Você também pode gostar

- Apprentice Cable Splicer (2902)Documento14 páginasApprentice Cable Splicer (2902)andresboy123Ainda não há avaliações

- Bond Analysis From BloombergDocumento10 páginasBond Analysis From BloombergAnonymous 31fa2FAPhAinda não há avaliações

- Credit Default SwapsDocumento14 páginasCredit Default SwapsAmit GandhiAinda não há avaliações

- Fabozzi Gupta MarDocumento16 páginasFabozzi Gupta MarFernanda RodriguesAinda não há avaliações

- Chapter 5: INTEREST RATE Derivatives: Forwards and SwapsDocumento69 páginasChapter 5: INTEREST RATE Derivatives: Forwards and SwapsDarshan raoAinda não há avaliações

- Cds - Heading Towards More Stable SystemDocumento28 páginasCds - Heading Towards More Stable SystemReadEverythingAinda não há avaliações

- Use Duration and Convexity To Measure RiskDocumento4 páginasUse Duration and Convexity To Measure RiskSreenesh PaiAinda não há avaliações

- Understanding Sovereign RiskDocumento7 páginasUnderstanding Sovereign Risk1234567899525Ainda não há avaliações

- Callable BrochureDocumento37 páginasCallable BrochurePratik MhatreAinda não há avaliações

- Principal Protected Investments: Structured Investments Solution SeriesDocumento8 páginasPrincipal Protected Investments: Structured Investments Solution SeriessonystdAinda não há avaliações

- PzenaCommentary Second Quarter 2013Documento3 páginasPzenaCommentary Second Quarter 2013CanadianValueAinda não há avaliações

- Ishares Portfolio Analytics Coskew and CoKurt VBA3Documento178 páginasIshares Portfolio Analytics Coskew and CoKurt VBA3Peter Urbani100% (1)

- 1 - Petrobras - DeepWater Gas LiftDocumento36 páginas1 - Petrobras - DeepWater Gas LiftNisar KhanAinda não há avaliações

- Section 3 - SwapsDocumento49 páginasSection 3 - SwapsEric FahertyAinda não há avaliações

- CLO Investing: With an Emphasis on CLO Equity & BB NotesNo EverandCLO Investing: With an Emphasis on CLO Equity & BB NotesAinda não há avaliações

- Citi TTS Seminar BASEL III Intraday LiquidityDocumento13 páginasCiti TTS Seminar BASEL III Intraday LiquidityCezara EminescuAinda não há avaliações

- CDS Presentation With References PDFDocumento42 páginasCDS Presentation With References PDF2401824Ainda não há avaliações

- Why Distributions Matter (16 Jan 2012)Documento43 páginasWhy Distributions Matter (16 Jan 2012)Peter UrbaniAinda não há avaliações

- Swaps Cms CMTDocumento7 páginasSwaps Cms CMTmarketfolly.comAinda não há avaliações

- Currency OverlayDocumento6 páginasCurrency OverlayprankyaquariusAinda não há avaliações

- Singular Spectrum Analysis Demo With VBADocumento12 páginasSingular Spectrum Analysis Demo With VBAPeter UrbaniAinda não há avaliações

- Fixed Income (Debt) Securities: Source: CFA IF Chapter 9 (Coverage of CH 9 Is MUST For Students)Documento17 páginasFixed Income (Debt) Securities: Source: CFA IF Chapter 9 (Coverage of CH 9 Is MUST For Students)Oona NiallAinda não há avaliações

- Chapter 6-Process Costing: LO1 LO2 LO3 LO4 LO5 LO6 LO7 LO8Documento68 páginasChapter 6-Process Costing: LO1 LO2 LO3 LO4 LO5 LO6 LO7 LO8Jose Dula IIAinda não há avaliações

- Dual Range AccrualsDocumento1 páginaDual Range AccrualszdfgbsfdzcgbvdfcAinda não há avaliações

- Lecture 4 2016 ALMDocumento70 páginasLecture 4 2016 ALMEmilioAinda não há avaliações

- DXF FormatDocumento208 páginasDXF Formatthigopal100% (1)

- John Carpenter, Bank of America, Introduction To CVA, DVA, FVA, UNC Charlotte Math Finance Seminar Series, 2014Documento17 páginasJohn Carpenter, Bank of America, Introduction To CVA, DVA, FVA, UNC Charlotte Math Finance Seminar Series, 2014IslaCanelaAinda não há avaliações

- Intra-Horizon VaR and Expected Shortfall Spreadsheet With VBADocumento7 páginasIntra-Horizon VaR and Expected Shortfall Spreadsheet With VBAPeter Urbani0% (1)

- UBS Synthetic CDOsDocumento6 páginasUBS Synthetic CDOsarahmedAinda não há avaliações

- SSRN Id2036979Documento26 páginasSSRN Id2036979aukie999Ainda não há avaliações

- Vanguard Principles InvestingDocumento40 páginasVanguard Principles InvestingRemo RaulisonAinda não há avaliações

- ATM SwaptionsDocumento7 páginasATM SwaptionssajivshrivAinda não há avaliações

- Convexity Adjustments and Forward Libor ModelDocumento19 páginasConvexity Adjustments and Forward Libor ModelfinenggAinda não há avaliações

- Bank Loans: Market Dynamics Poised To Deliver Attractive Risk-Adjusted ReturnsDocumento6 páginasBank Loans: Market Dynamics Poised To Deliver Attractive Risk-Adjusted ReturnsSabin NiculaeAinda não há avaliações

- Citi CVA ExampleDocumento29 páginasCiti CVA Examplepriak11Ainda não há avaliações

- UBS Bonds ArticleDocumento46 páginasUBS Bonds Articlesouto123Ainda não há avaliações

- (Bank of America) Credit Strategy - Monolines - A Potential CDS Settlement DisasterDocumento9 páginas(Bank of America) Credit Strategy - Monolines - A Potential CDS Settlement Disaster00aaAinda não há avaliações

- Introduction To DerivativesDocumento39 páginasIntroduction To DerivativesNagula Bala Ajesh GoudAinda não há avaliações

- FX 102 - FX Rates and ArbitrageDocumento32 páginasFX 102 - FX Rates and Arbitragetesting1997Ainda não há avaliações

- CLO Liquidity Provision and the Volcker Rule: Implications on the Corporate Bond MarketNo EverandCLO Liquidity Provision and the Volcker Rule: Implications on the Corporate Bond MarketAinda não há avaliações

- Money Market Black SwanDocumento29 páginasMoney Market Black SwanZerohedgeAinda não há avaliações

- Interest Rate Modelling A Matlab ImplementationDocumento41 páginasInterest Rate Modelling A Matlab ImplementationBen Salah MounaAinda não há avaliações

- Exchange Rate Determination Puzzle: Long Run Behavior and Short Run DynamicsNo EverandExchange Rate Determination Puzzle: Long Run Behavior and Short Run DynamicsAinda não há avaliações

- Investments & RiskDocumento20 páginasInvestments & RiskravaladityaAinda não há avaliações

- m339d Lecture Fourteen Binomial Option Pricing One Period PDFDocumento9 páginasm339d Lecture Fourteen Binomial Option Pricing One Period PDFPriyanka ChampatiAinda não há avaliações

- Swaps NewDocumento46 páginasSwaps NewJoseph Anbarasu100% (5)

- Bloomberg Professional For Bond Pricing & Yield To MaturityDocumento5 páginasBloomberg Professional For Bond Pricing & Yield To MaturityjujonetAinda não há avaliações

- SOP-Procedure Calibration of Metal TapesDocumento12 páginasSOP-Procedure Calibration of Metal Tapeshaharamesh100% (1)

- Python SyllabusDocumento6 páginasPython SyllabusVenkat KancherlaAinda não há avaliações

- FX Risk ManagementDocumento27 páginasFX Risk ManagementSMO979100% (1)

- Topic 3 Bonds VolatilityDocumento68 páginasTopic 3 Bonds Volatilityjason leeAinda não há avaliações

- Bond Pricing and Bond Yield SRPM2012Documento57 páginasBond Pricing and Bond Yield SRPM2012ashishbansal85Ainda não há avaliações

- ArbitrageDocumento3 páginasArbitragebhavnesh_muthaAinda não há avaliações

- DCM For LSEDocumento14 páginasDCM For LSEAlbert TsouAinda não há avaliações

- Capital Market AssumptionsDocumento19 páginasCapital Market AssumptionsKerim GokayAinda não há avaliações

- Auto Call Able SDocumento37 páginasAuto Call Able SAnkit VermaAinda não há avaliações

- Index Futures RMFDDocumento17 páginasIndex Futures RMFDAbhi_The_RockstarAinda não há avaliações

- Eun8e CH 005 PPTDocumento47 páginasEun8e CH 005 PPTannAinda não há avaliações

- Capm and AptDocumento10 páginasCapm and AptRajkumar35Ainda não há avaliações

- Bosphorus CLO II Designated Activity CompanyDocumento18 páginasBosphorus CLO II Designated Activity Companyeimg20041333Ainda não há avaliações

- SYBFM Equity Market II Session I Ver 1.2Documento84 páginasSYBFM Equity Market II Session I Ver 1.211SujeetAinda não há avaliações

- No-Armageddon Measure For Arbitrage-Free Pricing of Index Options in A Credit CrisisDocumento21 páginasNo-Armageddon Measure For Arbitrage-Free Pricing of Index Options in A Credit CrisisSapiensAinda não há avaliações

- A User's Guide To SOFR: The Alternative Reference Rates Committee April 2019Documento21 páginasA User's Guide To SOFR: The Alternative Reference Rates Committee April 2019rajat.panda2672100% (1)

- Econ 138: Financial and Behavioral Economics: Noise-Trader Risk in Financial Markets February 8 & 13, 2017Documento35 páginasEcon 138: Financial and Behavioral Economics: Noise-Trader Risk in Financial Markets February 8 & 13, 2017econdocs0% (1)

- Libor Market Model Specification and CalibrationDocumento29 páginasLibor Market Model Specification and CalibrationGeorge LiuAinda não há avaliações

- CFA1 2019 Mock3 QuestionsDocumento44 páginasCFA1 2019 Mock3 QuestionsmajedmoghadamiAinda não há avaliações

- Structured Financial Product A Complete Guide - 2020 EditionNo EverandStructured Financial Product A Complete Guide - 2020 EditionAinda não há avaliações

- The+Student's+t DistributionDocumento7 páginasThe+Student's+t DistributionAmarnathMaitiAinda não há avaliações

- Durbin Watson TablesDocumento11 páginasDurbin Watson TablesgotiiiAinda não há avaliações

- Do You Have To Be Abnormal To Beat The MarketDocumento3 páginasDo You Have To Be Abnormal To Beat The MarketPeter UrbaniAinda não há avaliações

- Random Forest in Excel and VBADocumento24 páginasRandom Forest in Excel and VBAPeter UrbaniAinda não há avaliações

- Cholesky Versus SVDDocumento4 páginasCholesky Versus SVDPeter UrbaniAinda não há avaliações

- Partial Correlation Network Graph VBA (DJINDI)Documento463 páginasPartial Correlation Network Graph VBA (DJINDI)Peter UrbaniAinda não há avaliações

- Opalesque New Managers May 2012Documento51 páginasOpalesque New Managers May 2012Peter Urbani0% (1)

- Opalesque NewManagers July 2012Documento45 páginasOpalesque NewManagers July 2012Peter UrbaniAinda não há avaliações

- Opalesque New Managers May 2012Documento51 páginasOpalesque New Managers May 2012Peter Urbani0% (1)

- Risk Perspectives: What Is Risk? Its Measurement, Dimensions, Modeling (Asset Classes, Risk Factors and Regimes)Documento11 páginasRisk Perspectives: What Is Risk? Its Measurement, Dimensions, Modeling (Asset Classes, Risk Factors and Regimes)Peter UrbaniAinda não há avaliações

- Opalesque New Managers March 2012Documento37 páginasOpalesque New Managers March 2012Peter UrbaniAinda não há avaliações

- How Well Does Your Hedge Fund HedgeDocumento2 páginasHow Well Does Your Hedge Fund HedgePeter UrbaniAinda não há avaliações

- Incremental and Marginal VaR Plus Infiniti 4 Moment Version No VBADocumento14 páginasIncremental and Marginal VaR Plus Infiniti 4 Moment Version No VBAPeter UrbaniAinda não há avaliações

- Four Moment Risk Decomposition No VBADocumento13 páginasFour Moment Risk Decomposition No VBAPeter UrbaniAinda não há avaliações

- Infiniti Capital Four Moment Risk DecompositionDocumento19 páginasInfiniti Capital Four Moment Risk DecompositionPeter UrbaniAinda não há avaliações

- Liqudity VaR With Correct Time Scaling of Higher MomentsDocumento113 páginasLiqudity VaR With Correct Time Scaling of Higher MomentsPeter UrbaniAinda não há avaliações

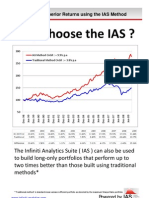

- Why Choose The IASDocumento6 páginasWhy Choose The IASPeter UrbaniAinda não há avaliações

- MODULE 2 Foundations of PhysicsDocumento7 páginasMODULE 2 Foundations of PhysicschloeAinda não há avaliações

- Math 8 System of Linear EquationDocumento17 páginasMath 8 System of Linear EquationMark Raniel Rimpillo PasalosdosAinda não há avaliações

- Pascal - OperatorsDocumento4 páginasPascal - OperatorsPaul MuasyaAinda não há avaliações

- Aberrations of TelescopeDocumento14 páginasAberrations of Telescopelighttec21Ainda não há avaliações

- CH 6 Sampling - and - EstimationDocumento15 páginasCH 6 Sampling - and - EstimationPoint BlankAinda não há avaliações

- Two PhaseDocumento29 páginasTwo Phaseafif arshadAinda não há avaliações

- Spectral DilationDocumento20 páginasSpectral DilationEsteban ZuluagaAinda não há avaliações

- Big Rip EssayDocumento2 páginasBig Rip EssayBo BobAinda não há avaliações

- 1.2 History and Scope of Fluid Mechanics: Chapter 1 IntroductionDocumento2 páginas1.2 History and Scope of Fluid Mechanics: Chapter 1 IntroductionFelipe Rocco EspinozaAinda não há avaliações

- Opman NotesDocumento10 páginasOpman NotesaegihyunAinda não há avaliações

- EEE 3201 Week 3Documento12 páginasEEE 3201 Week 3harun or rashidAinda não há avaliações

- CDC by Ajaysimha - VlsiDocumento14 páginasCDC by Ajaysimha - VlsiPriyanka GollapallyAinda não há avaliações

- Alkali Surfactant Polymer (ASP) Process For Shaley Formation With PyriteDocumento24 páginasAlkali Surfactant Polymer (ASP) Process For Shaley Formation With PyriteAlexandra Katerine LondoñoAinda não há avaliações

- Traction Versus Slip in A Wheel-Driven Belt Conveyor: Mechanism and Machine TheoryDocumento10 páginasTraction Versus Slip in A Wheel-Driven Belt Conveyor: Mechanism and Machine TheoryWashington MoraisAinda não há avaliações

- AP Statistics Review 2013Documento79 páginasAP Statistics Review 2013Jonathan TranAinda não há avaliações

- 03 Conic SectionsDocumento49 páginas03 Conic SectionsmeheheheAinda não há avaliações

- Presentation of DataDocumento18 páginasPresentation of DataMohit AlamAinda não há avaliações

- Workshop 5 2D Axisymmetric Impact: Introduction To ANSYS Explicit STRDocumento20 páginasWorkshop 5 2D Axisymmetric Impact: Introduction To ANSYS Explicit STRCosmin ConduracheAinda não há avaliações

- Customer Satisfaction On Service Quality in Private Commercial Banking Sector in BangladeshDocumento11 páginasCustomer Satisfaction On Service Quality in Private Commercial Banking Sector in BangladeshUmar KhanAinda não há avaliações

- Modular - Gen Math11-Lesson 1.1 Functions As Mathematical Model of Real-Life Situations - BALLERAS, MDocumento12 páginasModular - Gen Math11-Lesson 1.1 Functions As Mathematical Model of Real-Life Situations - BALLERAS, MAyesha YusopAinda não há avaliações

- 11 W11NSE6220 - Fall 2023 - ZengDocumento43 páginas11 W11NSE6220 - Fall 2023 - Zengrahul101056Ainda não há avaliações

- An Efficient Detection of Fake Currency KNN MethodDocumento7 páginasAn Efficient Detection of Fake Currency KNN MethodSenadheera PiyanwadaAinda não há avaliações

- Micro CH-7 RevenueDocumento8 páginasMicro CH-7 RevenueLalitKukrejaAinda não há avaliações

- HubbleDocumento2 páginasHubbleAlam AhmedAinda não há avaliações