Você também pode gostar

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (120)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Project Report On Credit RatingDocumento15 páginasProject Report On Credit RatingShambhu Kumar100% (4)

- Market Profile 102Documento44 páginasMarket Profile 102sinatra11235100% (4)

- Unit 6 Foreign Exchange Exposure: Sanjay Ghimire Tu-SomDocumento68 páginasUnit 6 Foreign Exchange Exposure: Sanjay Ghimire Tu-SomMotiram paudelAinda não há avaliações

- Trader's Psychology and Key Rules of Forex TradingDocumento3 páginasTrader's Psychology and Key Rules of Forex TradingAkingbemi MorakinyoAinda não há avaliações

- Chapter 10 Liabilities Power PointDocumento89 páginasChapter 10 Liabilities Power Pointgisel w100% (1)

- CBP Circular No. 905-82 December 10, 1982Documento6 páginasCBP Circular No. 905-82 December 10, 1982Emil BautistaAinda não há avaliações

- Multinational Financial ManagementDocumento95 páginasMultinational Financial ManagementAAinda não há avaliações

- Dubai Islamic Bank Results Update 16 AugustDocumento4 páginasDubai Islamic Bank Results Update 16 AugustEmran Lhr PakistanAinda não há avaliações

- CH 6 - Cost of Capital PDFDocumento49 páginasCH 6 - Cost of Capital PDFJanta RajaAinda não há avaliações

- Braden River High School BandsDocumento2 páginasBraden River High School BandsAlex MoralesAinda não há avaliações

- ENGINEERING ECONOMICS (18HS1T02) - Mid Term Exam (Back) - 2021-2022Documento2 páginasENGINEERING ECONOMICS (18HS1T02) - Mid Term Exam (Back) - 2021-2022sahu.tukun003Ainda não há avaliações

- Purchase Order No. 05873069 (40) Dated - 24 .07.2013Documento9 páginasPurchase Order No. 05873069 (40) Dated - 24 .07.2013Global LogisticsAinda não há avaliações

- Capital Structure and Dividen PolicyDocumento23 páginasCapital Structure and Dividen PolicyChristian DavidAinda não há avaliações

- Negotiable Instruments ActDocumento23 páginasNegotiable Instruments ActNarendran Kamal'iyan100% (1)

- Money PadDocumento15 páginasMoney PadSubhash PbsAinda não há avaliações

- Awb 6014931576Documento1 páginaAwb 6014931576SA ControlAinda não há avaliações

- Department of Business Administration Education FM 223 - Course SyllabusDocumento7 páginasDepartment of Business Administration Education FM 223 - Course SyllabusMari ParkAinda não há avaliações

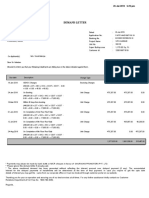

- Demand LetterDocumento2 páginasDemand LetterHimanshu RantiyaAinda não há avaliações

- DT Tax Laws 2021Documento1.060 páginasDT Tax Laws 2021Aluma MuzamilAinda não há avaliações

- Chapter 1 An Introduction To Accounting: Fundamental Financial Accounting Concepts, 10e (Edmonds)Documento53 páginasChapter 1 An Introduction To Accounting: Fundamental Financial Accounting Concepts, 10e (Edmonds)brockAinda não há avaliações

- Federal Ex Vs Antonio DIgestDocumento4 páginasFederal Ex Vs Antonio DIgestgrurocketAinda não há avaliações

- Chapter 4 - Present Worth AnalysisDocumento8 páginasChapter 4 - Present Worth AnalysisSandipAinda não há avaliações

- Monetary PolicyDocumento22 páginasMonetary PolicyHema BobadeAinda não há avaliações

- 1231.3376.01 -ל הרמהל ח"גאמ - Convertible ArbitrageDocumento3 páginas1231.3376.01 -ל הרמהל ח"גאמ - Convertible ArbitrageitzikhevronAinda não há avaliações

- Audit of Receivables: Cebu Cpar Center, IncDocumento10 páginasAudit of Receivables: Cebu Cpar Center, IncEvita Ayne TapitAinda não há avaliações

- Credit Insurance AaaaaDocumento21 páginasCredit Insurance AaaaaRohit GuptaAinda não há avaliações

- SHEKAR - Rural BankingDocumento20 páginasSHEKAR - Rural BankingkizieAinda não há avaliações

- Deductions in Gross EstateDocumento2 páginasDeductions in Gross EstateRAinda não há avaliações

- Chapter 15 Ppe Part 1Documento28 páginasChapter 15 Ppe Part 1marianAinda não há avaliações

- The Letter of Credit ProcessDocumento1 páginaThe Letter of Credit ProcessGirish RanganathanAinda não há avaliações