Rate Risk at Banks and ThriftsDocumento18 páginasGAP Management Managing Interest Rate Risk at Banks and ThriftsrunawayyyAinda não há avaliações

- Asset Pricing ModelDocumento15 páginasAsset Pricing ModelEnp Gus AgostoAinda não há avaliações

- Hierarchy of VariancesDocumento1 páginaHierarchy of VariancesQaisar AbbasAinda não há avaliações

- Cash Coversion CYcleDocumento29 páginasCash Coversion CYcleZohaib HassanAinda não há avaliações

- Assignment 1 - Investment AnalysisDocumento5 páginasAssignment 1 - Investment Analysisphillimon zuluAinda não há avaliações

- JitDocumento26 páginasJitRachanakumari100% (1)

- MC DonaldDocumento15 páginasMC DonaldShreya Patel100% (1)

- B03 - Life CycleDocumento11 páginasB03 - Life CycleAcca BooksAinda não há avaliações

- Chapter 8 PDFDocumento43 páginasChapter 8 PDFCarlosAinda não há avaliações

- Product Life Cycle Costing / Whole Life Cycle Costing /life Cycle CostingDocumento23 páginasProduct Life Cycle Costing / Whole Life Cycle Costing /life Cycle CostingTapiwa Tbone MadamombeAinda não há avaliações

- M7 International Financial InstitutionsDocumento29 páginasM7 International Financial Institutionsnaughty dela cruzAinda não há avaliações

- Just-in-Time and Lean OperationsDocumento90 páginasJust-in-Time and Lean OperationsSaad PirzadaAinda não há avaliações

- FX Risk Management Transaction Exposure: Slide 1Documento55 páginasFX Risk Management Transaction Exposure: Slide 1prakashputtuAinda não há avaliações

- CA IPCC Costing & FM Quick Revision NotesDocumento21 páginasCA IPCC Costing & FM Quick Revision NotesChandreshAinda não há avaliações

- Balance ScorecardDocumento25 páginasBalance ScorecardJia BarrientosAinda não há avaliações

- Cost Behavior AnalysisDocumento5 páginasCost Behavior AnalysisMuhammad Umer Qureshi100% (1)

- 3353 TVM Lecture 3Documento31 páginas3353 TVM Lecture 3herueuxAinda não há avaliações

- Balance Scorecard and BenchmarkingDocumento12 páginasBalance Scorecard and BenchmarkingGaurav Sharma100% (1)

- Advanced Bond ConceptsDocumento8 páginasAdvanced Bond ConceptsEllaine OlimberioAinda não há avaliações

- By: Anjali KulshresthaDocumento18 páginasBy: Anjali KulshresthaAnjali KulshresthaAinda não há avaliações

- Bond Valuation: Bond Analysis: Returns & Systematic RiskDocumento50 páginasBond Valuation: Bond Analysis: Returns & Systematic RiskSamad KhanAinda não há avaliações

- Measuring Exposure To Exchange Rate FluctuationsDocumento21 páginasMeasuring Exposure To Exchange Rate FluctuationsMohitAinda não há avaliações

- Financial Statement Analysis (Fsa)Documento32 páginasFinancial Statement Analysis (Fsa)Shashank100% (1)

- Chapter 6 International Banking and Money Market 4017Documento23 páginasChapter 6 International Banking and Money Market 4017jdahiya_1Ainda não há avaliações

- Management Accounting-Nature and ScopeDocumento13 páginasManagement Accounting-Nature and ScopePraveen SinghAinda não há avaliações

- Portfolio Selection Using Sharpe, Treynor & Jensen Performance IndexDocumento15 páginasPortfolio Selection Using Sharpe, Treynor & Jensen Performance Indexktkalai selviAinda não há avaliações

- 1.4 Market Failure: Section 1: MicroeconomicsDocumento19 páginas1.4 Market Failure: Section 1: MicroeconomicsCalvin ManAinda não há avaliações

- Components of Financial SystemDocumento11 páginasComponents of Financial SystemromaAinda não há avaliações

- Credit ManagementDocumento24 páginasCredit ManagementrajnishdubeAinda não há avaliações

- Dwnload Full Auditing and Assurance Services 15th Edition Arens Solutions Manual PDFDocumento35 páginasDwnload Full Auditing and Assurance Services 15th Edition Arens Solutions Manual PDFconstanceholmesz7jjy100% (12)

- Ipo Procedure: An Analysis On The Book Building Method in BangladeshDocumento9 páginasIpo Procedure: An Analysis On The Book Building Method in BangladeshMuhaiminul IslamAinda não há avaliações

- CPA ReviewDocumento14 páginasCPA ReviewnikkaaaAinda não há avaliações

- NilDocumento555 páginasNilMariline LeeAinda não há avaliações

- International Financial Management PgapteDocumento25 páginasInternational Financial Management PgapterameshmbaAinda não há avaliações

- Lesson 19 Value Investing For Smart People Safal NiveshakDocumento3 páginasLesson 19 Value Investing For Smart People Safal NiveshakKohinoor RoyAinda não há avaliações

- Negotiable Instruments Law - Philippine Law ReviewersDocumento49 páginasNegotiable Instruments Law - Philippine Law ReviewersRenalyn DarioAinda não há avaliações

- Safal Niveshak Mastermind BrochureDocumento3 páginasSafal Niveshak Mastermind BrochureNaveen K. JindalAinda não há avaliações

- Blink Health - Chaiken - ComplaintDocumento36 páginasBlink Health - Chaiken - Complainti723087100% (1)

- Annexure 1 - Detailed InstructionsDocumento4 páginasAnnexure 1 - Detailed InstructionsIshan CAinda não há avaliações

- © 1999. Omega Research, Inc. Miami, FloridaDocumento160 páginas© 1999. Omega Research, Inc. Miami, Floridajamesfin68100% (1)

- Standard Chartered Weekly Market ViewDocumento11 páginasStandard Chartered Weekly Market ViewAceAinda não há avaliações

- Carlingford - March EP Update - Part 1 - Premier OilDocumento14 páginasCarlingford - March EP Update - Part 1 - Premier Oil55entiAinda não há avaliações

- Banking Awareness Capsule Sbi Po Bob PoDocumento48 páginasBanking Awareness Capsule Sbi Po Bob PoLokesh AgarwalAinda não há avaliações

- Bursa Malaysia Annual Report 2015Documento222 páginasBursa Malaysia Annual Report 2015Ahmad Hakimi TajuddinAinda não há avaliações

- Financial Instruments Illustration 1Documento10 páginasFinancial Instruments Illustration 1Deep KrishnaAinda não há avaliações

- The Lunchtime Trader Version 17 With Footer and CryptoDocumento144 páginasThe Lunchtime Trader Version 17 With Footer and CryptoEnrique Blanco100% (3)

- Demerger of BajajDocumento30 páginasDemerger of BajajNikhil100% (1)

- ICS Transmile Group Berhad PDFDocumento36 páginasICS Transmile Group Berhad PDFUmar othman0% (1)

- Microfinance in Developed CountriesDocumento11 páginasMicrofinance in Developed CountriesSomesh SrivastavaAinda não há avaliações

- Fong v. DueñasDocumento3 páginasFong v. DueñasGia DimayugaAinda não há avaliações

- Remedies of The TaxpayerDocumento16 páginasRemedies of The TaxpayerCristelle Elaine Collera100% (1)

- Mutual Fund Investment From An Individual's PerspectiveDocumento89 páginasMutual Fund Investment From An Individual's PerspectiveSAJIDA SHAIKHAinda não há avaliações

- TechnipFMC Signs A Major Contract With MIDOR For Their Refinery Expansion and Modernization in EgyptDocumento2 páginasTechnipFMC Signs A Major Contract With MIDOR For Their Refinery Expansion and Modernization in Egyptmuhammad ilyasAinda não há avaliações

- RMC No 37-2016Documento6 páginasRMC No 37-2016sandra100% (1)

- SHA Broker Update Form - October 2015Documento1 páginaSHA Broker Update Form - October 2015henrydeeAinda não há avaliações

- Ki Unvr 20240212Documento9 páginasKi Unvr 20240212muh.asad.amAinda não há avaliações

- Final Exam Corporate Finance CFVG 2016-2017Documento8 páginasFinal Exam Corporate Finance CFVG 2016-2017Hạt TiêuAinda não há avaliações

- MULPHA-AnnualReport2007 (3.2MB)Documento148 páginasMULPHA-AnnualReport2007 (3.2MB)selvamech84Ainda não há avaliações

- Avant Garde Case StudyDocumento7 páginasAvant Garde Case StudyTanmayAinda não há avaliações