Você também pode gostar

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Ben Stein - Can Your Retirement SurviveDocumento8 páginasBen Stein - Can Your Retirement SurviveJulietaAinda não há avaliações

- In Gold We Trust July 2011Documento91 páginasIn Gold We Trust July 2011gjervisAinda não há avaliações

- Caveat VenditorDocumento6 páginasCaveat VenditorgjervisAinda não há avaliações

- SRLC Agm 2010Documento14 páginasSRLC Agm 2010gjervisAinda não há avaliações

- VAE CorporatePresentationDocumento21 páginasVAE CorporatePresentationgjervisAinda não há avaliações

- Sandstorm Metals & Energy LTD.: SND To Acquire Oil & Gas StreamsDocumento8 páginasSandstorm Metals & Energy LTD.: SND To Acquire Oil & Gas StreamsgjervisAinda não há avaliações

- Sandstorm Metals and Energy PresentationDocumento15 páginasSandstorm Metals and Energy PresentationgjervisAinda não há avaliações

- SSL - SND - Feb 23 - 2011Documento40 páginasSSL - SND - Feb 23 - 2011gjervisAinda não há avaliações

- May 2011 Corporate Presentation For Kiska MetalsDocumento27 páginasMay 2011 Corporate Presentation For Kiska MetalsgjervisAinda não há avaliações

- Doxa Energy April 2011 PresentationDocumento22 páginasDoxa Energy April 2011 PresentationgjervisAinda não há avaliações

- AsermacDocumento18 páginasAsermacgjervisAinda não há avaliações

- U.S. Geothermal Industry Overview 2011 01Documento44 páginasU.S. Geothermal Industry Overview 2011 01gjervisAinda não há avaliações

- 2011 Value Investing Congress NotesDocumento66 páginas2011 Value Investing Congress NotesgjervisAinda não há avaliações

- AAA Presentation Jan 2011Documento22 páginasAAA Presentation Jan 2011gjervisAinda não há avaliações

- AAA FactSheet Jan 2011Documento2 páginasAAA FactSheet Jan 2011gjervisAinda não há avaliações

- Empirical Parameterization of Setup, Swash, and RunupDocumento16 páginasEmpirical Parameterization of Setup, Swash, and RunupgjervisAinda não há avaliações

- IJREAMV05I0452086745Documento4 páginasIJREAMV05I0452086745yash wankhadeAinda não há avaliações

- Steelcast Limited: Website WW. Steel Cast NetDocumento5 páginasSteelcast Limited: Website WW. Steel Cast NetRahul PambharAinda não há avaliações

- Managerial Economics Financial Analysis June July 2022Documento8 páginasManagerial Economics Financial Analysis June July 2022Ashwik YadavAinda não há avaliações

- Here Are Some IdeasDocumento3 páginasHere Are Some IdeasBrahim OuhammouAinda não há avaliações

- CBSE Class 12 Accountancy Question Paper 2015 With SolutionsDocumento50 páginasCBSE Class 12 Accountancy Question Paper 2015 With SolutionsRavi AgrawalAinda não há avaliações

- Cash Chapter-DefinitionsDocumento44 páginasCash Chapter-DefinitionsJhonielyn Regalado RugaAinda não há avaliações

- Clean and Dirty PriceDocumento4 páginasClean and Dirty PriceAnkur GargAinda não há avaliações

- NOTESDocumento53 páginasNOTESirahQAinda não há avaliações

- GCG and ESG TheoryDocumento5 páginasGCG and ESG Theorypempi mlgAinda não há avaliações

- Global Money Dispatch: Credit Suisse EconomicsDocumento7 páginasGlobal Money Dispatch: Credit Suisse EconomicsRishrisAinda não há avaliações

- Leverage RatioDocumento4 páginasLeverage Ratiomanasapai12Ainda não há avaliações

- HiltonPlatt 11e TB Ch16Documento97 páginasHiltonPlatt 11e TB Ch16Jay HanAinda não há avaliações

- Impact On Rate of Household SavingsDocumento2 páginasImpact On Rate of Household SavingsKEVIN JUGOAinda não há avaliações

- Price B1 S2 2024 - DFDocumento30 páginasPrice B1 S2 2024 - DFYara AzizAinda não há avaliações

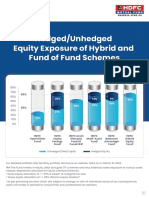

- Leaflet - Hedged and Unhedged Exposure of Hybrid FundsDocumento2 páginasLeaflet - Hedged and Unhedged Exposure of Hybrid FundsDeepakAinda não há avaliações

- Treasury and Capital Markets Interview PreparationDocumento5 páginasTreasury and Capital Markets Interview PreparationAbhishek BiswasAinda não há avaliações

- Multipurpose MallDocumento90 páginasMultipurpose MallkidanemariamAinda não há avaliações

- Ismr Full2019Documento206 páginasIsmr Full2019akpo-ebi johnAinda não há avaliações

- Mablethorpe Lincs Brochure MIPDocumento6 páginasMablethorpe Lincs Brochure MIPMark I'AnsonAinda não há avaliações

- FIN347 DraftDocumento11 páginasFIN347 DraftMUHAMMAD AIMANAinda não há avaliações

- Chapter 11: Arbitrage Pricing TheoryDocumento7 páginasChapter 11: Arbitrage Pricing TheorySilviu TrebuianAinda não há avaliações

- Manual OiDocumento30 páginasManual Oiudhaya kumarAinda não há avaliações

- CFO in Denver Colorado Resume Bruce PeeleDocumento2 páginasCFO in Denver Colorado Resume Bruce PeeleBruce PeeleAinda não há avaliações

- 2 ACC5215 2020 M11 Associates and JV All SlidesDocumento23 páginas2 ACC5215 2020 M11 Associates and JV All SlidesDev GargAinda não há avaliações

- METAPATH SOFTWARE AssignmentDocumento2 páginasMETAPATH SOFTWARE Assignmentsunil kumarAinda não há avaliações

- Accounting Top 50 QuestionsDocumento152 páginasAccounting Top 50 QuestionsDeep Mehta0% (1)

- Chapter 9: International Financial Statement AnalysisDocumento31 páginasChapter 9: International Financial Statement Analysisapi-241660930Ainda não há avaliações

- Relaxations & Amendments in Companies Act WebinarDocumento37 páginasRelaxations & Amendments in Companies Act WebinarAbhishek PareekAinda não há avaliações