Você também pode gostar

- Chap 6Documento110 páginasChap 6Mukesh Ek Talash100% (1)

- Promissory NoteDocumento1 páginaPromissory Noteapi-300362811Ainda não há avaliações

- Donavan 061914 - Notification of Reservation of Rights Recording County Public 26Documento3 páginasDonavan 061914 - Notification of Reservation of Rights Recording County Public 2614LEARNINGAinda não há avaliações

- Letter of RevocationDocumento1 páginaLetter of Revocationcashman966100% (1)

- Bill of ExchangeDocumento9 páginasBill of ExchangeMariyam MalsaAinda não há avaliações

- Depository AssignmentDocumento11 páginasDepository AssignmentDinesh GodhaniAinda não há avaliações

- Notice For AssignmentDocumento3 páginasNotice For AssignmentZaeem KhanAinda não há avaliações

- Power of Attorney and Declaration of RepresentativeDocumento2 páginasPower of Attorney and Declaration of Representativepreston_402003Ainda não há avaliações

- Affidavit of TitleDocumento2 páginasAffidavit of TitleFindLegalFormsAinda não há avaliações

- Proof of Delivery COVER LETTERDocumento1 páginaProof of Delivery COVER LETTERBen Hill100% (1)

- Presentation ON: "Commercial Banking"Documento22 páginasPresentation ON: "Commercial Banking"dont_forgetme2004Ainda não há avaliações

- Assignment of Promissory NoteDocumento1 páginaAssignment of Promissory NoteChicagoCitizens EmpowermentGroupAinda não há avaliações

- Fixed Interest Rate."Documento6 páginasFixed Interest Rate."Michelle T100% (1)

- Sovereign King BeyDocumento2 páginasSovereign King BeySovereign_King_3095Ainda não há avaliações

- W-8BEN: Do NOT Use This Form IfDocumento1 páginaW-8BEN: Do NOT Use This Form IfdoyokaAinda não há avaliações

- Revocable Letter of Credit Can Be Revoked Without The Consent of TheDocumento3 páginasRevocable Letter of Credit Can Be Revoked Without The Consent of ThePankaj ThapaAinda não há avaliações

- Asset-Backed Commercial PaperDocumento4 páginasAsset-Backed Commercial PaperdescataAinda não há avaliações

- Mortgage Bond For VehicleDocumento4 páginasMortgage Bond For Vehicleapi-19745405Ainda não há avaliações

- Correct Application and InterpretationDocumento106 páginasCorrect Application and Interpretationbiodun o100% (1)

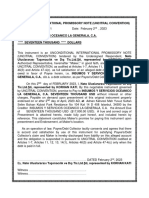

- Negotiable-International-Promissory-Note Nato Uluslararası Taşımacılık Ve Dış Tic - Ltd.Şti, Represented by KORHAN KATIDocumento1 páginaNegotiable-International-Promissory-Note Nato Uluslararası Taşımacılık Ve Dış Tic - Ltd.Şti, Represented by KORHAN KATItaoalvarado.everestAinda não há avaliações

- Bill of Sale: The John Smith Doe TrustDocumento1 páginaBill of Sale: The John Smith Doe TrustSim CookeAinda não há avaliações

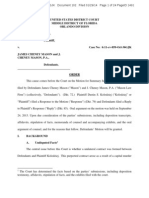

- Mason Summary JudgmentDocumento24 páginasMason Summary JudgmentEriq Gardner100% (1)

- Indemnity ClauseDocumento1 páginaIndemnity ClauseTerence LimAinda não há avaliações

- Trust DeedDocumento8 páginasTrust Deededdy_edwin23Ainda não há avaliações

- Creation Mandate in WLTDocumento10 páginasCreation Mandate in WLTsathishAinda não há avaliações

- Spousal Unity DoctrineDocumento2 páginasSpousal Unity DoctrineRESEARCHAinda não há avaliações

- Michael - 20160607 - 0001Documento6 páginasMichael - 20160607 - 0001PriyaSiranELAinda não há avaliações

- Demand DraftDocumento25 páginasDemand DraftDaksha PathakAinda não há avaliações

- T1 Checklist Establishment of A TrustDocumento4 páginasT1 Checklist Establishment of A TrustRod NewmanAinda não há avaliações

- Buczek 20081130 Bonded Promissory Note HSBC & BESTBUYDocumento1 páginaBuczek 20081130 Bonded Promissory Note HSBC & BESTBUYBob HurtAinda não há avaliações

- Bondforfeiture Civil SuretyDocumento10 páginasBondforfeiture Civil Suretyrhouse_1100% (1)

- US Internal Revenue Service: Irb04-43Documento27 páginasUS Internal Revenue Service: Irb04-43IRSAinda não há avaliações

- Suggested BylawsDocumento3 páginasSuggested Bylawsapi-343088725Ainda não há avaliações

- Sav1455 PDFDocumento6 páginasSav1455 PDFTed100% (1)

- General Durable Power of Attorney Effective Upon ExecutionDocumento5 páginasGeneral Durable Power of Attorney Effective Upon Executionsable1234Ainda não há avaliações

- Charge BackDocumento1 páginaCharge BackEyeAmAinda não há avaliações

- Custodial Power of AttorneyDocumento2 páginasCustodial Power of AttorneyhsjesqAinda não há avaliações

- Promissory Note TemplateDocumento5 páginasPromissory Note TemplateJason AbanesAinda não há avaliações

- UNCITRAL Model For International PaymentsDocumento8 páginasUNCITRAL Model For International PaymentsroselinAinda não há avaliações

- DTCCDocumento10 páginasDTCCpoojasengar100% (1)

- 1 Law of Boris Zoom Meeting DescriptionsDocumento16 páginas1 Law of Boris Zoom Meeting Descriptionsddrazen11Ainda não há avaliações

- HHIADocumento3 páginasHHIAGarrett GroverAinda não há avaliações

- TSB 5018e Financial Institution Bond STD No 24 PDFDocumento12 páginasTSB 5018e Financial Institution Bond STD No 24 PDFpanasheAinda não há avaliações

- NGO, Trust PDFDocumento15 páginasNGO, Trust PDFmonaAinda não há avaliações

- Binalay, Jude Alexis DDocumento18 páginasBinalay, Jude Alexis DChloe OberlinAinda não há avaliações

- Debt InstrumentsDocumento5 páginasDebt InstrumentsŚáńtőśh MőkáśhíAinda não há avaliações

- Security Assignment of Contractual Rights - PLCDocumento98 páginasSecurity Assignment of Contractual Rights - PLCMari Ana100% (1)

- Power of Appointment.Documento1 páginaPower of Appointment.georaw9588Ainda não há avaliações

- Bradford Exchange Lien UccDocumento2 páginasBradford Exchange Lien Uccstephen williamsAinda não há avaliações

- Irs - 2553 FormDocumento4 páginasIrs - 2553 FormmeikaizenAinda não há avaliações

- Hold Harmless and Indemnity Agreement No Hid - 220221 - Hhia Non-Negotiable - Private Between The PartiesDocumento2 páginasHold Harmless and Indemnity Agreement No Hid - 220221 - Hhia Non-Negotiable - Private Between The Partiesliz knight100% (1)

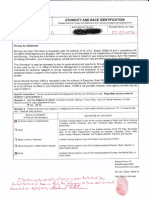

- Pcc-67te7368-C24 Finger and Palm Print FormDocumento2 páginasPcc-67te7368-C24 Finger and Palm Print FormAakash BarotAinda não há avaliações

- Fee Schedule PublicDocumento17 páginasFee Schedule PublicTori KleinAinda não há avaliações

- Cockerell V Title Ins Trust CoDocumento12 páginasCockerell V Title Ins Trust CoMortgage Compliance InvestigatorsAinda não há avaliações

- Negotiable Instruments ActDocumento30 páginasNegotiable Instruments ActRitik JainAinda não há avaliações

- Negotiable Instrument Act-1Documento56 páginasNegotiable Instrument Act-1Law LawyersAinda não há avaliações

- Common Law Trademark: KEVIN CARLTON GEORGE™ (1994 A.D.)Documento1 páginaCommon Law Trademark: KEVIN CARLTON GEORGE™ (1994 A.D.)Ambassador: Basadar: Qadar-Shar™, D.D. (h.c.) aka Kevin Carlton George™Ainda não há avaliações

- 1933 Royal Commission On Banking and Currency in Canada (Macmillan Commission)Documento119 páginas1933 Royal Commission On Banking and Currency in Canada (Macmillan Commission)Meliora Cogito100% (1)

- Arun Project FinalDocumento73 páginasArun Project FinalArun R NairAinda não há avaliações

- Banking InformationDocumento14 páginasBanking InformationIshaan KamalAinda não há avaliações

- MECO 121-Principles of Macroeconomics-Daud A DardDocumento5 páginasMECO 121-Principles of Macroeconomics-Daud A DardHaris AliAinda não há avaliações

- Mrs Fields CookiesDocumento12 páginasMrs Fields CookiesAditya Maheshwari100% (2)

- A Conference Interpreters View - Udo JorgDocumento14 páginasA Conference Interpreters View - Udo JorgElnur HuseynovAinda não há avaliações

- 4 Fleet Risk Assessment ProcessDocumento4 páginas4 Fleet Risk Assessment ProcessHaymanAHMEDAinda não há avaliações

- Naina Arvind MillsDocumento28 páginasNaina Arvind MillsMini Goel100% (1)

- Test of Significance - : 3-Standard Error of DifferenceDocumento4 páginasTest of Significance - : 3-Standard Error of Differenceavinash13071211Ainda não há avaliações

- Writing Stored Procedures For Microsoft SQL ServerDocumento334 páginasWriting Stored Procedures For Microsoft SQL Serverviust100% (4)

- HBO Jieliang Home PhoneDocumento6 páginasHBO Jieliang Home PhoneAshish BhalotiaAinda não há avaliações

- RAMPT Program PlanDocumento39 páginasRAMPT Program PlanganeshdhageAinda não há avaliações

- Classified Data AnalysisDocumento6 páginasClassified Data Analysiskaran976Ainda não há avaliações

- Four Fold TestDocumento19 páginasFour Fold TestNeil John CallanganAinda não há avaliações

- Cason Company Profile Eng 2011Documento11 páginasCason Company Profile Eng 2011Mercedesz TrumAinda não há avaliações

- GPP in IndonesiaDocumento5 páginasGPP in IndonesiaAconk FirmansyahAinda não há avaliações

- The Effectiveness of Product Placement in Video GamesDocumento91 páginasThe Effectiveness of Product Placement in Video GamesSbl Cakiroglu100% (1)

- General InformationDocumento5 páginasGeneral InformationPawan KumarAinda não há avaliações

- Case Problem The Hands On CEO of JetblueDocumento3 páginasCase Problem The Hands On CEO of JetblueMarinelEscotoCorderoAinda não há avaliações

- OpenText Business Center Capture For SAP Solutions 16.3 - Customization Guide English (CPBC160300-CGD-EN-01) PDFDocumento278 páginasOpenText Business Center Capture For SAP Solutions 16.3 - Customization Guide English (CPBC160300-CGD-EN-01) PDFAshish Yadav100% (2)

- 2 AILS StudyDocumento48 páginas2 AILS StudyRashid Nisar DarogeAinda não há avaliações

- Business Management Ethics 1Documento29 páginasBusiness Management Ethics 1Christy Malabanan100% (1)

- G.R. No. L-28329Documento6 páginasG.R. No. L-28329JoJOAinda não há avaliações

- Capital One's Letter To The Federal ReserveDocumento15 páginasCapital One's Letter To The Federal ReserveDealBookAinda não há avaliações

- Hire Purchase and LeasingDocumento30 páginasHire Purchase and LeasingShreyas Khanore100% (1)

- Property Surveyor CVDocumento2 páginasProperty Surveyor CVMike KelleyAinda não há avaliações

- PESTLE Analysis of IndiaDocumento19 páginasPESTLE Analysis of IndiaAbhishek7705100% (1)

- Sample Company Presentation PDFDocumento25 páginasSample Company Presentation PDFSachin DaharwalAinda não há avaliações

- ACC221 Quiz1Documento10 páginasACC221 Quiz1milkyode9Ainda não há avaliações

- Understanding and Applying Innovation Strategies in The Public SectorDocumento21 páginasUnderstanding and Applying Innovation Strategies in The Public SectorEda Paje AdornadoAinda não há avaliações

- AuditingDocumento51 páginasAuditingGolamSarwarAinda não há avaliações