Você também pode gostar

- Annual Income Tax Return: I I 0 1 1 I I 0 1 2 I I 0 1 1 I I 0 1 2 I I 0 1 3Documento9 páginasAnnual Income Tax Return: I I 0 1 1 I I 0 1 2 I I 0 1 1 I I 0 1 2 I I 0 1 3albertAinda não há avaliações

- BIR Form No. 1701Documento4 páginasBIR Form No. 1701blesypAinda não há avaliações

- New Income Tax Return BIR Form 1701 - November 2011 RevisedDocumento6 páginasNew Income Tax Return BIR Form 1701 - November 2011 RevisedBusinessTips.Ph100% (4)

- 1701 Bir Form 2006 2013-2019Documento11 páginas1701 Bir Form 2006 2013-2019Jessie Boy Balino BalderamaAinda não há avaliações

- 2550 MDocumento2 páginas2550 MJose Venturina Villacorta100% (3)

- Membership Savings Remittance Form (MSRF) : HQP-PFF-053Documento2 páginasMembership Savings Remittance Form (MSRF) : HQP-PFF-053Airine ParedesAinda não há avaliações

- New Income Tax Return BIR Form 1702 - November 2011 RevisedDocumento6 páginasNew Income Tax Return BIR Form 1702 - November 2011 RevisedBusinessTips.Ph100% (4)

- New Income Tax Return BIR Form 1700 - November 2011 RevisedDocumento4 páginasNew Income Tax Return BIR Form 1700 - November 2011 RevisedBusinessTips.Ph100% (2)

- SEC Requirements For Accreditation of CPAs in Public PracticeDocumento2 páginasSEC Requirements For Accreditation of CPAs in Public PracticemelissaAinda não há avaliações

- 0619-E Jan 2018 Rev Final - FFDocumento1 página0619-E Jan 2018 Rev Final - FFthis is my nameAinda não há avaliações

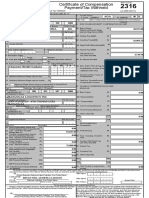

- 2316Documento13 páginas2316Ariel BarkerAinda não há avaliações

- 2020 - PFRS For SEs NotesDocumento16 páginas2020 - PFRS For SEs NotesRodelLabor100% (1)

- BIR Form 1906Documento1 páginaBIR Form 1906rafael soriaoAinda não há avaliações

- Bir Form 2306 and 2307 MchsDocumento3 páginasBir Form 2306 and 2307 Mchschristopher labastidaAinda não há avaliações

- BIR FORM 2307 SampleDocumento6 páginasBIR FORM 2307 SampleEasyHear Philippines by NuGen Hearing Devices, Inc.Ainda não há avaliações

- C BirDocumento1 páginaC Birchari cruzmanAinda não há avaliações

- Bir 2306Documento2 páginasBir 2306Caroline Sanchez90% (10)

- Gadiano 2316Documento2 páginasGadiano 2316Jypy Torrejos100% (1)

- Bir 2013Documento1 páginaBir 2013karlycoreAinda não há avaliações

- Request For Rulings - NAP 3.20.14Documento3 páginasRequest For Rulings - NAP 3.20.14ConnieAllanaMacapagaoAinda não há avaliações

- Sample 2307 2017Documento4 páginasSample 2307 2017jordzAinda não há avaliações

- Euv 1ST 2011 1701QDocumento6 páginasEuv 1ST 2011 1701QAdrian Raymnd EspirituAinda não há avaliações

- Bir 1701Documento4 páginasBir 1701Vanesa Calimag ClementeAinda não há avaliações

- Bir Ruling Da 192-08Documento2 páginasBir Ruling Da 192-08norliza albutraAinda não há avaliações

- 1601e Form PDFDocumento3 páginas1601e Form PDFLee GhaiaAinda não há avaliações

- BMBE SeminarDocumento60 páginasBMBE SeminarBabyGiant LucasAinda não há avaliações

- BIR Form No. 1709 Final PDFDocumento3 páginasBIR Form No. 1709 Final PDFErica Caliuag0% (1)

- Affidavit of No RentalDocumento1 páginaAffidavit of No RentalLala Duran100% (1)

- 267731702final PDFDocumento5 páginas267731702final PDFelmarcomonal100% (1)

- BIR Books of Accounts Registration SlipDocumento2 páginasBIR Books of Accounts Registration SlipAngieLlantoCuriosoAinda não há avaliações

- Sworn Application For Tax Clearance Annex C 1 RufDocumento1 páginaSworn Application For Tax Clearance Annex C 1 RufellenAinda não há avaliações

- BIR Form No. 0608 PDFDocumento2 páginasBIR Form No. 0608 PDFPaolo MartinAinda não há avaliações

- Makati City Business Registration FlowDocumento4 páginasMakati City Business Registration FlowAika Chescka DucaAinda não há avaliações

- Annex D Bir InventoryDocumento17 páginasAnnex D Bir InventoryMarie Fe EgarAinda não há avaliações

- Registration Update Sheet: Taxpayer InformationDocumento1 páginaRegistration Update Sheet: Taxpayer InformationRCVZ BKAinda não há avaliações

- Cda Red FR 003 Rev7 CaprDocumento32 páginasCda Red FR 003 Rev7 CaprRaina Phia PantaleonAinda não há avaliações

- Annex F RR 11-2018Documento1 páginaAnnex F RR 11-2018Gerynes Mae Bacarra100% (1)

- SEC Cover Sheet For AFSDocumento1 páginaSEC Cover Sheet For AFSredenbidedAinda não há avaliações

- TAX BRIEFING-NEW RegistrantsDocumento57 páginasTAX BRIEFING-NEW RegistrantsPcl Nueva Vizcaya100% (3)

- Cooperatives Financial StatementsDocumento76 páginasCooperatives Financial StatementsTaga AbraAinda não há avaliações

- Revenue Memorandum Order 26-2010Documento2 páginasRevenue Memorandum Order 26-2010Jayvee OlayresAinda não há avaliações

- Rmo 12 2013 List of Unused Expired Orssiscis Annex D Docxdocx PDF FreeDocumento2 páginasRmo 12 2013 List of Unused Expired Orssiscis Annex D Docxdocx PDF FreeShitake MitsukiAinda não há avaliações

- BIR Form 2316 UndertakingDocumento1 páginaBIR Form 2316 UndertakingJan Paolo CruzAinda não há avaliações

- Bookkeeping RegulationsDocumento23 páginasBookkeeping RegulationsJewellrie Dela Cruz100% (2)

- Bir Ruling (Da-031-07)Documento2 páginasBir Ruling (Da-031-07)Stacy Liong BloggerAccountAinda não há avaliações

- Republic of The Philippines) ) S.S.Documento4 páginasRepublic of The Philippines) ) S.S.Noan SimanAinda não há avaliações

- SEC Cover SheetDocumento1 páginaSEC Cover SheetAya PulidoAinda não há avaliações

- SEC FormsDocumento4 páginasSEC FormsZen Catolico ErumAinda não há avaliações

- Certification Statement of Management's Responsibility (Itr)Documento1 páginaCertification Statement of Management's Responsibility (Itr)Earl Jhune Amoranto100% (1)

- BIR PenaltiesDocumento12 páginasBIR PenaltiesMark VillaverdeAinda não há avaliações

- Old Form 0605 PDFDocumento2 páginasOld Form 0605 PDFeugene badere50% (2)

- 2316Documento1 página2316EmmanuelClementCastilloTalimoroAinda não há avaliações

- Affidavit of No RentalDocumento1 páginaAffidavit of No Rentalkevin cosnerAinda não há avaliações

- BIR Form 0605Documento3 páginasBIR Form 0605rafael soriao0% (1)

- Sana MabagoDocumento1 páginaSana MabagojoystambaAinda não há avaliações

- BIRForm1701 Old FormDocumento6 páginasBIRForm1701 Old FormKristine VelardeAinda não há avaliações

- 1701Q BIR Form PDFDocumento3 páginas1701Q BIR Form PDFJihani A. SalicAinda não há avaliações

- 1701qjuly2008 (ENCS) q22019Documento5 páginas1701qjuly2008 (ENCS) q22019Andrew AndalAinda não há avaliações

- Annual Income Tax Return: I I 0 1 1 I I 0 1 2 I I 0 1 1 I I 0 1 1 I I 0 1 2 I I 0 1 3Documento5 páginasAnnual Income Tax Return: I I 0 1 1 I I 0 1 2 I I 0 1 1 I I 0 1 1 I I 0 1 2 I I 0 1 3Jhanrich MatalaAinda não há avaliações

- 1701osd 2018 101224Documento7 páginas1701osd 2018 101224Janeth Tamayo NavalesAinda não há avaliações

- Travel Itinerary SpreadsheetDocumento31 páginasTravel Itinerary SpreadsheetNinaAinda não há avaliações

- Ace Sloution ReconsilationDocumento103 páginasAce Sloution ReconsilationgvramonAinda não há avaliações

- Designing A Container Terminal YardDocumento108 páginasDesigning A Container Terminal Yardlim kang hai100% (5)

- The Case Study of 3Pl: Fedex Supply Chain SolutionDocumento23 páginasThe Case Study of 3Pl: Fedex Supply Chain SolutionPhylix LaiAinda não há avaliações

- Review of The Accounting Process PDFDocumento3 páginasReview of The Accounting Process PDFShiela Marie Sta AnaAinda não há avaliações

- Double Entry SystemDocumento8 páginasDouble Entry SystemTayyaba TariqAinda não há avaliações

- Fee Challan FormDocumento1 páginaFee Challan FormMahmood Ahmad NooriAinda não há avaliações

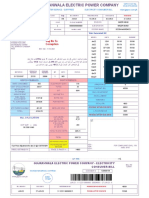

- Gepco Online Bill - Muhammad HussainDocumento1 páginaGepco Online Bill - Muhammad HussainUsman AmjadAinda não há avaliações

- Electronic Ticket Receipt, April 05 For MR JEMUEL LABRADORDocumento2 páginasElectronic Ticket Receipt, April 05 For MR JEMUEL LABRADORJemuel LabradorAinda não há avaliações

- Sovereign Container Line, Inc: 10644481 SCLI40008202Documento1 páginaSovereign Container Line, Inc: 10644481 SCLI40008202ORLANDO GONZALEZAinda não há avaliações

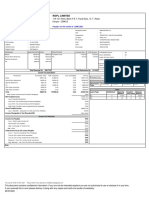

- RSPL Limited: Payslip For The Month of JUNE 2021Documento1 páginaRSPL Limited: Payslip For The Month of JUNE 2021Manju ManjappaAinda não há avaliações

- Complete Function Module Documentation From FKK - PAYMEDIUM Up To FMCA - DISPLAY - ConsolutDocumento23 páginasComplete Function Module Documentation From FKK - PAYMEDIUM Up To FMCA - DISPLAY - Consolutpal singhAinda não há avaliações

- Jan To Oct Statment PDFDocumento8 páginasJan To Oct Statment PDFP NAVEEN KUMARAinda não há avaliações

- Febrero 24Documento12 páginasFebrero 24micasacontractors893Ainda não há avaliações

- Advantages of Having Centralized Bus TerminalDocumento2 páginasAdvantages of Having Centralized Bus TerminalBlack Tirah TirahAinda não há avaliações

- Bill Malout PDFDocumento2 páginasBill Malout PDFCuber Anay GuptaAinda não há avaliações

- How Does A Letter of Credit WorkDocumento9 páginasHow Does A Letter of Credit WorkAnju KumariAinda não há avaliações

- New Balance $6,751.10 Payment Due Date 10/05/19: American Express Classic Gold CardDocumento8 páginasNew Balance $6,751.10 Payment Due Date 10/05/19: American Express Classic Gold CardIrshad aliAinda não há avaliações

- Overview of Regular Savings Key Policies and Fees: Bank of America Clarity StatementDocumento2 páginasOverview of Regular Savings Key Policies and Fees: Bank of America Clarity StatementJacob DaleAinda não há avaliações

- Report Detail Product Sold 2023-07-20Documento13 páginasReport Detail Product Sold 2023-07-20apotek-tanjungdurenrayaAinda não há avaliações

- Methods in International Payments: Bank Transfer Bank RemittanceDocumento12 páginasMethods in International Payments: Bank Transfer Bank RemittanceThach NcAinda não há avaliações

- Adjusted Adjusted Trial Balance Income Statement BalanceDocumento1 páginaAdjusted Adjusted Trial Balance Income Statement BalancedreaAinda não há avaliações

- Kakinada Municipal Corporation: ReceiptDocumento1 páginaKakinada Municipal Corporation: ReceiptYagna PrakashraoAinda não há avaliações

- Format of The Petty Cash BookDocumento49 páginasFormat of The Petty Cash BookNa Ni63% (8)

- transaction 25 Transaction/s /transaction 5 Transaction/s /transaction 1 Transaction/sDocumento1 páginatransaction 25 Transaction/s /transaction 5 Transaction/s /transaction 1 Transaction/sLease Management and Administration GroupSAMAinda não há avaliações

- Hyperloop - Explained - School AssignmentDocumento11 páginasHyperloop - Explained - School AssignmentMarket LitmusAinda não há avaliações

- Eticket Itinerary / Receipt: Booking DetailsDocumento4 páginasEticket Itinerary / Receipt: Booking DetailsSolikhinAinda não há avaliações

- Statement of Account: Transaction Date Description Debit Credit Available BalanceDocumento6 páginasStatement of Account: Transaction Date Description Debit Credit Available BalancezamanAinda não há avaliações

- DeclaredDocumento2 páginasDeclarednurun nahar chowdhuryAinda não há avaliações