Você também pode gostar

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Reynolds Public Health Proclamation - 2020.04.06Documento5 páginasReynolds Public Health Proclamation - 2020.04.06Shane Vander HartAinda não há avaliações

- USD TLGP MaturitiesDocumento1 páginaUSD TLGP MaturitiesCreditTraderAinda não há avaliações

- Fifth Circuit Decision Against FDA in Apter CaseDocumento24 páginasFifth Circuit Decision Against FDA in Apter CaseAssociation of American Physicians and Surgeons100% (1)

- IG Fundamentals Q22010Documento1 páginaIG Fundamentals Q22010CreditTraderAinda não há avaliações

- Weaponization Committee: HOW A "CYBERSECURITY" AGENCY COLLUDED WITH BIG TECH AND "DISINFORMATION" PARTNERS TO CENSOR AMERICANSDocumento37 páginasWeaponization Committee: HOW A "CYBERSECURITY" AGENCY COLLUDED WITH BIG TECH AND "DISINFORMATION" PARTNERS TO CENSOR AMERICANSJim Hoft100% (2)

- SPX Now and ThenDocumento1 páginaSPX Now and ThenCreditTraderAinda não há avaliações

- Credit ContractionDocumento1 páginaCredit ContractionCreditTraderAinda não há avaliações

- IG-HY Vs Stocks Relative-ValueDocumento1 páginaIG-HY Vs Stocks Relative-ValueCreditTraderAinda não há avaliações

- HY-IG Vs StocksDocumento1 páginaHY-IG Vs StocksCreditTraderAinda não há avaliações

- SPL 20101019Documento1 páginaSPL 20101019CreditTraderAinda não há avaliações

- HY Vs IG DurationDocumento1 páginaHY Vs IG DurationCreditTraderAinda não há avaliações

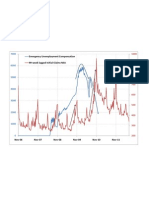

- EUC and 99-Week-Lagged Initial ClaimsDocumento1 páginaEUC and 99-Week-Lagged Initial ClaimsCreditTraderAinda não há avaliações

- CDR Csa 201007Documento1 páginaCDR Csa 201007CreditTraderAinda não há avaliações

- IG Over TSYDocumento1 páginaIG Over TSYCreditTraderAinda não há avaliações

- HY-IG Vs EquityDocumento1 páginaHY-IG Vs EquityCreditTraderAinda não há avaliações

- EUR Vs GDP-Weighted CDSDocumento1 páginaEUR Vs GDP-Weighted CDSCreditTraderAinda não há avaliações

- C&I Loans + ABCP - Aggregate CreditDocumento1 páginaC&I Loans + ABCP - Aggregate CreditCreditTraderAinda não há avaliações

- CDR Csa Aug2010Documento1 páginaCDR Csa Aug2010CreditTraderAinda não há avaliações

- CDR Csa Scatter Aug10Documento1 páginaCDR Csa Scatter Aug10CreditTraderAinda não há avaliações

- FSB30 IntrinsicsDocumento1 páginaFSB30 IntrinsicsCreditTraderAinda não há avaliações

- IG Range CompressionDocumento1 páginaIG Range CompressionCreditTraderAinda não há avaliações

- CDR Csa 20100813Documento1 páginaCDR Csa 20100813CreditTraderAinda não há avaliações

- IG Weekly RangeDocumento1 páginaIG Weekly RangeCreditTraderAinda não há avaliações

- Exchange Rate Regime Analysis For The Chinese YuanDocumento10 páginasExchange Rate Regime Analysis For The Chinese YuanCreditTraderAinda não há avaliações

- Spread Leverage ComparisonDocumento1 páginaSpread Leverage ComparisonCreditTraderAinda não há avaliações

- CDR Csa 20100716Documento1 páginaCDR Csa 20100716CreditTraderAinda não há avaliações

- IG Vs TSY CycleDocumento1 páginaIG Vs TSY CycleCreditTraderAinda não há avaliações

- JUN Roll by SectorDocumento1 páginaJUN Roll by SectorCreditTraderAinda não há avaliações

- Implied CorrelationDocumento1 páginaImplied CorrelationCreditTraderAinda não há avaliações

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- AC330 Class2 CascinoDocumento18 páginasAC330 Class2 Cascino2c_adminAinda não há avaliações

- Financial Planning of IndividualsDocumento70 páginasFinancial Planning of Individualstanvi100% (1)

- 15 The Functioning of Financial MarketsDocumento23 páginas15 The Functioning of Financial Marketsrajeshaisdu009Ainda não há avaliações

- Contrarian Investment ExtrapolationDocumento11 páginasContrarian Investment ExtrapolationB.C. MoonAinda não há avaliações

- Auto Trender PPT SMCDocumento14 páginasAuto Trender PPT SMCMithil Doshi100% (1)

- Fin 383 Final Cheat SheetDocumento1 páginaFin 383 Final Cheat SheetAnonymous ODAZn6VL6Ainda não há avaliações

- QUIZDocumento74 páginasQUIZmabelpal4783100% (2)

- English For Accounting A - Z Word List: Email - Wordlist Copy - QXD 4/4/07 3:40 PM Page 1Documento8 páginasEnglish For Accounting A - Z Word List: Email - Wordlist Copy - QXD 4/4/07 3:40 PM Page 1Do NguyenAinda não há avaliações

- Stopper v. Kestel, 4th Cir. (2001)Documento5 páginasStopper v. Kestel, 4th Cir. (2001)Scribd Government DocsAinda não há avaliações

- Finalchapter 21Documento9 páginasFinalchapter 21Jud Rossette ArcebesAinda não há avaliações

- Stock StrategiesDocumento29 páginasStock StrategiesHans CAinda não há avaliações

- The Upper Doab Sugar Mills LimitedDocumento96 páginasThe Upper Doab Sugar Mills LimitedAgam MittalAinda não há avaliações

- A Project Report: "Equity Analysis"Documento103 páginasA Project Report: "Equity Analysis"Sampath SanguAinda não há avaliações

- Kraft HeinzDocumento43 páginasKraft HeinzAnonymous 6f8RIS6Ainda não há avaliações

- Building A Holistic Capital Management FrameworkDocumento16 páginasBuilding A Holistic Capital Management FrameworkCognizantAinda não há avaliações

- Bain and CompanyDocumento10 páginasBain and CompanyRahul SinghAinda não há avaliações

- CURRENT PRICING OF IPOs: Is It Investor-Friendly?Documento53 páginasCURRENT PRICING OF IPOs: Is It Investor-Friendly?Sayam RoyAinda não há avaliações

- GHCL Limited - : 1 P - (FaxDocumento30 páginasGHCL Limited - : 1 P - (FaxShyam SunderAinda não há avaliações

- Accounting For PartnershipsDocumento58 páginasAccounting For PartnershipsAmy MurphyAinda não há avaliações

- CFA Tai Lieu On TapDocumento100 páginasCFA Tai Lieu On Tapkey4onAinda não há avaliações

- Interest Rate CollarDocumento3 páginasInterest Rate Collarinaam mahmoodAinda não há avaliações

- 2015 Narra Nickel Mining v. Redmont Consolidated MinesDocumento1 página2015 Narra Nickel Mining v. Redmont Consolidated MinesMarioneMaeThiamAinda não há avaliações

- Aimr - Investing Separately Alpha and Beta PDFDocumento102 páginasAimr - Investing Separately Alpha and Beta PDFAnonymous Mgq9dupCAinda não há avaliações

- Jpmorgan's 129 Page Internal Report On Whale Jan 16 2013Documento132 páginasJpmorgan's 129 Page Internal Report On Whale Jan 16 201383jjmackAinda não há avaliações

- Predicting Movement of Stock of Y Using Sutte IndicatorDocumento11 páginasPredicting Movement of Stock of Y Using Sutte Indicatoransari1621Ainda não há avaliações

- Financial InnovationDocumento19 páginasFinancial InnovationSiva ShankarAinda não há avaliações

- Statement of Cashflows SlidesDocumento48 páginasStatement of Cashflows SlidesAnita KhanAinda não há avaliações

- Dividend Decision ICICI by ImtiazaliDocumento26 páginasDividend Decision ICICI by ImtiazaliImtiyazMoverAinda não há avaliações

- Principles of Finance - 2101Documento14 páginasPrinciples of Finance - 2101Noel MartinAinda não há avaliações

- Threshold Heteroskedastic Models: Jean-Michel ZakoianDocumento25 páginasThreshold Heteroskedastic Models: Jean-Michel ZakoianLuis Bautista0% (1)