Você também pode gostar

- European Union: Statistical FactsheetDocumento22 páginasEuropean Union: Statistical FactsheetloginxscribdAinda não há avaliações

- Ευρωπαϊκή Επιτροπή - Εαρινές οικονομικές προβλέψεις 2020Documento216 páginasΕυρωπαϊκή Επιτροπή - Εαρινές οικονομικές προβλέψεις 2020Kappa NewsAinda não há avaliações

- Subscription Boxes 3Documento20 páginasSubscription Boxes 3assignmentexperts254Ainda não há avaliações

- 2013 EU IVD Market Statistics ReportDocumento21 páginas2013 EU IVD Market Statistics Reportanda_avAinda não há avaliações

- TourismDocumento6 páginasTourismad2iitAinda não há avaliações

- Boix-Privatizing The Public Business Sector in The Eighties-1997Documento25 páginasBoix-Privatizing The Public Business Sector in The Eighties-1997HermesAinda não há avaliações

- Economy of SwedenDocumento19 páginasEconomy of SwedenShailesh NairAinda não há avaliações

- DZT Incoming GTM11 WebDocumento24 páginasDZT Incoming GTM11 WebrusuemaAinda não há avaliações

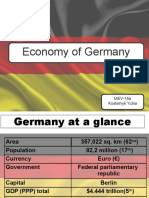

- Economy of Germany: MEV-18a Kostelnyk YuliiaDocumento21 páginasEconomy of Germany: MEV-18a Kostelnyk YuliiaЮлияAinda não há avaliações

- ImmigrationDocumento14 páginasImmigrationHareen JuniorAinda não há avaliações

- Datamonitor Life Insurance in FranceDocumento26 páginasDatamonitor Life Insurance in FranceMaimouna NdiayeAinda não há avaliações

- Agri Statistical Factsheet Eu enDocumento23 páginasAgri Statistical Factsheet Eu enJovanaAinda não há avaliações

- Datamonitor Insurance in FranceDocumento25 páginasDatamonitor Insurance in FranceMaimouna NdiayeAinda não há avaliações

- Anthony Hans HL Biology Ia Database WM PDFDocumento12 páginasAnthony Hans HL Biology Ia Database WM PDFYadhira IbañezAinda não há avaliações

- Anthony Hans HL Biology Ia Database WMDocumento12 páginasAnthony Hans HL Biology Ia Database WMEduardo Ricaldi ContrerasAinda não há avaliações

- Total Expenditure On Social Protection Per Head of Population. ECU/EUR (TPS00099)Documento8 páginasTotal Expenditure On Social Protection Per Head of Population. ECU/EUR (TPS00099)Hachi KamiAinda não há avaliações

- FranceDocumento12 páginasFranceMusfequr Rahman (191051015)Ainda não há avaliações

- Chapter 6 - An Overview of Market Struture Based Upon Existing SourcesDocumento15 páginasChapter 6 - An Overview of Market Struture Based Upon Existing Sourcesempower93 empower93Ainda não há avaliações

- Inversion de Los HogaresDocumento11 páginasInversion de Los HogaresgabrielaAinda não há avaliações

- Why mortality higher in developed nations for Covid-19Documento3 páginasWhy mortality higher in developed nations for Covid-19Luigie CorpuzAinda não há avaliações

- MH 7 2020 EN FinalDocumento42 páginasMH 7 2020 EN FinalUden RahmatAinda não há avaliações

- Italy Economy Report: GDP, Inflation, Monetary PolicyDocumento9 páginasItaly Economy Report: GDP, Inflation, Monetary PolicySHIVAKUMARAinda não há avaliações

- Ip136 enDocumento224 páginasIp136 ensaidAinda não há avaliações

- BRITISH Economy: By: Tra My - Thanh Thuy BDocumento28 páginasBRITISH Economy: By: Tra My - Thanh Thuy Banh tuAinda não há avaliações

- 12 Agritourism MarketsDocumento13 páginas12 Agritourism MarketsJepry PriyadiAinda não há avaliações

- Phpurt QKNDocumento7 páginasPhpurt QKNfred607Ainda não há avaliações

- China and EU Trading 2020Documento3 páginasChina and EU Trading 2020Dr. Murad AbelAinda não há avaliações

- GCI Analysis SwitzerlandDocumento35 páginasGCI Analysis Switzerlandsajal kumarAinda não há avaliações

- European Economic ForecastDocumento224 páginasEuropean Economic ForecastpxmtlAinda não há avaliações

- Croatia Packaging Sector 2014Documento80 páginasCroatia Packaging Sector 2014manojAinda não há avaliações

- PIGS Countries' New Challenges Under Europe 2020 Strategy: Danubius University of Galati, Faculty of EconomicsDocumento10 páginasPIGS Countries' New Challenges Under Europe 2020 Strategy: Danubius University of Galati, Faculty of EconomicsЕлизавета МиняйленкоAinda não há avaliações

- Sov Debt CrisisDocumento9 páginasSov Debt CrisisAzra Hanić SućeskaAinda não há avaliações

- Germany Country ProfileDocumento9 páginasGermany Country ProfilePut AllinsideAinda não há avaliações

- General Comparative Characteristic of The Economy of Belgium and The Netherlands - Agriculture.IndustryDocumento20 páginasGeneral Comparative Characteristic of The Economy of Belgium and The Netherlands - Agriculture.IndustryTotomir DumitruAinda não há avaliações

- The Pharmaceutical Industry in Figures 2021Documento28 páginasThe Pharmaceutical Industry in Figures 2021Smarthealthindia Healthcare TechAinda não há avaliações

- SWISS Directory 2013 PDFDocumento98 páginasSWISS Directory 2013 PDFmax100% (1)

- EU Direct Investment Positions, Flows and Income, Breakdown by Partner Countries (BPM6) (BOP - FDI6 - GEO)Documento7 páginasEU Direct Investment Positions, Flows and Income, Breakdown by Partner Countries (BPM6) (BOP - FDI6 - GEO)людмилаAinda não há avaliações

- ALGERIE CoucheDocumento99 páginasALGERIE CoucheDj@melAinda não há avaliações

- Incoming-Tourism Germany: Edition 2013Documento24 páginasIncoming-Tourism Germany: Edition 2013Aron ConstantinAinda não há avaliações

- Ethiopia: Ethiopia With World EU With EthiopiaDocumento2 páginasEthiopia: Ethiopia With World EU With EthiopiaTSEDEKEAinda não há avaliações

- Real GDP Per Capita EUDocumento9 páginasReal GDP Per Capita EUMiroslav ZutikovAinda não há avaliações

- Submitted By: Akash Aggarwal Ankit Gupta Ankur Talwar Submitted To: Prof. Alka MauryaDocumento31 páginasSubmitted By: Akash Aggarwal Ankit Gupta Ankur Talwar Submitted To: Prof. Alka MauryaAnkur TalwarAinda não há avaliações

- Economy of AustriaDocumento13 páginasEconomy of AustriaAman DecoraterAinda não há avaliações

- SERIEs (2016) - Vol 7 (3) - 341-357Documento7 páginasSERIEs (2016) - Vol 7 (3) - 341-357Oscar ClaveriaAinda não há avaliações

- Eurostat Key Figures On Europe 2012 PDFDocumento192 páginasEurostat Key Figures On Europe 2012 PDFionutandoAinda não há avaliações

- Document 2018 05 3 22427081 0 Prognoza PDFDocumento208 páginasDocument 2018 05 3 22427081 0 Prognoza PDFDan BAinda não há avaliações

- WEO DataDocumento1 páginaWEO Datacasarodriguez8621Ainda não há avaliações

- Cover: European Tourism: Trends & Prospects (Q1/2020) 1Documento54 páginasCover: European Tourism: Trends & Prospects (Q1/2020) 1RohitAinda não há avaliações

- Class Notes I 10-03Documento132 páginasClass Notes I 10-031991anuragAinda não há avaliações

- Spain Economy Seminar AssignmentDocumento7 páginasSpain Economy Seminar AssignmentFeham AliAinda não há avaliações

- Netherlands Country ProfileDocumento9 páginasNetherlands Country ProfilePut AllinsideAinda não há avaliações

- Cost Model - Country Analysis Report (CAR) For GermanyDocumento31 páginasCost Model - Country Analysis Report (CAR) For GermanyAcuacria DosAinda não há avaliações

- Final Market: Towards A New Hierarchy of Risks ?Documento19 páginasFinal Market: Towards A New Hierarchy of Risks ?Morningstar FranceAinda não há avaliações

- Romania: South AfricaDocumento33 páginasRomania: South AfricaDiacAinda não há avaliações

- Appendix A2: INCOME, ESS8 - 2016 Ed. 2.1Documento31 páginasAppendix A2: INCOME, ESS8 - 2016 Ed. 2.1Guillem RicoAinda não há avaliações

- Current Economic Indicators - Euro ZoneDocumento2 páginasCurrent Economic Indicators - Euro ZoneShiva DuttaAinda não há avaliações

- CNMVTrimestreI07 Een PDFDocumento273 páginasCNMVTrimestreI07 Een PDFsolajeroAinda não há avaliações

- OECD GDP Growth Slows to 0.7% in Q4 2020Documento2 páginasOECD GDP Growth Slows to 0.7% in Q4 2020Nina KondićAinda não há avaliações

- Germany Country Risk AnalysisDocumento22 páginasGermany Country Risk Analysisamitsharma_acdsAinda não há avaliações

- Country ReviewSwitzerland: A CountryWatch PublicationNo EverandCountry ReviewSwitzerland: A CountryWatch PublicationAinda não há avaliações

- DMI Review-What Is The Real Value of Design Jeneanne Rae Motiv Strategies-WEBDocumento8 páginasDMI Review-What Is The Real Value of Design Jeneanne Rae Motiv Strategies-WEBdabbaAinda não há avaliações

- Retail Book Chap07Documento17 páginasRetail Book Chap07Harman GillAinda não há avaliações

- Retail Wholesale LogisticsDocumento90 páginasRetail Wholesale LogisticsYandex PrithuAinda não há avaliações

- A Case Study of WalDocumento4 páginasA Case Study of Walshahi09Ainda não há avaliações

- Executive SummaryDocumento6 páginasExecutive SummaryRavindra PawarAinda não há avaliações

- Lidl SR Report 2017Documento68 páginasLidl SR Report 2017royalbakerytAinda não há avaliações

- Retail Institutions by Store-Based Strategy Mix: Retail Management: A Strategic ApproachDocumento34 páginasRetail Institutions by Store-Based Strategy Mix: Retail Management: A Strategic ApproachebustosfAinda não há avaliações

- Managing Retailing, Wholesaling, and LogisticsDocumento20 páginasManaging Retailing, Wholesaling, and LogisticsRozan FarizqyAinda não há avaliações

- WALMART CASE Group1 Finished Revised 3Documento50 páginasWALMART CASE Group1 Finished Revised 3Elnur MahmudovAinda não há avaliações

- Carrefour-Which Way To Go?: An Assignment inDocumento8 páginasCarrefour-Which Way To Go?: An Assignment inKelly maria RodriguesAinda não há avaliações

- Google's journey from start-up to global giantDocumento14 páginasGoogle's journey from start-up to global giantJawad KaramatAinda não há avaliações

- RETAIL MANAGEMENT UNIT 1 Part 1Documento14 páginasRETAIL MANAGEMENT UNIT 1 Part 1SrinathParshettyAinda não há avaliações

- Unit 9 Chapter 13 Retailing and Wholesaling Eng 04-04-2021Documento39 páginasUnit 9 Chapter 13 Retailing and Wholesaling Eng 04-04-2021Elias Macher CarpenaAinda não há avaliações

- Caso D! EMPEA-Institute - Impact-Case-Study - Koba - WEBDocumento2 páginasCaso D! EMPEA-Institute - Impact-Case-Study - Koba - WEBFranklin GrisalesAinda não há avaliações

- Aldi Case Study (IESE) PDFDocumento27 páginasAldi Case Study (IESE) PDFhrushiAinda não há avaliações

- Mba-Iii-Retail Management NotesDocumento84 páginasMba-Iii-Retail Management NotesRonit t.eAinda não há avaliações

- Supply ChainDocumento19 páginasSupply ChainmeseretAinda não há avaliações

- Simmons Foods Inc Prelim Offer 2017Documento194 páginasSimmons Foods Inc Prelim Offer 2017William O'ConnellAinda não há avaliações

- Walmart SWOT and PORTERS FIVE FORCE MODELDocumento7 páginasWalmart SWOT and PORTERS FIVE FORCE MODELsanelnair0% (1)

- Retailing Management 9th Edition Levy Weitz Professor 007802899X Solution ManualDocumento37 páginasRetailing Management 9th Edition Levy Weitz Professor 007802899X Solution Manualkathleen100% (25)

- Wal MartDocumento21 páginasWal MartSeptember Irish MaldonadoAinda não há avaliações

- SEMA Market Report 2020 PDFDocumento90 páginasSEMA Market Report 2020 PDFdjdazedAinda não há avaliações

- Sample Report Beauty Personal Care Baby CareDocumento20 páginasSample Report Beauty Personal Care Baby CareHuy PhamAinda não há avaliações

- Consulting Casebook 2019Documento135 páginasConsulting Casebook 2019Hari Chandana100% (1)

- Ross Supply Chain StudyDocumento22 páginasRoss Supply Chain StudyKaushik ReddyAinda não há avaliações

- Case Study: Examining Walmart’s International Market Entry Strategy and TacticsDocumento28 páginasCase Study: Examining Walmart’s International Market Entry Strategy and TacticsMohammed Ansarul HoqueAinda não há avaliações

- Business Level StrategyDocumento40 páginasBusiness Level Strategymudassir23100% (2)

- CPDocumento10 páginasCPalweenarAinda não há avaliações

- Wal-Mart Corporation vs. Target Corporation CSRDocumento10 páginasWal-Mart Corporation vs. Target Corporation CSRDanaObeidAinda não há avaliações

- 2016 Economics H2 JC2 Pioneer Junior CollegeDocumento14 páginas2016 Economics H2 JC2 Pioneer Junior CollegeSebastian ZhangAinda não há avaliações