Você também pode gostar

- Forces of Fantasy (1ed)Documento127 páginasForces of Fantasy (1ed)Strogg100% (7)

- Organic Cotton Market ReportDocumento7 páginasOrganic Cotton Market Reportmlganesh666100% (1)

- The World Agriculture Industry: A Study in Falling Supply and Rising DemandDocumento12 páginasThe World Agriculture Industry: A Study in Falling Supply and Rising DemandsuvromallickAinda não há avaliações

- Chapter 1 Capstone Case: New Century Wellness GroupDocumento4 páginasChapter 1 Capstone Case: New Century Wellness GroupJC100% (7)

- World Food Outlook: Geo FactsheetDocumento4 páginasWorld Food Outlook: Geo FactsheetParco300Ainda não há avaliações

- Project Technical TextilesDocumento22 páginasProject Technical Textilesvijayabaskar777Ainda não há avaliações

- Report On Techinical TextilesDocumento235 páginasReport On Techinical Textilesmlganesh666100% (1)

- Ceresana - Brochure Market Study UreaDocumento7 páginasCeresana - Brochure Market Study UreaSyukri ShahAinda não há avaliações

- Food Outlook: Biannual Report on Global Food Markets. November 2020No EverandFood Outlook: Biannual Report on Global Food Markets. November 2020Ainda não há avaliações

- School Form 10 SF10 Learners Permanent Academic Record For Elementary SchoolDocumento10 páginasSchool Form 10 SF10 Learners Permanent Academic Record For Elementary SchoolRene ManansalaAinda não há avaliações

- 2011 Usda Outlook 02252011Documento18 páginas2011 Usda Outlook 02252011Sazid RahmanAinda não há avaliações

- Usda 2011 LatestDocumento40 páginasUsda 2011 LatestsuperclonefanAinda não há avaliações

- Cotton OutlookDocumento16 páginasCotton Outlookskouroudis_443636363Ainda não há avaliações

- World Agricultural Supply and Demand Estimates: United States Department of AgricultureDocumento40 páginasWorld Agricultural Supply and Demand Estimates: United States Department of Agricultureankit19833760Ainda não há avaliações

- Wasde 09 2011 AnalysisDocumento40 páginasWasde 09 2011 AnalysisDiego GervasAinda não há avaliações

- World Agricultural Supply and Demand Estimates: United States Department of AgricultureDocumento40 páginasWorld Agricultural Supply and Demand Estimates: United States Department of AgricultureAnkit AgarwalAinda não há avaliações

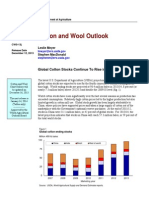

- Cotton and Wool Outlook: India Leads 2021/22 Global Cotton ProductionDocumento8 páginasCotton and Wool Outlook: India Leads 2021/22 Global Cotton ProductionBrittany EtheridgeAinda não há avaliações

- WHEAT: Projected U.S. Wheat Ending Stocks For 2011/12 Are Raised 90 Million Bushels This MonthDocumento67 páginasWHEAT: Projected U.S. Wheat Ending Stocks For 2011/12 Are Raised 90 Million Bushels This MonthDiego GervasAinda não há avaliações

- A Presentation On CottonDocumento24 páginasA Presentation On CottonUrooj AnsariAinda não há avaliações

- World Agricultural Supply and Demand Estimates: United States Department of AgricultureDocumento40 páginasWorld Agricultural Supply and Demand Estimates: United States Department of AgricultureDiego GervasAinda não há avaliações

- Cotton: Trends in Global Production, Trade and PolicyDocumento14 páginasCotton: Trends in Global Production, Trade and PolicyInternational Centre for Trade and Sustainable DevelopmentAinda não há avaliações

- World Agricultural Supply and Demand Estimates: United States Department of AgricultureDocumento40 páginasWorld Agricultural Supply and Demand Estimates: United States Department of AgricultureFranc LuisAinda não há avaliações

- World Agricultural Supply and Demand Estimates: United States Department of AgricultureDocumento40 páginasWorld Agricultural Supply and Demand Estimates: United States Department of Agricultureapi-78654247Ainda não há avaliações

- World Agricultural Production: Southeast Asia Rice: Production Forecast Lower Owing To Widespread FloodingDocumento27 páginasWorld Agricultural Production: Southeast Asia Rice: Production Forecast Lower Owing To Widespread Floodingapi-51572145Ainda não há avaliações

- World Agricultural Supply and Demand Estimates: United States Department of AgricultureDocumento40 páginasWorld Agricultural Supply and Demand Estimates: United States Department of Agricultureapi-51572145Ainda não há avaliações

- ICAC Report Projects Global Cotton Market Trends Through 2020Documento9 páginasICAC Report Projects Global Cotton Market Trends Through 2020Shukhrat TuychievAinda não há avaliações

- Production PDFDocumento37 páginasProduction PDFHankAinda não há avaliações

- Famine Is Now Looming: Volatile But Buoyant MarketDocumento1 páginaFamine Is Now Looming: Volatile But Buoyant MarketblwardAinda não há avaliações

- World Agricultural Supply and Demand Estimates Report SummaryDocumento40 páginasWorld Agricultural Supply and Demand Estimates Report SummaryB6D4N0Ainda não há avaliações

- Global Feed Markets: November - December 2011Documento6 páginasGlobal Feed Markets: November - December 2011Milling and Grain magazineAinda não há avaliações

- Commodities - MARKETS OUTLOOK 1506Documento6 páginasCommodities - MARKETS OUTLOOK 1506Milling and Grain magazineAinda não há avaliações

- Final Report 01Documento1 páginaFinal Report 01Hrishi GaykarAinda não há avaliações

- Commodities - MARKETS OUTLOOK 1504Documento6 páginasCommodities - MARKETS OUTLOOK 1504Milling and Grain magazineAinda não há avaliações

- USDA Coffee Report Outlines World Production and PricesDocumento26 páginasUSDA Coffee Report Outlines World Production and PricesSanjay NarayanAinda não há avaliações

- El Niño and Cereal Production Shortfalls: Policies For Resilience and Food Security in 2016 and BeyondDocumento6 páginasEl Niño and Cereal Production Shortfalls: Policies For Resilience and Food Security in 2016 and BeyondIFPRIAinda não há avaliações

- چاول خبریں ۴ جولائ ۲۰۲۰Documento40 páginasچاول خبریں ۴ جولائ ۲۰۲۰Mujahid AliAinda não há avaliações

- Wasde 0521Documento40 páginasWasde 0521Willfrieds Nong WaingAinda não há avaliações

- Cotton FibreDocumento30 páginasCotton Fibreankit161019893980Ainda não há avaliações

- FAO FodOutlookDocumento119 páginasFAO FodOutlookVinay Hr LaambaAinda não há avaliações

- Global Feed Markets: November - December 2013Documento8 páginasGlobal Feed Markets: November - December 2013Milling and Grain magazineAinda não há avaliações

- CWS 22fDocumento6 páginasCWS 22fRajnish ShuklaAinda não há avaliações

- Cotton UpdateDocumento6 páginasCotton UpdateAngel BrokingAinda não há avaliações

- MB Emerging Food Crisis ... A Problem or Consequence 4 18 2011Documento9 páginasMB Emerging Food Crisis ... A Problem or Consequence 4 18 2011Vin LavaAinda não há avaliações

- Rice YearbookDocumento92 páginasRice Yearbookm76507084Ainda não há avaliações

- RT Vol. 10, No. 4 Rice FactsDocumento2 páginasRT Vol. 10, No. 4 Rice FactsRice TodayAinda não há avaliações

- LatestDocumento40 páginasLatestPetrus Slamet Putra WijayaAinda não há avaliações

- World Agricultural Production: Canada Wheat: Crop Area Rebounds Despite Early Season ProblemsDocumento25 páginasWorld Agricultural Production: Canada Wheat: Crop Area Rebounds Despite Early Season Problemsapi-78654247Ainda não há avaliações

- Corn-Tortilla Value ChainDocumento41 páginasCorn-Tortilla Value Chainchame_sanpedroAinda não há avaliações

- Current Wolrd Fertilizers Trends and OutlookDocumento45 páginasCurrent Wolrd Fertilizers Trends and OutlookFlorinel DAinda não há avaliações

- India peanut production forecast lower due to insufficient southern rainfallDocumento25 páginasIndia peanut production forecast lower due to insufficient southern rainfallRahul PachoriAinda não há avaliações

- Commodities - MARKETS OUTLOOKDocumento8 páginasCommodities - MARKETS OUTLOOKMilling and Grain magazineAinda não há avaliações

- Jumlah Konsumsi Jagung GlobalDocumento21 páginasJumlah Konsumsi Jagung GlobalVincentius EdwardAinda não há avaliações

- Afghanistan Report 2010Documento2 páginasAfghanistan Report 2010AhadAinda não há avaliações

- Cotton Fibre Quality Research Needs in IndiaDocumento11 páginasCotton Fibre Quality Research Needs in IndiaprabhjotseehraAinda não há avaliações

- AICO SeedCo ReportDocumento16 páginasAICO SeedCo ReportBatanai MatsikaAinda não há avaliações

- Exploring PresentationDocumento30 páginasExploring Presentationrighth012Ainda não há avaliações

- Commodities - MARKETS OUTLOOKDocumento6 páginasCommodities - MARKETS OUTLOOKMilling and Grain magazineAinda não há avaliações

- RT Vol. 10, No. 3 Rice FactsDocumento2 páginasRT Vol. 10, No. 3 Rice FactsRice TodayAinda não há avaliações

- Cotton M StapleDocumento2 páginasCotton M StapleSandeep TopeAinda não há avaliações

- Pakistan Flood Demage Full Crop Report: 2010-11Documento25 páginasPakistan Flood Demage Full Crop Report: 2010-11cottontradeAinda não há avaliações

- World Agricultural Supply and Demand Estimates: United States Department of AgricultureDocumento40 páginasWorld Agricultural Supply and Demand Estimates: United States Department of Agricultureapi-78654247Ainda não há avaliações

- Cotton and Products India 2013Documento22 páginasCotton and Products India 2013Kannan KrishnamurthyAinda não há avaliações

- Market ReportDocumento3 páginasMarket Reportapi-311090769Ainda não há avaliações

- Role of Cotton in PakistanDocumento3 páginasRole of Cotton in PakistanUmair Mushtaq SyedAinda não há avaliações

- Food Outlook: Biannual Report on Global Food Markets: November 2019No EverandFood Outlook: Biannual Report on Global Food Markets: November 2019Ainda não há avaliações

- Food Outlook: Biannual Report on Global Food Markets: November 2021No EverandFood Outlook: Biannual Report on Global Food Markets: November 2021Ainda não há avaliações

- COTTON USA Global Fax Update - November 2010Documento2 páginasCOTTON USA Global Fax Update - November 2010mlganesh666Ainda não há avaliações

- U.S. Cotton Prices and The World Cotton MarketDocumento32 páginasU.S. Cotton Prices and The World Cotton Marketmlganesh666Ainda não há avaliações

- Cotton: World Markets and Trade: Franc-Zone Africa Exportable Supplies StabilizeDocumento26 páginasCotton: World Markets and Trade: Franc-Zone Africa Exportable Supplies Stabilizemlganesh666Ainda não há avaliações

- The Impacts of Increased Minimum Support Prices in India On World and U.S. Cotton MarketsDocumento8 páginasThe Impacts of Increased Minimum Support Prices in India On World and U.S. Cotton Marketsmlganesh666Ainda não há avaliações

- Cotton: World Markets and Trade: June 2010Documento26 páginasCotton: World Markets and Trade: June 2010mlganesh666Ainda não há avaliações

- Cotton World Market and Trade ReportDocumento26 páginasCotton World Market and Trade ReportcottontradeAinda não há avaliações

- Cotton: World Markets and TradeDocumento28 páginasCotton: World Markets and Trademlganesh666Ainda não há avaliações

- Cotton World Market and Trade ReportDocumento26 páginasCotton World Market and Trade ReportcottontradeAinda não há avaliações

- Franc-Zone Africa Exportable Supplies StabilizeDocumento26 páginasFranc-Zone Africa Exportable Supplies Stabilizemlganesh666Ainda não há avaliações

- Record World Cotton Prices and High VolatilityDocumento1 páginaRecord World Cotton Prices and High Volatilitymlganesh666Ainda não há avaliações

- 2010 Annual Economic OutlookDocumento74 páginas2010 Annual Economic OutlookKhehleng TsosaneAinda não há avaliações

- USTER AFIS PRO - Measurement Principle & Test ResultsDocumento51 páginasUSTER AFIS PRO - Measurement Principle & Test Resultsmlganesh66691% (35)

- Spinning NormsDocumento39 páginasSpinning Normsmlganesh666100% (1)

- USTER HVI Spectrum Measuring PrinciplesDocumento45 páginasUSTER HVI Spectrum Measuring PrinciplesRAMARAMRAM100% (2)

- PT Krakatau Steel's Energy Efficiency Best PracticesDocumento32 páginasPT Krakatau Steel's Energy Efficiency Best PracticesDavid Budi SaputraAinda não há avaliações

- Compact Cotton YarnDocumento5 páginasCompact Cotton Yarnmlganesh666Ainda não há avaliações

- A Comparative Study of The Characteristicsof Compact Yarn-Based Knitted FabricsDocumento5 páginasA Comparative Study of The Characteristicsof Compact Yarn-Based Knitted Fabricsmlganesh666Ainda não há avaliações

- Waste Minimasation GuideDocumento92 páginasWaste Minimasation Guidemlganesh666Ainda não há avaliações

- China Cotton Index Detail Meaning & TermsDocumento2 páginasChina Cotton Index Detail Meaning & Termsmlganesh666Ainda não há avaliações

- Textile EngineeringDocumento9 páginasTextile Engineeringmlganesh666Ainda não há avaliações

- 6269 19651 1 PBDocumento4 páginas6269 19651 1 PBmlganesh666Ainda não há avaliações

- Trade Price Case Cotton YarnDocumento30 páginasTrade Price Case Cotton Yarnmlganesh666Ainda não há avaliações

- Indian Textile and ApparelDocumento30 páginasIndian Textile and Apparelmlganesh666Ainda não há avaliações

- China Zce TermsDocumento1 páginaChina Zce Termsmlganesh666Ainda não há avaliações

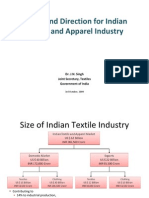

- Status and DirectionDocumento28 páginasStatus and Directionmlganesh666Ainda não há avaliações

- Indian Textile and Clothing Global ComparativeDocumento32 páginasIndian Textile and Clothing Global Comparativemlganesh666Ainda não há avaliações

- Intermediate Algebra For College Students 7th Edition Blitzer Test BankDocumento19 páginasIntermediate Algebra For College Students 7th Edition Blitzer Test Bankdireful.trunnionmnwf5100% (30)

- Acts and Statutory Instruments: The Volume of UK Legislation 1850 To 2019Documento24 páginasActs and Statutory Instruments: The Volume of UK Legislation 1850 To 2019Adam GreenAinda não há avaliações

- Pradeep Kumar SinghDocumento9 páginasPradeep Kumar SinghHarsh TiwariAinda não há avaliações

- Summary of Kamban's RamayanaDocumento4 páginasSummary of Kamban's RamayanaRaj VenugopalAinda não há avaliações

- The Meaning of Life Without Parole - Rough Draft 1Documento4 páginasThe Meaning of Life Without Parole - Rough Draft 1api-504422093Ainda não há avaliações

- RVU Distribution - New ChangesDocumento5 páginasRVU Distribution - New Changesmy indiaAinda não há avaliações

- Key Concepts in Marketing: Maureen Castillo Dyna Enad Carelle Trisha Espital Ethel SilvaDocumento35 páginasKey Concepts in Marketing: Maureen Castillo Dyna Enad Carelle Trisha Espital Ethel Silvasosoheart90Ainda não há avaliações

- Purpose and Types of Construction EstimatesDocumento10 páginasPurpose and Types of Construction EstimatesAisha MalikAinda não há avaliações

- 721-1002-000 Ad 0Documento124 páginas721-1002-000 Ad 0rashmi mAinda não há avaliações

- History-Complete Study NoteDocumento48 páginasHistory-Complete Study NoteRahul PandeyAinda não há avaliações

- Statutory Audit Fee Estimate for CNC Firm FY20-21Documento1 páginaStatutory Audit Fee Estimate for CNC Firm FY20-21Saad AkhtarAinda não há avaliações

- How To Become A Hacker - Haibo WuDocumento281 páginasHow To Become A Hacker - Haibo WuAlex de OliveiraAinda não há avaliações

- The Indian Navy - Inet (Officers)Documento3 páginasThe Indian Navy - Inet (Officers)ANKIT KUMARAinda não há avaliações

- Medtech LawsDocumento19 páginasMedtech LawsJon Nicole DublinAinda não há avaliações

- Phil Pharma Health Vs PfizerDocumento14 páginasPhil Pharma Health Vs PfizerChristian John Dela CruzAinda não há avaliações

- Trivandrum District IT Quiz Questions and Answers 2016 - IT Quiz PDFDocumento12 páginasTrivandrum District IT Quiz Questions and Answers 2016 - IT Quiz PDFABINAinda não há avaliações

- Mind Map All in One PBA-2021-08-20 12-38-51Documento1 páginaMind Map All in One PBA-2021-08-20 12-38-51MikosamirAinda não há avaliações

- RAS MARKAZ CRUDE OIL PARK SITE INSPECTION PROCEDUREDocumento1 páginaRAS MARKAZ CRUDE OIL PARK SITE INSPECTION PROCEDUREANIL PLAMOOTTILAinda não há avaliações

- Wa0010Documento3 páginasWa0010BRANDO LEONARDO ROJAS ROMEROAinda não há avaliações

- Qustion 2020-Man QB MCQ - MAN-22509 - VI SEME 2019-20Documento15 páginasQustion 2020-Man QB MCQ - MAN-22509 - VI SEME 2019-20Raees JamadarAinda não há avaliações

- Problematika Pengembangan Kurikulum Di Lembaga Pendidikan Islam: Tinjauan EpistimologiDocumento11 páginasProblematika Pengembangan Kurikulum Di Lembaga Pendidikan Islam: Tinjauan EpistimologiAhdanzulAinda não há avaliações

- Controlled Chaos in Joseph Heller's Catch-22Documento5 páginasControlled Chaos in Joseph Heller's Catch-22OliverAinda não há avaliações

- 4 - Factors Affecting ConformityDocumento8 páginas4 - Factors Affecting ConformityKirill MomohAinda não há avaliações

- IiuyiuDocumento2 páginasIiuyiuLudriderm ChapStickAinda não há avaliações

- Mobile phone controlled car locking systemDocumento13 páginasMobile phone controlled car locking systemKevin Adrian ZorillaAinda não há avaliações

- Human Resource Management in HealthDocumento7 páginasHuman Resource Management in HealthMark MadridanoAinda não há avaliações

- Test Bank For Goulds Pathophysiology For The Health Professions 5 Edition Karin C VanmeterDocumento36 páginasTest Bank For Goulds Pathophysiology For The Health Professions 5 Edition Karin C Vanmetermulctalinereuwlqu100% (41)