Você também pode gostar

- Planning Decision Support ModelDocumento2.505 páginasPlanning Decision Support ModelwahajAinda não há avaliações

- Development Sales Lacking: Wheelock Properties (S)Documento7 páginasDevelopment Sales Lacking: Wheelock Properties (S)Theng RogerAinda não há avaliações

- HQ - Sr. DCM Meeting 14.11.14Documento16 páginasHQ - Sr. DCM Meeting 14.11.14ccm erAinda não há avaliações

- Horizontal Analysis Statement of Financial Position: Current AssetsDocumento8 páginasHorizontal Analysis Statement of Financial Position: Current AssetsCarlyn TarigaAinda não há avaliações

- Deptl HighlightsDocumento84 páginasDeptl HighlightsAshwin ShankarAinda não há avaliações

- Sett Info UIN Wise 16 FebDocumento8 páginasSett Info UIN Wise 16 FebHussain AliAinda não há avaliações

- Compan: Interest ProfitDocumento4 páginasCompan: Interest ProfitkhatiwodasushantAinda não há avaliações

- Daily FNO Overview: Retail ResearchDocumento5 páginasDaily FNO Overview: Retail ResearchjaimaaganAinda não há avaliações

- Realisasi 29 Januari 2024Documento1 páginaRealisasi 29 Januari 2024alvindwio10Ainda não há avaliações

- Dily Gainers and LosersDocumento10 páginasDily Gainers and LosersAnshuman GuptaAinda não há avaliações

- Pipeline Tematik Plafond Besar November Belum Di TL SD 14 Nov'23Documento53 páginasPipeline Tematik Plafond Besar November Belum Di TL SD 14 Nov'23del.camp9795Ainda não há avaliações

- 2018 Fund Utilization ConsolidatedDocumento1 página2018 Fund Utilization ConsolidatedNERI LLENAinda não há avaliações

- RBE-KHI 6-6-2023 AnalysisDocumento1 páginaRBE-KHI 6-6-2023 AnalysisKashif MalikAinda não há avaliações

- Pi Daily Strategy 24112023 SumDocumento7 páginasPi Daily Strategy 24112023 SumPateera Chananti PhoomwanitAinda não há avaliações

- Format LapselDocumento27 páginasFormat LapselTana BudiyanaAinda não há avaliações

- Summary BenchmarkDocumento28 páginasSummary BenchmarkADAinda não há avaliações

- Tanaman Biofarmaka (TBF) 2013-2016Documento32 páginasTanaman Biofarmaka (TBF) 2013-2016zumantaraAinda não há avaliações

- Laporan TDPDocumento57 páginasLaporan TDPRizky Sena Ramadhan 16Ainda não há avaliações

- Merck Gen Eurofarma Gen Sandoz Medley Ranbaxy Ache Gen Ems Gen Germed GSK RX SanofiDocumento13 páginasMerck Gen Eurofarma Gen Sandoz Medley Ranbaxy Ache Gen Ems Gen Germed GSK RX SanofiLuiz PereiraAinda não há avaliações

- Assets & Liabilities Committee Report: Performance Management & MonitoringDocumento15 páginasAssets & Liabilities Committee Report: Performance Management & MonitoringMichael OseleAinda não há avaliações

- Weekly Report - Xiv - April 4 To 8, 2011Documento2 páginasWeekly Report - Xiv - April 4 To 8, 2011JC CalaycayAinda não há avaliações

- Reporte-1t2023 MagotsabDocumento2 páginasReporte-1t2023 MagotsabLuis Walter Hernandez VallejosAinda não há avaliações

- Next 50Documento631 páginasNext 50Kasthuri CoimbatoreAinda não há avaliações

- 274 CKDocumento1 página274 CKsanitasisanggauAinda não há avaliações

- M Ceo Campaign As On 25.02.2024Documento1 páginaM Ceo Campaign As On 25.02.2024sivajaduAinda não há avaliações

- Building InsuranceDocumento6 páginasBuilding Insurancepgmc.pg42020Ainda não há avaliações

- Weekly Report - Xvii - April 25 To 29, 2011Documento2 páginasWeekly Report - Xvii - April 25 To 29, 2011JC CalaycayAinda não há avaliações

- Country: Iraq: Usd Million S.No. Hscode Commodity 2018-2019 2019-2020 (Apr - Jan (P) )Documento3 páginasCountry: Iraq: Usd Million S.No. Hscode Commodity 2018-2019 2019-2020 (Apr - Jan (P) )Drx Mehazabeen KachchawalaAinda não há avaliações

- Costos LogisticosDocumento7 páginasCostos LogisticosBrayan Calcina BellotAinda não há avaliações

- DOMO-Mill Cost Des'21Documento20 páginasDOMO-Mill Cost Des'21Andreas Eduard LerrickAinda não há avaliações

- Year 2013 2014 2015 2016 2017 Latest: CompetitionDocumento3 páginasYear 2013 2014 2015 2016 2017 Latest: CompetitionDahagam SaumithAinda não há avaliações

- FY2019-20 q3 RESULTDocumento4 páginasFY2019-20 q3 RESULTgauravkrastogiAinda não há avaliações

- CMD VC (03.04.24) - v.6Documento7 páginasCMD VC (03.04.24) - v.6sandeshymcaAinda não há avaliações

- Annual Report 2012Documento16 páginasAnnual Report 2012DonaldDeLeonAinda não há avaliações

- 2019 2020Documento6 páginas2019 2020ylliansanluisAinda não há avaliações

- Turnarounds Marco 2023Documento17 páginasTurnarounds Marco 2023Gustavo Turatto HenriqueAinda não há avaliações

- NHPC LTDDocumento9 páginasNHPC LTDMit chauhanAinda não há avaliações

- Description: Tags: 06q4ffelpgaDocumento4 páginasDescription: Tags: 06q4ffelpgaanon-313532Ainda não há avaliações

- Team Arthaniti - K J Somaiya Institute of ManagementDocumento22 páginasTeam Arthaniti - K J Somaiya Institute of Managementpratyay gangulyAinda não há avaliações

- OI SpurtsDocumento22 páginasOI SpurtsBallAinda não há avaliações

- Report As On 25.11.23Documento6 páginasReport As On 25.11.23sachingowdacvAinda não há avaliações

- Location SnapshotDocumento8 páginasLocation SnapshotJ MarshallAinda não há avaliações

- Detail AnalysisDocumento1 páginaDetail AnalysisPraveen ShresthaAinda não há avaliações

- Accord Capital Equities Corporation: Outlook For Week16 - April 18 To 20 - TD 076-078Documento4 páginasAccord Capital Equities Corporation: Outlook For Week16 - April 18 To 20 - TD 076-078JC CalaycayAinda não há avaliações

- Demon Slayer Vol1Documento1 páginaDemon Slayer Vol1veerag jamdarAinda não há avaliações

- Daily FNO Overview: Retail ResearchDocumento5 páginasDaily FNO Overview: Retail ResearchjaimaaganAinda não há avaliações

- Rce Consumption ReportDocumento18 páginasRce Consumption ReportMaribeth LibuitAinda não há avaliações

- Give and Care RS ScoreDocumento84 páginasGive and Care RS Scoretawatchai limAinda não há avaliações

- Description: Tags: 05ffelpgaDocumento3 páginasDescription: Tags: 05ffelpgaanon-439255Ainda não há avaliações

- Report Closing Area 29.09.2022Documento1 páginaReport Closing Area 29.09.2022MardiansahAinda não há avaliações

- Presentation On PG Process and Returns IssuesDocumento12 páginasPresentation On PG Process and Returns IssuesFederico Dipay Jr.Ainda não há avaliações

- Narration Mar-08 Mar-09 Mar-10 Mar-11 Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Trailing Best Case Worst CaseDocumento10 páginasNarration Mar-08 Mar-09 Mar-10 Mar-11 Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Trailing Best Case Worst CasemkrahumanAinda não há avaliações

- Cfin2 HW1Documento25 páginasCfin2 HW1Anirudh BharAinda não há avaliações

- Pharmaceutical Pakistan PPT 2019Documento20 páginasPharmaceutical Pakistan PPT 2019Syed Haider Ali50% (2)

- OAAP West BengalDocumento13 páginasOAAP West Bengalfunda metricsAinda não há avaliações

- TATA Steel and CorusDocumento28 páginasTATA Steel and CorusTushar ShahAinda não há avaliações

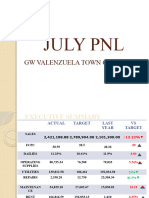

- July PNLDocumento7 páginasJuly PNLTeacher JoanAinda não há avaliações

- Daily FNO Overview: Retail ResearchDocumento5 páginasDaily FNO Overview: Retail ResearchjaimaaganAinda não há avaliações

- Croda Smarter Polymers Guide Sep 2019Documento20 páginasCroda Smarter Polymers Guide Sep 2019Keith Tamura100% (1)

- Practical Research 2Documento16 páginasPractical Research 2Benedict Coloma BandongAinda não há avaliações

- Two Occult Philosophers in The Elizabethan Age: by Peter ForshawDocumento10 páginasTwo Occult Philosophers in The Elizabethan Age: by Peter ForshawFrancesco VinciguerraAinda não há avaliações

- CHAPTER 2 (C) Innovation in EntrepreneurDocumento36 páginasCHAPTER 2 (C) Innovation in EntrepreneurHuiLingAinda não há avaliações

- Bhagavatam English Chapter 10bDocumento22 páginasBhagavatam English Chapter 10bsrimatsimhasaneshwarAinda não há avaliações

- To Word AkheebDocumento31 páginasTo Word AkheebDavid Raju GollapudiAinda não há avaliações

- Soal PTS Vii BigDocumento6 páginasSoal PTS Vii Bigdimas awe100% (1)

- PS410Documento2 páginasPS410Kelly AnggoroAinda não há avaliações

- 2012 Karshaniya YavaguDocumento4 páginas2012 Karshaniya YavaguRANJEET SAWANTAinda não há avaliações

- South San Francisco Talks Plans For Sports Park ImprovementsDocumento32 páginasSouth San Francisco Talks Plans For Sports Park ImprovementsSan Mateo Daily JournalAinda não há avaliações

- Membrane and TransportDocumento25 páginasMembrane and TransportHafsa JalisiAinda não há avaliações

- Action Research in Araling PanlipunanDocumento3 páginasAction Research in Araling PanlipunanLotisBlanca94% (17)

- Goal SettingDocumento11 páginasGoal Settingraul_mahadikAinda não há avaliações

- Zoology LAB Scheme of Work 2023 Hsslive HSSDocumento7 páginasZoology LAB Scheme of Work 2023 Hsslive HSSspookyvibee666Ainda não há avaliações

- Test Iii Cultural Social and Political OrganizationDocumento2 páginasTest Iii Cultural Social and Political OrganizationTin NatayAinda não há avaliações

- 5024Documento2 páginas5024Luis JesusAinda não há avaliações

- Best S and Nocella, III (Eds.) - Igniting A Revolution - Voices in Defense of The Earth PDFDocumento455 páginasBest S and Nocella, III (Eds.) - Igniting A Revolution - Voices in Defense of The Earth PDFRune Skjold LarsenAinda não há avaliações

- ArticleDocumento9 páginasArticleElly SufriadiAinda não há avaliações

- Learning Theories Behaviourism, Cognitivism, Social ConstructivismDocumento39 páginasLearning Theories Behaviourism, Cognitivism, Social ConstructivismJuan Miguel100% (3)

- Recruitment Process Outsourcing PDFDocumento4 páginasRecruitment Process Outsourcing PDFDevesh NamdeoAinda não há avaliações

- CIT 811 TMA 4 Quiz QuestionDocumento3 páginasCIT 811 TMA 4 Quiz QuestionjohnAinda não há avaliações

- Different Art TechniquesDocumento39 páginasDifferent Art TechniquesRommel LegaspiAinda não há avaliações

- TRUMPF Marking Laser BrochureDocumento48 páginasTRUMPF Marking Laser BrochureKKM SBAinda não há avaliações

- Case Study 17 TomDocumento7 páginasCase Study 17 Tomapi-519148723Ainda não há avaliações

- Structural Engineering Formulas Second EditionDocumento224 páginasStructural Engineering Formulas Second Editionahmed_60709595194% (33)

- California Academy For Lilminius (Cal) : Lesson PlanDocumento4 páginasCalifornia Academy For Lilminius (Cal) : Lesson Plandarryl franciscoAinda não há avaliações

- Automotive SensorsDocumento20 páginasAutomotive SensorsahmedAinda não há avaliações

- Revised LabDocumento18 páginasRevised LabAbu AyemanAinda não há avaliações

- Calculating Staff Strength:: Find Latest Hospitality Resources atDocumento8 páginasCalculating Staff Strength:: Find Latest Hospitality Resources atPriyanjali SainiAinda não há avaliações