Você também pode gostar

- Midc Industries ListDocumento3 páginasMidc Industries ListTushar Malkar63% (8)

- Importance of Service Sector in India: Subject: Managerial EconomicsDocumento19 páginasImportance of Service Sector in India: Subject: Managerial EconomicsRamana ReddyAinda não há avaliações

- Importance of Service Sector in India: Subject: Managerial EconomicsDocumento20 páginasImportance of Service Sector in India: Subject: Managerial EconomicsDeepak SoniAinda não há avaliações

- Assignment On "Service Sector: The Future of Indian Economy"Documento19 páginasAssignment On "Service Sector: The Future of Indian Economy"VijayKumar NishadAinda não há avaliações

- What Is Service SectorDocumento17 páginasWhat Is Service Sectormsms_khatriAinda não há avaliações

- Service Sector in Indian EconomyDocumento5 páginasService Sector in Indian EconomyAvik SarkarAinda não há avaliações

- Service Operations Management Final NotesDocumento49 páginasService Operations Management Final Notessanan inamdarAinda não há avaliações

- Role of Service Sector in Modern Economic Development of India PDFDocumento3 páginasRole of Service Sector in Modern Economic Development of India PDFBiswajit PaulAinda não há avaliações

- Services OperationsDocumento44 páginasServices Operationssheebakbs5144Ainda não há avaliações

- Service Sector An OverviewDocumento10 páginasService Sector An OverviewFebbyAinda não há avaliações

- 1 Growing Importance of Services Sector For IndiaDocumento6 páginas1 Growing Importance of Services Sector For IndiaPriya AhujaAinda não há avaliações

- An Analysis of Services Sector in Indian EconomyDocumento5 páginasAn Analysis of Services Sector in Indian EconomyERAKACHEDU HARI PRASADAinda não há avaliações

- Unit 1 Services Marketing by Dr. Sanjay ManochaDocumento115 páginasUnit 1 Services Marketing by Dr. Sanjay ManochaAASTHA VERMAAinda não há avaliações

- Ruplal Sir's AssignmentDocumento9 páginasRuplal Sir's Assignmentemraan0099606Ainda não há avaliações

- Dena Ind. ProfileDocumento14 páginasDena Ind. ProfileDhaval MahatmaAinda não há avaliações

- Services 2013 ReportDocumento6 páginasServices 2013 Reportnishantjain95Ainda não há avaliações

- Service Sector in IndiaDocumento10 páginasService Sector in Indiamelsonj100% (1)

- India's Service Sector - Shaping Future of Indian Retail IndustryDocumento9 páginasIndia's Service Sector - Shaping Future of Indian Retail IndustryRajkumari AgrawalAinda não há avaliações

- Service SectorDocumento14 páginasService Sectoranjali shilpa kajalAinda não há avaliações

- Service SectorDocumento14 páginasService Sectorneeru792000Ainda não há avaliações

- INVESTMENT OPPORTUNITIES IN SERVICE SECTORS IN INDIA C 1222 PDFDocumento5 páginasINVESTMENT OPPORTUNITIES IN SERVICE SECTORS IN INDIA C 1222 PDFDEXGUN GUNAinda não há avaliações

- 1.1 Introduction Ot The SectorDocumento9 páginas1.1 Introduction Ot The SectorkanikashahsuratAinda não há avaliações

- International Journal of Advance & Innovative Research Volume 1, Issue 1 ISSN: 2394-7780Documento36 páginasInternational Journal of Advance & Innovative Research Volume 1, Issue 1 ISSN: 2394-7780empyrealAinda não há avaliações

- Year GDPDocumento9 páginasYear GDPishwaryaAinda não há avaliações

- About Service IndustryDocumento12 páginasAbout Service IndustrySaeesh Pai KakodeAinda não há avaliações

- Reliance Communications LimitedDocumento35 páginasReliance Communications LimitedRajat BaliyanAinda não há avaliações

- Service Led Growth in India Gbs Write UpDocumento9 páginasService Led Growth in India Gbs Write UpSIMRAN SHOKEENAinda não há avaliações

- ConclusionDocumento11 páginasConclusiongayatrimaravarAinda não há avaliações

- Service Sector in Indian EconomyDocumento20 páginasService Sector in Indian EconomyShivshaktiRanjanAinda não há avaliações

- Performance of Indian Service SectorDocumento40 páginasPerformance of Indian Service SectorHema BhargaviAinda não há avaliações

- Report ReferencesDocumento6 páginasReport ReferencesNaveen KumarAinda não há avaliações

- Chapter-1: An Organization Study at Future Group CoDocumento47 páginasChapter-1: An Organization Study at Future Group Cochethan kumar.sAinda não há avaliações

- Service SectorDocumento4 páginasService Sectoraakanksha1janAinda não há avaliações

- Services-Led Industrialization in India: Assessment and LessonsDocumento57 páginasServices-Led Industrialization in India: Assessment and LessonsRishabh ManglikAinda não há avaliações

- Eco Essay On TheDocumento12 páginasEco Essay On ThemasoodAinda não há avaliações

- Sasi Report 1Documento23 páginasSasi Report 1Sasi KumarAinda não há avaliações

- Equity ValuationDocumento18 páginasEquity ValuationAbhishek NagpalAinda não há avaliações

- Assignment OF Service Marketing: Submitted byDocumento10 páginasAssignment OF Service Marketing: Submitted bymanalibhardwajAinda não há avaliações

- Performance of India's Service SectorDocumento9 páginasPerformance of India's Service SectorutsavAinda não há avaliações

- Service Sector ASSIGNEMENTDocumento3 páginasService Sector ASSIGNEMENTJagjeet S. BhardwajAinda não há avaliações

- Macro Eco - Service SectorDocumento22 páginasMacro Eco - Service SectorTejas Singh PanwarAinda não há avaliações

- Service SectorDocumento34 páginasService SectorRavikrishna NagarajanAinda não há avaliações

- Services Sector: S S: I CDocumento25 páginasServices Sector: S S: I CGomathiRachakondaAinda não há avaliações

- KPMG The Indian Services Sector Poised For Global AscendancyDocumento282 páginasKPMG The Indian Services Sector Poised For Global Ascendancyrahulp9999Ainda não há avaliações

- Service Operations Management AssignmentDocumento5 páginasService Operations Management AssignmentSai Krishna Teja PamulaparthiAinda não há avaliações

- Lalalajpatrai College: Subject: Service Sector ManagementDocumento30 páginasLalalajpatrai College: Subject: Service Sector ManagementShweta VaghelaAinda não há avaliações

- Service Sector in IndiaDocumento3 páginasService Sector in Indiaabhi4all3Ainda não há avaliações

- Services July 2019Documento31 páginasServices July 2019AkshayAinda não há avaliações

- How Do Tertiary Sectors Contribute To The Indian Economy?Documento11 páginasHow Do Tertiary Sectors Contribute To The Indian Economy?SOHEL BANGIAinda não há avaliações

- Service Sector and Its Role in Indian EconomyDocumento12 páginasService Sector and Its Role in Indian EconomyTage Nobin100% (1)

- Is Service-Led Growth A Miracle For IndiaDocumento42 páginasIs Service-Led Growth A Miracle For IndiaDivya SreenivasAinda não há avaliações

- Project Report ON: Customer SatisfationDocumento74 páginasProject Report ON: Customer Satisfationnightking_1Ainda não há avaliações

- Unit 10 Service Sector: StructureDocumento20 páginasUnit 10 Service Sector: StructureTushar PunjaniAinda não há avaliações

- Ecoooooooooooooooooooooooooooo....... Did It..Documento17 páginasEcoooooooooooooooooooooooooooo....... Did It..JainPalashAinda não há avaliações

- India's Services SectorDocumento146 páginasIndia's Services SectorInsideout100% (37)

- Emerging FinTech: Understanding and Maximizing Their BenefitsNo EverandEmerging FinTech: Understanding and Maximizing Their BenefitsAinda não há avaliações

- Exporting Services: A Developing Country PerspectiveNo EverandExporting Services: A Developing Country PerspectiveNota: 5 de 5 estrelas5/5 (2)

- Provincial Facilitation for Investment and Trade Index: Measuring Economic Governance for Business Development in the Lao People’s Democratic Republic-Second EditionNo EverandProvincial Facilitation for Investment and Trade Index: Measuring Economic Governance for Business Development in the Lao People’s Democratic Republic-Second EditionAinda não há avaliações

- Policies to Support the Development of Indonesia’s Manufacturing Sector during 2020–2024: A Joint ADB–BAPPENAS ReportNo EverandPolicies to Support the Development of Indonesia’s Manufacturing Sector during 2020–2024: A Joint ADB–BAPPENAS ReportAinda não há avaliações

- Tajikistan: Promoting Export Diversification and GrowthNo EverandTajikistan: Promoting Export Diversification and GrowthAinda não há avaliações

- Moving up the Value Chain: The Road Ahead for Indian It ExportersNo EverandMoving up the Value Chain: The Road Ahead for Indian It ExportersAinda não há avaliações

- Bse Listed CompaniesDocumento35 páginasBse Listed CompaniesVikas SinghAinda não há avaliações

- Up PDFDocumento225 páginasUp PDFajay_430Ainda não há avaliações

- Role of Micro, Small and Medium Enterprises (MSME) in Rural Transformation and Consequent Economic Growth of IndiaDocumento8 páginasRole of Micro, Small and Medium Enterprises (MSME) in Rural Transformation and Consequent Economic Growth of IndiaInternational Journal of Innovative Science and Research TechnologyAinda não há avaliações

- TradeableHoldings 6 4 2019 PDFDocumento2 páginasTradeableHoldings 6 4 2019 PDFDhwani ShahAinda não há avaliações

- MROs PDFDocumento6 páginasMROs PDFhem singhAinda não há avaliações

- 1563788375467Documento32 páginas1563788375467Ritusree BasuAinda não há avaliações

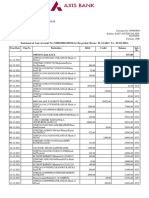

- Statement of Axis Account No:920010006130934 For The Period (From: 01-12-2021 To: 09-05-2022)Documento13 páginasStatement of Axis Account No:920010006130934 For The Period (From: 01-12-2021 To: 09-05-2022)subhadeepAinda não há avaliações

- Share Market PricesDocumento52 páginasShare Market Pricesvishalsharma8522Ainda não há avaliações

- Ministry Wise Main Schemes Doc Updated Part-1 Lyst2795Documento289 páginasMinistry Wise Main Schemes Doc Updated Part-1 Lyst2795VIBHAKAR SINGHAinda não há avaliações

- 4987234Documento7 páginas4987234venkatesh_1829Ainda não há avaliações

- FR CSM 21 Engl 300522 - 0Documento15 páginasFR CSM 21 Engl 300522 - 0VIKAS SANGWANAinda não há avaliações

- Column1 53% 27% 74%: Enrollment ID Name Batch KNTYW224A05 Phase Phase Test-3Documento1 páginaColumn1 53% 27% 74%: Enrollment ID Name Batch KNTYW224A05 Phase Phase Test-3Soumabho PalAinda não há avaliações

- Good Service Tax (GST) Exam Week 3Documento2 páginasGood Service Tax (GST) Exam Week 3M Daiko S PAinda não há avaliações

- BamboDocumento13 páginasBambojaspreet kahlonAinda não há avaliações

- Analysis of Trends, Composition and Direction of India's Foreign Trade Since 2000Documento37 páginasAnalysis of Trends, Composition and Direction of India's Foreign Trade Since 2000venkatimAinda não há avaliações

- List of Successful Students in JEE (Advanced) 2020 From FIITJEE Non Classroom ProgramDocumento26 páginasList of Successful Students in JEE (Advanced) 2020 From FIITJEE Non Classroom ProgramVikash KumarAinda não há avaliações

- Acct Statement - XX0447 - 26062023Documento20 páginasAcct Statement - XX0447 - 26062023Mr UnknownAinda não há avaliações

- GDP AssignmentDocumento7 páginasGDP AssignmentIshpreet SinghAinda não há avaliações

- Baza de Date ImproDocumento92 páginasBaza de Date ImproAlin LupuAinda não há avaliações

- Indian Models of Economy Business and MaDocumento5 páginasIndian Models of Economy Business and Mamanny201620Ainda não há avaliações

- Itbm Ayush Sharma FT DDocumento14 páginasItbm Ayush Sharma FT DAyushAinda não há avaliações

- Nava RatnaDocumento19 páginasNava RatnaMadhu Mahesh RajAinda não há avaliações

- Economic Reforms in IndiaDocumento29 páginasEconomic Reforms in IndiaVishnu BralAinda não há avaliações

- Bfsi ListDocumento8 páginasBfsi ListShantanu AnandAinda não há avaliações

- Acct Statement - XX6419 - 05012022Documento22 páginasAcct Statement - XX6419 - 05012022AartiAinda não há avaliações

- Frmt5: Frret6Tq,@Documento3 páginasFrmt5: Frret6Tq,@VinothAinda não há avaliações

- Scrip MasterDocumento234 páginasScrip MasterjavajaganAinda não há avaliações

- Indian Economy On The Eve of IndependenceDocumento17 páginasIndian Economy On The Eve of IndependenceNoorunnishaAinda não há avaliações

- Economic Reforms Since 1991 or New Economic PolicyDocumento14 páginasEconomic Reforms Since 1991 or New Economic PolicyAnu Sikka100% (4)