Você também pode gostar

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

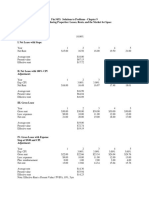

- Real Estate Chapter 9Documento5 páginasReal Estate Chapter 9febrythiodorAinda não há avaliações

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- CCIM Module 3 Study GuideDocumento8 páginasCCIM Module 3 Study GuideTony Simpson100% (1)

- Beechy 7ce v2 Ch18Documento89 páginasBeechy 7ce v2 Ch18منیر سادات0% (2)

- Net Lease Market Report 2018Documento3 páginasNet Lease Market Report 2018netleaseAinda não há avaliações

- Q1 2016 Net Lease Bank Ground Lease ReportDocumento3 páginasQ1 2016 Net Lease Bank Ground Lease ReportnetleaseAinda não há avaliações

- Cache Logistics Trust Prospectus (1 April 2010)Documento345 páginasCache Logistics Trust Prospectus (1 April 2010)Tan YanzhenAinda não há avaliações

- RE700 - Commercial Triple Net Lease (Single Tenant)Documento13 páginasRE700 - Commercial Triple Net Lease (Single Tenant)Malcolm ChristopherAinda não há avaliações

- Net Lease Tenant ProfilesDocumento82 páginasNet Lease Tenant ProfilesnetleaseAinda não há avaliações

- Net Lease Drug Store ReportDocumento4 páginasNet Lease Drug Store ReportnetleaseAinda não há avaliações

- Triple Net Lease Cap Rate ReportDocumento3 páginasTriple Net Lease Cap Rate ReportnetleaseAinda não há avaliações

- Net Lease Dollar Store Cap Rates 2018Documento3 páginasNet Lease Dollar Store Cap Rates 2018netleaseAinda não há avaliações

- The Net Lease QSR Market Report: Market Overview QSR (Corporate) Properties Median Asking Cap RatesDocumento3 páginasThe Net Lease QSR Market Report: Market Overview QSR (Corporate) Properties Median Asking Cap RatesnetleaseAinda não há avaliações

- Net Lease Medical Report - The Boulder GroupDocumento3 páginasNet Lease Medical Report - The Boulder GroupnetleaseAinda não há avaliações

- Net Lease Cricket WirelessDocumento14 páginasNet Lease Cricket WirelessnetleaseAinda não há avaliações

- 2017 Q3 Net Lease Drug Store Report - The Boulder GroupDocumento4 páginas2017 Q3 Net Lease Drug Store Report - The Boulder Groupnetlease100% (1)

- Best Buy Property For SaleDocumento15 páginasBest Buy Property For SalenetleaseAinda não há avaliações

- Chap 007Documento27 páginasChap 007Purushottam KumarAinda não há avaliações

- Net Lease Medical Report - The Boulder GroupDocumento3 páginasNet Lease Medical Report - The Boulder GroupnetleaseAinda não há avaliações

- Net Lease Research ReportDocumento3 páginasNet Lease Research ReportnetleaseAinda não há avaliações

- Commercial Real Estate For Beginners PDFDocumento92 páginasCommercial Real Estate For Beginners PDFmotaz_omar9651100% (3)

- Iqor Call Center: 6000 New Way, Klamath Falls, or 97601Documento9 páginasIqor Call Center: 6000 New Way, Klamath Falls, or 97601DANICA QUIOMAinda não há avaliações

- MKT 310 WK 11 Final Exam All Possible Questions 632666Documento247 páginasMKT 310 WK 11 Final Exam All Possible Questions 632666nataliewongjy3879Ainda não há avaliações

- Lecture 3 FIN 566Documento31 páginasLecture 3 FIN 566mf-shroomAinda não há avaliações

- ManagementDocumento8 páginasManagementAnish KumarAinda não há avaliações

- Ibig 04 08Documento45 páginasIbig 04 08Russell KimAinda não há avaliações

- LEXINGTONREALTY10KDocumento196 páginasLEXINGTONREALTY10Kmatthewphenry1951Ainda não há avaliações

- Triple Net Lease Research Report by The Boulder GroupDocumento2 páginasTriple Net Lease Research Report by The Boulder GroupnetleaseAinda não há avaliações

- 3rd Quarter Net Lease Market Research Report - The Boulder GroupDocumento3 páginas3rd Quarter Net Lease Market Research Report - The Boulder GroupnetleaseAinda não há avaliações

- Triple Net LeaseDocumento3 páginasTriple Net Leasearturo7942Ainda não há avaliações

- Notice of Removal, RK Associates, Anonymous Blogger South FloridaDocumento27 páginasNotice of Removal, RK Associates, Anonymous Blogger South FloridaLynnKWalshAinda não há avaliações

- 2 May 2023 INDIVIDUAL Investor PresentationDocumento22 páginas2 May 2023 INDIVIDUAL Investor PresentationAdetokunbo AdemolaAinda não há avaliações

- HW 7 Answer KeyDocumento2 páginasHW 7 Answer KeyhatanoloveAinda não há avaliações

- Building Economics Complete NotesDocumento20 páginasBuilding Economics Complete NotesManish MishraAinda não há avaliações

- Commercial Real Estate TerminologyDocumento7 páginasCommercial Real Estate TerminologyvjvijetaAinda não há avaliações

- Net Lease Bank Ground Lease Research ReportDocumento3 páginasNet Lease Bank Ground Lease Research ReportnetleaseAinda não há avaliações

- Net Lease Bank Ground Lease Report - The Boulder GroupDocumento3 páginasNet Lease Bank Ground Lease Report - The Boulder GroupnetleaseAinda não há avaliações

- Commercial LeaseDocumento33 páginasCommercial LeaseEmil Mitev100% (2)

- Module 4 LeaseDocumento34 páginasModule 4 LeaseJuhi JethaniAinda não há avaliações

- 2014 Q3 Net Lease Research ReportDocumento3 páginas2014 Q3 Net Lease Research ReportnetleaseAinda não há avaliações