Você também pode gostar

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- JPM Insurance PrimerDocumento104 páginasJPM Insurance Primerdamon_enola3313Ainda não há avaliações

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- FA Study Text 2019 PDFDocumento476 páginasFA Study Text 2019 PDFsmlingwa100% (1)

- Cute Exam Paper Set 4Documento12 páginasCute Exam Paper Set 4Raja PeriasamyAinda não há avaliações

- Force Majeure Clauses in ICC Rules 1559904833 PDFDocumento27 páginasForce Majeure Clauses in ICC Rules 1559904833 PDFReena TahirAinda não há avaliações

- Commonwealth Bank StatementDocumento5 páginasCommonwealth Bank Statementsattazee1992100% (1)

- Lecture Notes On Principles of Risk Mana PDFDocumento138 páginasLecture Notes On Principles of Risk Mana PDFsafiqulislamAinda não há avaliações

- Types of AuditingDocumento7 páginasTypes of AuditingGhulam Mustafa100% (1)

- A8 Chemical BankDocumento27 páginasA8 Chemical BankPriyank BavishiAinda não há avaliações

- Internship Report On KBLDocumento33 páginasInternship Report On KBLMurtaza Mari67% (9)

- Account Statement From 1 Jul 2018 To 22 Jun 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocumento2 páginasAccount Statement From 1 Jul 2018 To 22 Jun 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceRahumanAinda não há avaliações

- Professional LiabilityDocumento8 páginasProfessional LiabilitySrinivasa Madhusudhana100% (1)

- (88387899) Mptcv2form24Documento18 páginas(88387899) Mptcv2form24Rakhi Chordiya0% (1)

- COC - SUbcontract FormDocumento32 páginasCOC - SUbcontract Formsham2000Ainda não há avaliações

- Freddie Mac & Fannie Mae and MGIC Underwriting GuidelinesDocumento6 páginasFreddie Mac & Fannie Mae and MGIC Underwriting Guidelines83jjmackAinda não há avaliações

- Lavigne RoofDocumento7 páginasLavigne Roofusmanf87Ainda não há avaliações

- The Best Travel Insurance For 2017 - Top Ten ReviewsDocumento13 páginasThe Best Travel Insurance For 2017 - Top Ten ReviewsPiAinda não há avaliações

- Fullbook PP Il P 2018 CRCDocumento446 páginasFullbook PP Il P 2018 CRCप्रेम शिवाAinda não há avaliações

- Tata AIG General Insurance (1) - 1Documento11 páginasTata AIG General Insurance (1) - 1sanjay_swastikAinda não há avaliações

- Intern Report On Bank AsiaDocumento89 páginasIntern Report On Bank Asiaziko777Ainda não há avaliações

- Amsterdam Ghid Parcari P+RDocumento4 páginasAmsterdam Ghid Parcari P+RIrina MihaelaAinda não há avaliações

- Challenges Faced by Indian Banking IndustryDocumento5 páginasChallenges Faced by Indian Banking IndustryPooja Sakru100% (1)

- Insurance Law Notes: Concealment in Marine InsuranceDocumento3 páginasInsurance Law Notes: Concealment in Marine InsuranceJohn SanchezAinda não há avaliações

- Partnership (A)Documento5 páginasPartnership (A)Wing Yee Choy0% (1)

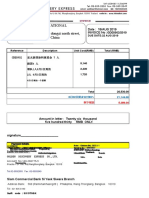

- Invoice - Seasky International Business Travel Gde0902Documento1 páginaInvoice - Seasky International Business Travel Gde0902Hank ZhouAinda não há avaliações

- Landmark Cases in The Law of Contract Order FormDocumento4 páginasLandmark Cases in The Law of Contract Order Formshahbaz_malbari_bballb13Ainda não há avaliações

- Real Estate and Construction Sector in The UAEDocumento20 páginasReal Estate and Construction Sector in The UAERoshan de SilvaAinda não há avaliações

- Rig Brochures Odfjell Drilling Rig Brochure SkjermvisningDocumento9 páginasRig Brochures Odfjell Drilling Rig Brochure SkjermvisningBima MahendraAinda não há avaliações

- Dissertation Report FormatDocumento53 páginasDissertation Report FormatSonal ThakurAinda não há avaliações

- Money Banking Generic Elective Third Sem. 5.5 PDFDocumento3 páginasMoney Banking Generic Elective Third Sem. 5.5 PDFAkistaaAinda não há avaliações