Você também pode gostar

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (120)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Indusrial Training Report. (Accounting)Documento71 páginasIndusrial Training Report. (Accounting)sen2000fc1095% (81)

- Twirl RegressionDocumento1 páginaTwirl RegressionceeshaaAinda não há avaliações

- FAQ2022MTECH2022Documento3 páginasFAQ2022MTECH2022ceeshaaAinda não há avaliações

- Ridge RegressionDocumento1 páginaRidge RegressionceeshaaAinda não há avaliações

- ABSF enDocumento22 páginasABSF enceeshaaAinda não há avaliações

- NovelDocumento1 páginaNovelceeshaaAinda não há avaliações

- Lasso RegressionDocumento1 páginaLasso RegressionceeshaaAinda não há avaliações

- بلی میں نے پالی ہےDocumento1 páginaبلی میں نے پالی ہےatiq khanAinda não há avaliações

- NovelDocumento1 páginaNovelceeshaaAinda não há avaliações

- PoemDocumento1 páginaPoemceeshaaAinda não há avaliações

- All Multiplication TableDocumento1 páginaAll Multiplication TableceeshaaAinda não há avaliações

- PoemDocumento1 páginaPoemceeshaaAinda não há avaliações

- My PoetryDocumento5 páginasMy PoetryceeshaaAinda não há avaliações

- All Tabs AdworksDocumento1 páginaAll Tabs AdworksceeshaaAinda não há avaliações

- Letter of CreditDocumento9 páginasLetter of CreditceeshaaAinda não há avaliações

- Day Wise ListDocumento6 páginasDay Wise ListceeshaaAinda não há avaliações

- Budget 2014/15Documento5 páginasBudget 2014/15ceeshaaAinda não há avaliações

- Table 1Documento1 páginaTable 1ceeshaaAinda não há avaliações

- Mocked Up Employee DataDocumento1 páginaMocked Up Employee DataceeshaaAinda não há avaliações

- Inserted New in AfterDocumento1 páginaInserted New in AfterceeshaaAinda não há avaliações

- Argentina Vs Germany BrazilDocumento2 páginasArgentina Vs Germany BrazilceeshaaAinda não há avaliações

- Movie ListDocumento8 páginasMovie ListceeshaaAinda não há avaliações

- My ProseDocumento5 páginasMy ProseceeshaaAinda não há avaliações

- Song ListDocumento8 páginasSong ListceeshaaAinda não há avaliações

- MonthlyDocumento3 páginasMonthlyceeshaaAinda não há avaliações

- My PoetryDocumento5 páginasMy PoetryceeshaaAinda não há avaliações

- Certificate Course in Financial Accounting (CDTP) : Duration: 6 MonthsDocumento1 páginaCertificate Course in Financial Accounting (CDTP) : Duration: 6 MonthsceeshaaAinda não há avaliações

- Save The Children: SubjectDocumento2 páginasSave The Children: SubjectAshraf AliAinda não há avaliações

- Naat Nisa Brochure 2023...Documento4 páginasNaat Nisa Brochure 2023...Queen CAinda não há avaliações

- Unity Terms of ServiceDocumento12 páginasUnity Terms of ServiceMahboobAinda não há avaliações

- General Terms and Conditions: 7. SAFIR PortalDocumento6 páginasGeneral Terms and Conditions: 7. SAFIR PortalIndra Jeet KushwahaAinda não há avaliações

- Chapter Five Accounting For Internal Control and Cash Internal ControlDocumento8 páginasChapter Five Accounting For Internal Control and Cash Internal ControlTIZITAW MASRESHAAinda não há avaliações

- Volante For SWIFTDocumento2 páginasVolante For SWIFTLuis YañezAinda não há avaliações

- FEMADocumento51 páginasFEMAChinmay Shirsat50% (2)

- Midterm Exam Government Accounting and Npo Dfcamclp Ay 2020 2021 For Online StudentsDocumento12 páginasMidterm Exam Government Accounting and Npo Dfcamclp Ay 2020 2021 For Online StudentsNate Dela Cruz100% (1)

- Life Insurance Policy WordingDocumento3 páginasLife Insurance Policy WordingAkmal HelmiAinda não há avaliações

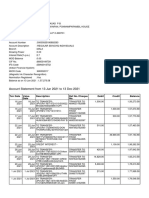

- Account Statement From 13 Jun 2021 To 13 Dec 2021Documento10 páginasAccount Statement From 13 Jun 2021 To 13 Dec 2021Syamprasad P BAinda não há avaliações

- Salary IncomeDocumento83 páginasSalary IncomechitkarashellyAinda não há avaliações

- The Negotiable Instruments (Amendment) Bill, 2018Documento2 páginasThe Negotiable Instruments (Amendment) Bill, 2018Jaskeerat Singh JoharAinda não há avaliações

- Working Capital MGTDocumento68 páginasWorking Capital MGTSidd MishraAinda não há avaliações

- Marisa IklanDocumento30 páginasMarisa IklanFadell FmAinda não há avaliações

- Romelo Online101 - 6 Digits - 2022 - EricDocumento15 páginasRomelo Online101 - 6 Digits - 2022 - EricFredrick GordonAinda não há avaliações

- 4 Cham V Paita-MoyaDocumento2 páginas4 Cham V Paita-MoyaNikita DaceraAinda não há avaliações

- Installment Promissory Note 1Documento1 páginaInstallment Promissory Note 1api-385482345Ainda não há avaliações

- Eservices Terms and Contitions enDocumento6 páginasEservices Terms and Contitions enMohammed Shams TabrezAinda não há avaliações

- Tibajia vs. CADocumento1 páginaTibajia vs. CARemelyn SeldaAinda não há avaliações

- Cash and Bank AccountsDocumento15 páginasCash and Bank AccountsFalola Feyisola Richard100% (1)

- 4 PDFDocumento4 páginas4 PDFsatish sharmaAinda não há avaliações

- G 1450Documento1 páginaG 1450Joel GuityAinda não há avaliações

- WebconnectDocumento1 páginaWebconnectThottempudi VyshnaviAinda não há avaliações

- Fee Structure For 2023 24 RenewalsDocumento2 páginasFee Structure For 2023 24 RenewalsshanmukhsagarAinda não há avaliações

- Nordea BankDocumento6 páginasNordea Bankeureka.net24Ainda não há avaliações

- PDFFile5b2780d4bf42a8 02107843Documento338 páginasPDFFile5b2780d4bf42a8 02107843Vinit MAinda não há avaliações

- Plumbing Invoice TemplateDocumento2 páginasPlumbing Invoice TemplateccadjuakkfojwaerccAinda não há avaliações

- Insta Loan On Card TCDocumento3 páginasInsta Loan On Card TCMANIKANDAN ANANTHARAJANAinda não há avaliações

- OblicasesDocumento38 páginasOblicasessakuraAinda não há avaliações