Você também pode gostar

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (890)

- Tap Yourself FreeDocumento134 páginasTap Yourself Freenguyenhavn100% (2)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- ABB 3HAC050988 AM Arc and Arc Sensor RW 6-En PDFDocumento238 páginasABB 3HAC050988 AM Arc and Arc Sensor RW 6-En PDForefat1Ainda não há avaliações

- Adeptus Evangelion 2.5 - Operations ManualDocumento262 páginasAdeptus Evangelion 2.5 - Operations ManualGhostwheel50% (2)

- Revised fire drill performance standardsDocumento47 páginasRevised fire drill performance standardsKartikeya GuptaAinda não há avaliações

- Cumulative List of Notices to MarinersDocumento2 páginasCumulative List of Notices to MarinersResian Garalde Bisco100% (2)

- Goat Milk Marketing Feasibility Study Report - Only For ReferenceDocumento40 páginasGoat Milk Marketing Feasibility Study Report - Only For ReferenceSurajSinghalAinda não há avaliações

- The Study of 220 KV Power Substation Equipment DetailsDocumento90 páginasThe Study of 220 KV Power Substation Equipment DetailsAman GauravAinda não há avaliações

- Chapter-8 Turbine and Governor TestingDocumento10 páginasChapter-8 Turbine and Governor Testingafru2000Ainda não há avaliações

- LIST Real Estate Contacts ListDocumento4 páginasLIST Real Estate Contacts ListChauhan Harshit100% (1)

- AOAC 2012.11 Vitamin DDocumento3 páginasAOAC 2012.11 Vitamin DPankaj BudhlakotiAinda não há avaliações

- Meet The Money 2011® Jan Freitag, STR: US Lodging Industry - What Lies Ahead?Documento28 páginasMeet The Money 2011® Jan Freitag, STR: US Lodging Industry - What Lies Ahead?JefferMangelsAinda não há avaliações

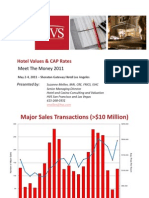

- Suzanne Mellen, HVS: Hotel Values and Cap RatesDocumento29 páginasSuzanne Mellen, HVS: Hotel Values and Cap RatesJefferMangelsAinda não há avaliações

- Daniel Lesser, U.S. Lodging Industry Analysis, September 2016Documento7 páginasDaniel Lesser, U.S. Lodging Industry Analysis, September 2016JefferMangelsAinda não há avaliações

- General Introduction To Assignment For Benefit of CreditorsDocumento9 páginasGeneral Introduction To Assignment For Benefit of CreditorsJefferMangelsAinda não há avaliações

- Art Adler, Jones Lang LaSalle Hotels: Global Capital MarketsDocumento17 páginasArt Adler, Jones Lang LaSalle Hotels: Global Capital MarketsJefferMangelsAinda não há avaliações

- Richard Green, USC Lusk Center: Economy and OutlookDocumento13 páginasRichard Green, USC Lusk Center: Economy and OutlookJefferMangelsAinda não há avaliações

- Commercial Finance Roundtable: A Creditor's Plan - A Way Out of The Morass of A Single Asset Real Estate Bankruptcy CaseDocumento2 páginasCommercial Finance Roundtable: A Creditor's Plan - A Way Out of The Morass of A Single Asset Real Estate Bankruptcy CaseJefferMangelsAinda não há avaliações

- Meet The Money® 2011: David Loeb, RW Baird: Trends in Hotel Capital MarketsDocumento28 páginasMeet The Money® 2011: David Loeb, RW Baird: Trends in Hotel Capital MarketsJefferMangelsAinda não há avaliações

- Suzanne Mellen, HVS: Hotel Value & CAP RatesDocumento29 páginasSuzanne Mellen, HVS: Hotel Value & CAP RatesJefferMangelsAinda não há avaliações

- U.S. Lodging Industry - Is There Light at The End of The Tunnel? by Greg Hartmann From Smith Travel Research AnalyticsDocumento66 páginasU.S. Lodging Industry - Is There Light at The End of The Tunnel? by Greg Hartmann From Smith Travel Research Analyticsal11823Ainda não há avaliações

- Benoit Gateau CuminDocumento11 páginasBenoit Gateau Cuminal11823Ainda não há avaliações

- Illuminating The Dark Side of The BankDocumento44 páginasIlluminating The Dark Side of The BankJefferMangelsAinda não há avaliações

- MTM Westergom PMDocumento13 páginasMTM Westergom PMJefferMangelsAinda não há avaliações

- U.S. Lodging Industry - Is There Light at The End of The Tunnel? by Greg Hartmann From Smith Travel Research AnalyticsDocumento66 páginasU.S. Lodging Industry - Is There Light at The End of The Tunnel? by Greg Hartmann From Smith Travel Research Analyticsal11823Ainda não há avaliações

- PKF Forecasts by Mark Woodworth, PKF Consulting at Meet The Money 2010Documento49 páginasPKF Forecasts by Mark Woodworth, PKF Consulting at Meet The Money 2010al11823Ainda não há avaliações

- Loeb Meet The Money Presentation 5-4-2010Documento35 páginasLoeb Meet The Money Presentation 5-4-2010JefferMangelsAinda não há avaliações

- Receiverships 101Documento41 páginasReceiverships 101JefferMangelsAinda não há avaliações

- Receivership 201Documento1 páginaReceivership 201JefferMangelsAinda não há avaliações

- Opportunity Buying 101 Purchasing Valuable Assets Before and After BankruptcyDocumento28 páginasOpportunity Buying 101 Purchasing Valuable Assets Before and After BankruptcyJefferMangelsAinda não há avaliações

- Financing Companies in Chap 11: How To Do It, How To Profit From ItDocumento18 páginasFinancing Companies in Chap 11: How To Do It, How To Profit From ItJefferMangelsAinda não há avaliações

- Loeb Meet The Money Presentation 5-4-2010Documento35 páginasLoeb Meet The Money Presentation 5-4-2010JefferMangelsAinda não há avaliações

- What To Send CounselDocumento1 páginaWhat To Send CounselJefferMangelsAinda não há avaliações

- RAR Property Sciences WebinarDocumento23 páginasRAR Property Sciences WebinarJefferMangelsAinda não há avaliações

- Receiverships 101Documento41 páginasReceiverships 101JefferMangelsAinda não há avaliações

- Receiverships 101Documento41 páginasReceiverships 101JefferMangelsAinda não há avaliações

- Financing Companies in Chap 11: How To Do It, How To Profit From ItDocumento18 páginasFinancing Companies in Chap 11: How To Do It, How To Profit From ItJefferMangelsAinda não há avaliações

- Special Assets "Tricks of The Trade": San Francisco OfficeDocumento14 páginasSpecial Assets "Tricks of The Trade": San Francisco OfficeJefferMangelsAinda não há avaliações

- Kendriya vidyalaya reading comprehension and grammar questionsDocumento7 páginasKendriya vidyalaya reading comprehension and grammar questionsRaam sivaAinda não há avaliações

- GE - Oil Sheen Detection, An Alternative To On-Line PPM AnalyzersDocumento2 páginasGE - Oil Sheen Detection, An Alternative To On-Line PPM AnalyzersjorgegppAinda não há avaliações

- 35.2 - ING - El Puente NewsletterDocumento13 páginas35.2 - ING - El Puente NewsletterIrmali FrancoAinda não há avaliações

- DGPS Sensor JLR-4331W Instruction ManualDocumento42 páginasDGPS Sensor JLR-4331W Instruction ManualantonioAinda não há avaliações

- Template EbcrDocumento7 páginasTemplate EbcrNoraAinda não há avaliações

- Datasheet Optris XI 410Documento2 páginasDatasheet Optris XI 410davidaldamaAinda não há avaliações

- BiologyDocumento21 páginasBiologyHrituraj banikAinda não há avaliações

- Gante Iris PPT Pe p006Documento20 páginasGante Iris PPT Pe p006Donna Ville GanteAinda não há avaliações

- 4 Ideal Models of Engine CyclesDocumento23 páginas4 Ideal Models of Engine CyclesSyedAinda não há avaliações

- BELL B40C - 872071-01 Section 2 EngineDocumento38 páginasBELL B40C - 872071-01 Section 2 EngineALI AKBAR100% (1)

- HS-2172 Vs HS-5500 Test ComparisonDocumento1 páginaHS-2172 Vs HS-5500 Test ComparisonRicardo VillarAinda não há avaliações

- Kingspan Spectrum™: Premium Organic Coating SystemDocumento4 páginasKingspan Spectrum™: Premium Organic Coating SystemNikolaAinda não há avaliações

- IruChem Co., Ltd-Introduction of CompanyDocumento62 páginasIruChem Co., Ltd-Introduction of CompanyKhongBietAinda não há avaliações

- MUCLecture 2021 10311889Documento11 páginasMUCLecture 2021 10311889Ramon Angelo MendezAinda não há avaliações

- 2nd Quarter Summative Test in MusicDocumento2 páginas2nd Quarter Summative Test in MusicIverAlambraAinda não há avaliações

- 9701 s12 QP 11 PDFDocumento16 páginas9701 s12 QP 11 PDFHubbak KhanAinda não há avaliações

- Applying Value Engineering to Improve Quality and Reduce Costs of Ready-Mixed ConcreteDocumento15 páginasApplying Value Engineering to Improve Quality and Reduce Costs of Ready-Mixed ConcreteayyishAinda não há avaliações

- Belden CatalogDocumento24 páginasBelden CatalogMani MaranAinda não há avaliações

- Frobenius Method for Solving Differential EquationsDocumento9 páginasFrobenius Method for Solving Differential EquationsMario PetričevićAinda não há avaliações

- Electrical Machines Multiple Choice Questions - Mcqs - QuizDocumento10 páginasElectrical Machines Multiple Choice Questions - Mcqs - Quiztooba mukhtarAinda não há avaliações