Você também pode gostar

- Computerised Payroll Practice Set Using MYOB AccountRight: Australian EditionNo EverandComputerised Payroll Practice Set Using MYOB AccountRight: Australian EditionAinda não há avaliações

- Payroll ProcessDocumento16 páginasPayroll Processgeorgebabyc100% (1)

- Payroll ManagementDocumento6 páginasPayroll ManagementNisha_Yadav_6277Ainda não há avaliações

- Payroll PreparationDocumento34 páginasPayroll PreparationShubha DevAinda não há avaliações

- Payroll ProceduresDocumento15 páginasPayroll ProceduresPaksmiler50% (2)

- Sap HR Payroll: - AghuDocumento73 páginasSap HR Payroll: - Aghussvallabhaneni100% (1)

- Payroll Methods R12Documento111 páginasPayroll Methods R12naga100% (1)

- RTMDH Multi Purpose Cooperative: Amt. Due For Overtime Holiday The Period Trans. Exp. 100% DeductionDocumento10 páginasRTMDH Multi Purpose Cooperative: Amt. Due For Overtime Holiday The Period Trans. Exp. 100% DeductionREMA PALCORINAinda não há avaliações

- Flow Chart (Accounts Payable Clerk)Documento2 páginasFlow Chart (Accounts Payable Clerk)cristynvilAinda não há avaliações

- Payroll CycleDocumento43 páginasPayroll CycleKylie TarnateAinda não há avaliações

- Payroll Procedures and ControlDocumento75 páginasPayroll Procedures and Controlalabotshubhang100% (1)

- Payroll AccountingDocumento7 páginasPayroll Accountingmobinil1Ainda não há avaliações

- PayrollDocumento49 páginasPayrollnikhil_jbpAinda não há avaliações

- Payroll Study SheetsDocumento2 páginasPayroll Study SheetsNatalie DeLazzari VerberkAinda não há avaliações

- New York University: Payroll AssessmentDocumento39 páginasNew York University: Payroll AssessmentTony MorganAinda não há avaliações

- Payroll Summary Report PDF TemplateDocumento12 páginasPayroll Summary Report PDF TemplateSyaiful Bahri0% (4)

- PAYROLLDocumento6 páginasPAYROLLDinesh Kumar GuptaAinda não há avaliações

- Payroll DeductionsDocumento63 páginasPayroll Deductionsishu1707Ainda não há avaliações

- Payroll CycleDocumento31 páginasPayroll Cyclehiwatari_sasukeAinda não há avaliações

- Chart of Accounts With DescriptionsDocumento8 páginasChart of Accounts With DescriptionsKhan Mohammad100% (2)

- CVIOG Payroll Internal ControlsDocumento34 páginasCVIOG Payroll Internal ControlsTony MorganAinda não há avaliações

- PayrollDocumento73 páginasPayrollKamran KhanAinda não há avaliações

- General Payroll, Employment and DeductionsDocumento6 páginasGeneral Payroll, Employment and DeductionsJosh LeBlancAinda não há avaliações

- PayrollDocumento10 páginasPayrollRodlyn LajonAinda não há avaliações

- Payroll Process Oracle HrmsDocumento44 páginasPayroll Process Oracle HrmsSAM ANUAinda não há avaliações

- 1 Payroll-SopDocumento12 páginas1 Payroll-SopbhanupalavarapuAinda não há avaliações

- HRMS Payroll Processing Management GuideDocumento228 páginasHRMS Payroll Processing Management GuideKandooz Al KandoozAinda não há avaliações

- Payroll DocumentDocumento23 páginasPayroll Documentkarthiksainath100% (3)

- ADP Payroll Detail Manual v4 PDFDocumento21 páginasADP Payroll Detail Manual v4 PDFchakripsAinda não há avaliações

- Payroll Summary ReportDocumento2 páginasPayroll Summary ReportAbril Jordan CasinilloAinda não há avaliações

- Payroll: Policy and ProceduresDocumento5 páginasPayroll: Policy and ProceduresHer Huw100% (1)

- Tax Preparer Notes PDFDocumento2 páginasTax Preparer Notes PDFJenny Williams0% (1)

- Payroll Specialist in Denver CO Resume Robert CenknerDocumento2 páginasPayroll Specialist in Denver CO Resume Robert CenknerRobertCenknerAinda não há avaliações

- Payroll: Company Financial Salaries Wages DeductionsDocumento5 páginasPayroll: Company Financial Salaries Wages DeductionsKavitaAinda não há avaliações

- Module - Payroll CycleDocumento3 páginasModule - Payroll CycleGANNLAUREN SIMANGANAinda não há avaliações

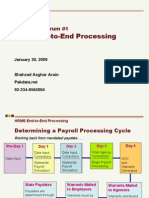

- Processing PayrollDocumento13 páginasProcessing PayrollShahzad Asghar ArainAinda não há avaliações

- PCL Chap 1 en CaDocumento42 páginasPCL Chap 1 en CaLaura100% (1)

- EXPENDITURE CYCLE: Payroll Process: (Third Party)Documento2 páginasEXPENDITURE CYCLE: Payroll Process: (Third Party)Sheila Mae AramanAinda não há avaliações

- HR Payroll US PracticeDocumento37 páginasHR Payroll US PracticeHau LeAinda não há avaliações

- SAP Payroll Canada: Payroll InfotypesDocumento4 páginasSAP Payroll Canada: Payroll Infotypeshellosri2001Ainda não há avaliações

- BSBFIM601 Human ResourcesDocumento19 páginasBSBFIM601 Human ResourcesHerawan Adif100% (2)

- Business Activity StatementDocumento5 páginasBusiness Activity StatementDhivya MadanAinda não há avaliações

- Employee Retention Credit For Employers Subject To Closure Due To COVID-19 CrisisDocumento6 páginasEmployee Retention Credit For Employers Subject To Closure Due To COVID-19 CrisisMoni ShafiqAinda não há avaliações

- PayrollDocumento73 páginasPayrollToqeer AhmedAinda não há avaliações

- Sap Payroll Taxes ScribdDocumento41 páginasSap Payroll Taxes ScribdChakrapani Dusetti100% (3)

- Bookkeeping Accounting Manager in Elkhart IN Resume Sally RodriguezDocumento2 páginasBookkeeping Accounting Manager in Elkhart IN Resume Sally RodriguezSallyRodriguezAinda não há avaliações

- ADP - APA CPP Study Group - CPPHandoutsDocumento238 páginasADP - APA CPP Study Group - CPPHandoutsJohn DavisAinda não há avaliações

- Accounting Excel Reports - Report Generalledger ExcelDocumento36 páginasAccounting Excel Reports - Report Generalledger ExcelMark Ceddrick MioleAinda não há avaliações

- 3 Payroll PresentationDocumento39 páginas3 Payroll PresentationFuad Abdul BaqiAinda não há avaliações

- Payroll Management: Presented By:-Shweta DhadkeDocumento16 páginasPayroll Management: Presented By:-Shweta Dhadkeshweta dhadkeAinda não há avaliações

- Finance Policies and Procedures Manual - TEMPLATEDocumento60 páginasFinance Policies and Procedures Manual - TEMPLATEHassan Liquat100% (2)

- CHAPTER 8 Business Activity Statements and Instalment Activity StatementsDocumento25 páginasCHAPTER 8 Business Activity Statements and Instalment Activity StatementsCJAinda não há avaliações

- GSTandAustralianTaxes PDFDocumento104 páginasGSTandAustralianTaxes PDFLefter Telos ZakaAinda não há avaliações

- FNSACC301 Learner Guide V1.1Documento187 páginasFNSACC301 Learner Guide V1.1Oyunsuvd Amgalan50% (2)

- Fixed Asset RegisterDocumento3 páginasFixed Asset Registerzuldvsb0% (1)

- 00 02 GST Advance - Info PDFDocumento118 páginas00 02 GST Advance - Info PDFKen ChiaAinda não há avaliações

- Payroll Taxes in U.SDocumento6 páginasPayroll Taxes in U.SLokesh ChittoraAinda não há avaliações

- Quickbooks Payroll Qs Section 3Documento7 páginasQuickbooks Payroll Qs Section 3Noorullah0% (1)

- Wage Type CharacteristicsDocumento29 páginasWage Type Characteristicsananth-jAinda não há avaliações

- PAYROLLDocumento32 páginasPAYROLLapi-19990211100% (1)

- Articles of IncorporationDocumento5 páginasArticles of IncorporationFranz Kafka100% (5)

- Share Application Doc MEGI AGRO PDFDocumento1 páginaShare Application Doc MEGI AGRO PDFcarthik19Ainda não há avaliações

- PB 113Documento45 páginasPB 113CLEAH MARYELL LLAMASAinda não há avaliações

- ACC 558 Lecture 5 IPSAS 23 ASSETSDocumento89 páginasACC 558 Lecture 5 IPSAS 23 ASSETSEzekiel Korankye OtooAinda não há avaliações

- Topic 2 Financial Information ProcessDocumento45 páginasTopic 2 Financial Information ProcessStunning AinAinda não há avaliações

- 5.2. Tax-Aggressiveness-In-Private-Family-Firms - An - 2014 - Journal-of-Family-Busine PDFDocumento11 páginas5.2. Tax-Aggressiveness-In-Private-Family-Firms - An - 2014 - Journal-of-Family-Busine PDFLiLyzLolaSLaluAinda não há avaliações

- Cost Reduction Techniques-FinalDocumento75 páginasCost Reduction Techniques-FinalSatishMatta70% (10)

- Famii KarooraDocumento9 páginasFamii KarooraIbsa MohammedAinda não há avaliações

- SUV Program BrochureDocumento4 páginasSUV Program BrochurerahuAinda não há avaliações

- Chapter 13 - Stockholder Rights and Corporate GovernanceDocumento19 páginasChapter 13 - Stockholder Rights and Corporate Governanceapi-328716222Ainda não há avaliações

- Frequently Asked Questions in ManagementDocumento230 páginasFrequently Asked Questions in ManagementsiddharthzalaAinda não há avaliações

- Answer of Integrative Case 1 (Track Software, LTD)Documento2 páginasAnswer of Integrative Case 1 (Track Software, LTD)Mrito Manob67% (3)

- Sap Fi /co Course Content in Ecc6 To Ehp 5Documento8 páginasSap Fi /co Course Content in Ecc6 To Ehp 5Mahesh JAinda não há avaliações

- Intelligent Business: Management in Mid-Sized German CompaniesDocumento8 páginasIntelligent Business: Management in Mid-Sized German Companiesrafael goesAinda não há avaliações

- Strategy, Organization Design and EffectivenessDocumento16 páginasStrategy, Organization Design and EffectivenessJaJ08Ainda não há avaliações

- Project Manager Business Analyst in ST Louis Resume Sharon DelPietroDocumento2 páginasProject Manager Business Analyst in ST Louis Resume Sharon DelPietroSharonDelPietroAinda não há avaliações

- Volkswagen Group LogisticsDocumento17 páginasVolkswagen Group LogisticsVIPUL TUTEJA100% (1)

- A Roadmap For A Digital TransformationDocumento11 páginasA Roadmap For A Digital TransformationrayestmAinda não há avaliações

- Fundamentals of Human Resource Management 6th Edition Noe Test BankDocumento26 páginasFundamentals of Human Resource Management 6th Edition Noe Test BankKatherineConneryaqk100% (53)

- Part 2 Basic Accounting Journalizing LectureDocumento11 páginasPart 2 Basic Accounting Journalizing LectureKong Aodian100% (2)

- 54R-07 - AACE InternationalDocumento17 páginas54R-07 - AACE InternationalFirasAlnaimiAinda não há avaliações

- Wipro Case StudyDocumento10 páginasWipro Case StudyNisha Bhagat0% (1)

- Louiscardin Brand PresentationDocumento48 páginasLouiscardin Brand PresentationdailaAinda não há avaliações

- Reaction Paper On MarxDocumento4 páginasReaction Paper On MarxRia LegaspiAinda não há avaliações

- The 6 Killerapps-NotesDocumento6 páginasThe 6 Killerapps-NotesKashifOfflineAinda não há avaliações

- Compilation of Raw Data - LBOBGDT Group 9Documento165 páginasCompilation of Raw Data - LBOBGDT Group 9Romm SamsonAinda não há avaliações

- Lesson 4 - The Steps in The Accounting CycleDocumento5 páginasLesson 4 - The Steps in The Accounting Cycleamora elyseAinda não há avaliações

- IO Model Vs Resource Based Model - Two Approaches To StrategyDocumento14 páginasIO Model Vs Resource Based Model - Two Approaches To StrategyM ManjunathAinda não há avaliações

- Job CircularDocumento28 páginasJob CircularTimeAinda não há avaliações

- Finance - Cost of Capital TheoryDocumento30 páginasFinance - Cost of Capital TheoryShafkat RezaAinda não há avaliações