Você também pode gostar

- Exercises Chapter1Documento4 páginasExercises Chapter1Huyen Siu NhưnAinda não há avaliações

- Forum 6Documento1 páginaForum 6cecillia lissawatiAinda não há avaliações

- CH 06Documento50 páginasCH 06Dr-Bahaaeddin Alareeni100% (1)

- Tutorial Laporan Arus KasDocumento17 páginasTutorial Laporan Arus KasRatna DwiAinda não há avaliações

- Consolidated Financial Statement Practice 3-2Documento2 páginasConsolidated Financial Statement Practice 3-2Winnie TanAinda não há avaliações

- Exercise - Dilutive Securities - AdillaikhsaniDocumento4 páginasExercise - Dilutive Securities - Adillaikhsaniaidil fikri ikhsan100% (1)

- Syukur Tugas Akl IiDocumento3 páginasSyukur Tugas Akl IiMuhammad SyukurAinda não há avaliações

- Audit of Other Income Statement ComponentsDocumento7 páginasAudit of Other Income Statement ComponentsIbratama Sukses PratamaAinda não há avaliações

- Accounting For LeasesDocumento112 páginasAccounting For LeasesPoomza TaramarukAinda não há avaliações

- CH16Documento80 páginasCH16mahinAinda não há avaliações

- Variance Analysi1Documento2 páginasVariance Analysi1Elliot RichardAinda não há avaliações

- Contoh Dan Soal Cash FlowDocumento9 páginasContoh Dan Soal Cash FlowAltaf HauzanAinda não há avaliações

- The Statement of Financial Position of Stancia Sa at DecemberDocumento1 páginaThe Statement of Financial Position of Stancia Sa at DecemberCharlotte100% (1)

- Exercise - Dilutive Securities - AdillaikhsaniDocumento4 páginasExercise - Dilutive Securities - Adillaikhsaniaidil fikri ikhsanAinda não há avaliações

- Belinda 125150469 OY E7-14. On April 1, 2015, Prince Company Assigns $500,000 of Its Accounts Receivable To TheDocumento1 páginaBelinda 125150469 OY E7-14. On April 1, 2015, Prince Company Assigns $500,000 of Its Accounts Receivable To ThebelindaAinda não há avaliações

- Problem 18 - 18 18 - 31 and 18 - 32Documento5 páginasProblem 18 - 18 18 - 31 and 18 - 32anon_459698449Ainda não há avaliações

- Ch.16 Dilutive Securities and Earnings Per Share: Chapter Learning ObjectivesDocumento7 páginasCh.16 Dilutive Securities and Earnings Per Share: Chapter Learning ObjectivesFaishal Alghi FariAinda não há avaliações

- SOAL LATIHAN MK - AKL - FC TransactionsDocumento4 páginasSOAL LATIHAN MK - AKL - FC Transactionscaca natalia100% (1)

- Latihan Soal Akuntansi Untuk PensionDocumento4 páginasLatihan Soal Akuntansi Untuk PensionRini SusantyAinda não há avaliações

- Working 3Documento6 páginasWorking 3Hà Lê DuyAinda não há avaliações

- Quiz - Inter 2 UTS - Wo AnsDocumento3 páginasQuiz - Inter 2 UTS - Wo AnsNike HannaAinda não há avaliações

- 1 Intermediate Accounting IFRS 3rd Edition-554-569Documento16 páginas1 Intermediate Accounting IFRS 3rd Edition-554-569Khofifah SalmahAinda não há avaliações

- Meyerson S Bakery Is Considering The Addition of A New LineDocumento1 páginaMeyerson S Bakery Is Considering The Addition of A New LineLet's Talk With HassanAinda não há avaliações

- Income Statement, EPSDocumento2 páginasIncome Statement, EPSHolly Motley50% (2)

- P11Documento7 páginasP11Arif RahmanAinda não há avaliações

- Uas AKMDocumento14 páginasUas AKMThorieq Mulya MiladyAinda não há avaliações

- Sesi 9 & 10 Praktikum - SharedDocumento9 páginasSesi 9 & 10 Praktikum - SharedDian Permata SariAinda não há avaliações

- Accounting Textbook Solutions - 39Documento19 páginasAccounting Textbook Solutions - 39acc-expert0% (1)

- ABC, Resource Drivers, Service Industry Glencoe Medical Clinic Operates A Cardiology Care Unit and A Maternity Care UnitDocumento3 páginasABC, Resource Drivers, Service Industry Glencoe Medical Clinic Operates A Cardiology Care Unit and A Maternity Care UnitKailash KumarAinda não há avaliações

- Ac557 W3 HW HBDocumento2 páginasAc557 W3 HW HBHasan Barakat100% (2)

- Udah Bener'Documento4 páginasUdah Bener'Shafa AzahraAinda não há avaliações

- 17-38 Transferred-In Costs, Weighted-Average Method. Bookworm, Inc., Has TwoDocumento6 páginas17-38 Transferred-In Costs, Weighted-Average Method. Bookworm, Inc., Has TwoMajd MustafaAinda não há avaliações

- Benefits AccountingDocumento4 páginasBenefits AccountingJulian Christopher Torcuator50% (2)

- Chapter 09 Indirect and Mutual HoldingsDocumento12 páginasChapter 09 Indirect and Mutual HoldingsNicolas ErnestoAinda não há avaliações

- Slide Akuntansi ManahemenDocumento10 páginasSlide Akuntansi ManahemenHandaru Edit Sasongko0% (1)

- Body EmailDocumento2 páginasBody Emailferry firmannaAinda não há avaliações

- Adjusted Retained Earnings StatementDocumento2 páginasAdjusted Retained Earnings StatementSerazul Arafin MrinmoyAinda não há avaliações

- Pertemuan 8 Chapter 17Documento29 páginasPertemuan 8 Chapter 17Jordan Siahaan100% (1)

- KidsTravel Produces Car Seats For Children From Newborn To 2 Years OldDocumento2 páginasKidsTravel Produces Car Seats For Children From Newborn To 2 Years OldElliot Richard0% (1)

- Soal UTS Financial AuditDocumento4 páginasSoal UTS Financial AuditIkhsan Uiandra Putra SitorusAinda não há avaliações

- E7-39 Comparing ABC and Plantwide Overhead Cost Assigments: Setup Hours Oven HoursDocumento3 páginasE7-39 Comparing ABC and Plantwide Overhead Cost Assigments: Setup Hours Oven HoursDhiva Rianitha Manurung100% (1)

- Bab 6 Intercompany Profit TransactionsDocumento2 páginasBab 6 Intercompany Profit TransactionsAnonymous dMkY9G2Ainda não há avaliações

- BINUS University: Undergraduate / Master / Doctoral ) International/Regular/Smart Program/Global Class )Documento3 páginasBINUS University: Undergraduate / Master / Doctoral ) International/Regular/Smart Program/Global Class )Audrey NataliaAinda não há avaliações

- 11.3 Break Even in Units ($75,000/15,000 Units) - Fixed Cost Is $37,500Documento14 páginas11.3 Break Even in Units ($75,000/15,000 Units) - Fixed Cost Is $37,500Rizzah Nianiah100% (1)

- E22-6 (LO 2) Accounting Changes-DepreciationDocumento6 páginasE22-6 (LO 2) Accounting Changes-DepreciationRiana DeztianiAinda não há avaliações

- CH 14Documento2 páginasCH 14tigger5191100% (1)

- ACCT550 Homework Week 1Documento6 páginasACCT550 Homework Week 1Natasha DeclanAinda não há avaliações

- Be16 P16 2aDocumento7 páginasBe16 P16 2aLisa Hammerle ClarkAinda não há avaliações

- Exercise 21Documento3 páginasExercise 21Ruth UtamiAinda não há avaliações

- IFRS 15 Session4 Handout 1Documento2 páginasIFRS 15 Session4 Handout 1Simon YossefAinda não há avaliações

- InstructionsDocumento2 páginasInstructionsGabriel SAinda não há avaliações

- تابع فصل ادارة المخزونDocumento1 páginaتابع فصل ادارة المخزونAhmed El KhateebAinda não há avaliações

- P 6-3 DrebinDocumento6 páginasP 6-3 DrebinJulia Pratiwi ParhusipAinda não há avaliações

- Soal GSLC-6 Advanced AccountingDocumento2 páginasSoal GSLC-6 Advanced AccountingEunice ShevlinAinda não há avaliações

- Soal Debt InvestmentDocumento5 páginasSoal Debt InvestmentKyle Kuro0% (1)

- Debt Investments TutorialDocumento4 páginasDebt Investments TutorialRawan YasserAinda não há avaliações

- ACCT336 Solved Exercises - Chapters 14 and 15Documento5 páginasACCT336 Solved Exercises - Chapters 14 and 15kareemrawwadAinda não há avaliações

- Additional Solutions - Chapter 15Documento24 páginasAdditional Solutions - Chapter 15maxima0078Ainda não há avaliações

- Solution Manual For Financial Accounting in An Economic Context 10th Edition Pratt PetersDocumento37 páginasSolution Manual For Financial Accounting in An Economic Context 10th Edition Pratt PetersLauraEllisrkgp100% (43)

- ACY4001 1920 S2 Individual Assignment 3Documento1 páginaACY4001 1920 S2 Individual Assignment 3Morris LoAinda não há avaliações

- ACY4001 1920 S2 Individual Assignment 3Documento1 páginaACY4001 1920 S2 Individual Assignment 3Morris LoAinda não há avaliações

- ACY4001 1920 S2 Individual Assignment 4Documento3 páginasACY4001 1920 S2 Individual Assignment 4Morris LoAinda não há avaliações

- ACY4001 Advanced Accounting 1 - Individual Assignment 2 - Ch17Documento2 páginasACY4001 Advanced Accounting 1 - Individual Assignment 2 - Ch17Morris LoAinda não há avaliações

- F7 - Hkas 33Documento2 páginasF7 - Hkas 33Morris LoAinda não há avaliações

- Assignment Tax LawDocumento31 páginasAssignment Tax LawZohaib BabarAinda não há avaliações

- Audit Report 2019-20 To DAG CAE On 06-02-2020 KarachiDocumento225 páginasAudit Report 2019-20 To DAG CAE On 06-02-2020 KarachiAbc DefAinda não há avaliações

- Full Text Tax First Set Lifeblood TheoryDocumento18 páginasFull Text Tax First Set Lifeblood TheorySu Kings AbetoAinda não há avaliações

- Torrent Gas Private Limited: Application For Franchisee CNG StationDocumento9 páginasTorrent Gas Private Limited: Application For Franchisee CNG Stationmaulesh1982Ainda não há avaliações

- 2010-01-12 123253 IntermediateDocumento10 páginas2010-01-12 123253 IntermediateYoshidaAinda não há avaliações

- Topic 5 - Part1Documento45 páginasTopic 5 - Part1Minato MeaAinda não há avaliações

- CMA Class 1 A FDocumento58 páginasCMA Class 1 A FRithesh KAinda não há avaliações

- Chapter 3 Review PDFDocumento5 páginasChapter 3 Review PDFAisha KhanAinda não há avaliações

- Kashato Shirts: General JournalDocumento34 páginasKashato Shirts: General JournalJade Cruz100% (1)

- Ashiana AR 2019 20Documento240 páginasAshiana AR 2019 20Dhrubajyoti DattaAinda não há avaliações

- Solution Manual Cost Accounting 14th Ed by Carter PDFDocumento720 páginasSolution Manual Cost Accounting 14th Ed by Carter PDFUmar Sarfraz KhanAinda não há avaliações

- Alaska Journal - ConocoPhillipsDocumento1 páginaAlaska Journal - ConocoPhillipsREandoAinda não há avaliações

- Format EdelweisDocumento48 páginasFormat EdelweisabcAinda não há avaliações

- Finance Act 2010Documento5 páginasFinance Act 2010Tapia MelvinAinda não há avaliações

- Chapter 1 Overview of Cost ControlDocumento11 páginasChapter 1 Overview of Cost ControlCaren SilvaAinda não há avaliações

- Scope of Work For Corporate & Tax ConsultantDocumento10 páginasScope of Work For Corporate & Tax ConsultantStartup CAAinda não há avaliações

- Organisational Study On Titagarh Wagons LTD, by Sidharh Singhee (Final)Documento51 páginasOrganisational Study On Titagarh Wagons LTD, by Sidharh Singhee (Final)Sidharth SingheeAinda não há avaliações

- Filipinas Life Assurance Company v. Court of Tax Appeals GR No. L-21258Documento27 páginasFilipinas Life Assurance Company v. Court of Tax Appeals GR No. L-21258rowela jane paanoAinda não há avaliações

- Accounting For Share Capital TransactionsDocumento6 páginasAccounting For Share Capital TransactionsJessa Mae Banse50% (2)

- Acelec 331 Midterm Exam: MC QuestionsDocumento7 páginasAcelec 331 Midterm Exam: MC Questionshwo0% (1)

- Cost Accounting: Sixteenth EditionDocumento30 páginasCost Accounting: Sixteenth EditionHIMANSHU AGRAWALAinda não há avaliações

- Advanced Accounting: Translation of Financial Statements of Foreign AffiliatesDocumento27 páginasAdvanced Accounting: Translation of Financial Statements of Foreign AffiliatesSoniea DianiAinda não há avaliações

- Module 2c Notes ReceivableDocumento35 páginasModule 2c Notes ReceivableChen HaoAinda não há avaliações

- One Year After Acquisition: Consolidated F.SDocumento4 páginasOne Year After Acquisition: Consolidated F.SAngel Dela Cruz CoAinda não há avaliações

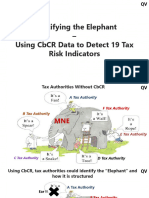

- 19 Tax Risk Indicators in CBCRDocumento22 páginas19 Tax Risk Indicators in CBCRidan28Ainda não há avaliações

- Ready ReckonerDocumento72 páginasReady ReckonerSRINIVAS SEESALAAinda não há avaliações

- Q1: Jan 2018: Deferred Tax Liabilities Deferred Tax AssetsDocumento17 páginasQ1: Jan 2018: Deferred Tax Liabilities Deferred Tax AssetsCliAinda não há avaliações

- Tcs Financial ProjectionsDocumento6 páginasTcs Financial Projectionsjohnna louella vicedo borjaAinda não há avaliações

- Chương 3Documento22 páginasChương 3Mai Duong ThiAinda não há avaliações

- English Allied Traders PLC Has A Wide Range of ManufacturingDocumento2 páginasEnglish Allied Traders PLC Has A Wide Range of ManufacturingAmit Pandey0% (1)

- The 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamNo EverandThe 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamAinda não há avaliações

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNo EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialAinda não há avaliações

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistNo EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistNota: 4.5 de 5 estrelas4.5/5 (73)

- The Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceNo EverandThe Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceNota: 4 de 5 estrelas4/5 (1)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNo EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNota: 4.5 de 5 estrelas4.5/5 (32)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaNo EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaNota: 4.5 de 5 estrelas4.5/5 (14)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNNo Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNNota: 4.5 de 5 estrelas4.5/5 (3)

- Mind over Money: The Psychology of Money and How to Use It BetterNo EverandMind over Money: The Psychology of Money and How to Use It BetterNota: 4 de 5 estrelas4/5 (24)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingNo EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingNota: 4.5 de 5 estrelas4.5/5 (17)

- Venture Deals: Be Smarter Than Your Lawyer and Venture CapitalistNo EverandVenture Deals: Be Smarter Than Your Lawyer and Venture CapitalistNota: 4 de 5 estrelas4/5 (32)

- The Value of a Whale: On the Illusions of Green CapitalismNo EverandThe Value of a Whale: On the Illusions of Green CapitalismNota: 5 de 5 estrelas5/5 (2)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaNo EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaNota: 3.5 de 5 estrelas3.5/5 (8)

- John D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthNo EverandJohn D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthNota: 4 de 5 estrelas4/5 (20)

- Corporate Finance Formulas: A Simple IntroductionNo EverandCorporate Finance Formulas: A Simple IntroductionNota: 4 de 5 estrelas4/5 (8)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successNo EverandReady, Set, Growth hack:: A beginners guide to growth hacking successNota: 4.5 de 5 estrelas4.5/5 (93)

- An easy approach to trading with bollinger bands: How to learn how to use Bollinger bands to trade online successfullyNo EverandAn easy approach to trading with bollinger bands: How to learn how to use Bollinger bands to trade online successfullyNota: 3 de 5 estrelas3/5 (1)

- Creating Shareholder Value: A Guide For Managers And InvestorsNo EverandCreating Shareholder Value: A Guide For Managers And InvestorsNota: 4.5 de 5 estrelas4.5/5 (8)

- YouTube Marketing: Comprehensive Beginners Guide to Learn YouTube Marketing, Tips & Secrets to Growth Hacking Your Channel and Building Profitable Passive Income Business OnlineNo EverandYouTube Marketing: Comprehensive Beginners Guide to Learn YouTube Marketing, Tips & Secrets to Growth Hacking Your Channel and Building Profitable Passive Income Business OnlineNota: 4.5 de 5 estrelas4.5/5 (2)

- Financial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityNo EverandFinancial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityNota: 4.5 de 5 estrelas4.5/5 (4)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisNo EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisNota: 5 de 5 estrelas5/5 (6)

- The Illusion of Innovation: Escape "Efficiency" and Unleash Radical ProgressNo EverandThe Illusion of Innovation: Escape "Efficiency" and Unleash Radical ProgressAinda não há avaliações

- Mastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsNo EverandMastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsAinda não há avaliações