Você também pode gostar

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Yucca Mountain Safety Evaluation Report - Volume 2Documento665 páginasYucca Mountain Safety Evaluation Report - Volume 2The Heritage FoundationAinda não há avaliações

- Detailed Lesson Plan in Science 5Documento5 páginasDetailed Lesson Plan in Science 5hs4fptm82gAinda não há avaliações

- ARRI SkyPanel - DMX Protocol Specification V4.4Documento88 páginasARRI SkyPanel - DMX Protocol Specification V4.4Quan LyAinda não há avaliações

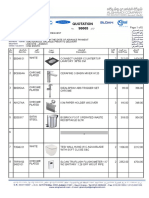

- Quotation 98665Documento5 páginasQuotation 98665Reda IsmailAinda não há avaliações

- Particle Swarm Optimization - WikipediaDocumento9 páginasParticle Swarm Optimization - WikipediaRicardo VillalongaAinda não há avaliações

- Fasteners Lecture 11-20-03Documento67 páginasFasteners Lecture 11-20-03laponggaAinda não há avaliações

- Chip DielDocumento45 páginasChip DielJUANCANEXTAinda não há avaliações

- Source 22Documento2 páginasSource 22Alexander FloresAinda não há avaliações

- Technical Owner Manual Nfinity v6Documento116 páginasTechnical Owner Manual Nfinity v6Tom MondjollianAinda não há avaliações

- Available Protocols in PcVueDocumento5 páginasAvailable Protocols in PcVueWan EzzatAinda não há avaliações

- OTM Reports FTI Training ManualDocumento78 páginasOTM Reports FTI Training ManualAquib Khan100% (2)

- National Power Training Institute: Admission Notice: 2020-21Documento3 páginasNational Power Training Institute: Admission Notice: 2020-21a.jainAinda não há avaliações

- Mumbai BylawsDocumento110 páginasMumbai BylawsLokesh SharmaAinda não há avaliações

- Metalband SawDocumento7 páginasMetalband SawRichard JongAinda não há avaliações

- Draft BLDocumento3 páginasDraft BLimam faodjiAinda não há avaliações

- Planning and Site Investigation in TunnellingDocumento6 páginasPlanning and Site Investigation in TunnellingJean DalyAinda não há avaliações

- Viewnet Diy PricelistDocumento2 páginasViewnet Diy PricelistKhay SaadAinda não há avaliações

- Ilovepdf Merged MergedDocumento209 páginasIlovepdf Merged MergedDeepak AgrawalAinda não há avaliações

- Dnvgl-Ru-Ships (2015) Part 3 Ch-10 TrolleyDocumento7 páginasDnvgl-Ru-Ships (2015) Part 3 Ch-10 TrolleyyogeshAinda não há avaliações

- En Privacy The Best Reseller SMM Panel, Cheap SEO and PR - MRPOPULARDocumento4 páginasEn Privacy The Best Reseller SMM Panel, Cheap SEO and PR - MRPOPULARZhenyuan LiAinda não há avaliações

- Mainframe Vol-II Version 1.2Documento246 páginasMainframe Vol-II Version 1.2Nikunj Agarwal100% (1)

- 2009 PMI CatalogueDocumento124 páginas2009 PMI Cataloguedesbennett004Ainda não há avaliações

- Suzuki B-King Indicator Mod CompleteDocumento9 páginasSuzuki B-King Indicator Mod Completehookuspookus1Ainda não há avaliações

- TIL 1881 Network Security TIL For Mark VI Controller Platform PDFDocumento11 páginasTIL 1881 Network Security TIL For Mark VI Controller Platform PDFManuel L LombarderoAinda não há avaliações

- VX-1700 Owners ManualDocumento32 páginasVX-1700 Owners ManualVan ThaoAinda não há avaliações

- CHE 322 - Gaseous Fuel ProblemsDocumento26 páginasCHE 322 - Gaseous Fuel ProblemsDanice LunaAinda não há avaliações

- Tutorial Class 1 Questions 1Documento2 páginasTutorial Class 1 Questions 1Bố Quỳnh ChiAinda não há avaliações

- Renewsys India Pvt. LTD.: Form Factor - 18 Cells Reference Drawing Numbers: Bom For C06 - 5Wp With Elmex JB Per ModuleDocumento31 páginasRenewsys India Pvt. LTD.: Form Factor - 18 Cells Reference Drawing Numbers: Bom For C06 - 5Wp With Elmex JB Per Modulesandeep devabhaktuniAinda não há avaliações

- Ecg Signal Thesis1Documento74 páginasEcg Signal Thesis1McSudul HasanAinda não há avaliações

- Jrules Installation onWEBSPHEREDocumento196 páginasJrules Installation onWEBSPHEREjagr123Ainda não há avaliações