Você também pode gostar

- Food Outlook: Biannual Report on Global Food Markets: November 2022No EverandFood Outlook: Biannual Report on Global Food Markets: November 2022Ainda não há avaliações

- Manish 1Documento71 páginasManish 1Anurag RathiAinda não há avaliações

- Solar Powered Agro Industrial Project of Cassava Based Bioethanol Processing UnitNo EverandSolar Powered Agro Industrial Project of Cassava Based Bioethanol Processing UnitAinda não há avaliações

- Cold Storage Industry, Apmc MarketDocumento59 páginasCold Storage Industry, Apmc Marketdinkar13375100% (2)

- Energy Storage: Legal and Regulatory Challenges and OpportunitiesNo EverandEnergy Storage: Legal and Regulatory Challenges and OpportunitiesAinda não há avaliações

- Cold Chain Market-IndiaDocumento4 páginasCold Chain Market-IndiaRachna GuptaAinda não há avaliações

- The State of Food and Agriculture 2021: Making Agrifood Systems More Resilient to Shocks and StressesNo EverandThe State of Food and Agriculture 2021: Making Agrifood Systems More Resilient to Shocks and StressesAinda não há avaliações

- Cold Chain Industry in India A ReportDocumento5 páginasCold Chain Industry in India A ReportANKUSHSINGH2690Ainda não há avaliações

- Food Outlook: Biannual Report on Global Food Markets: June 2020No EverandFood Outlook: Biannual Report on Global Food Markets: June 2020Ainda não há avaliações

- Chapter 1: Introduction Topic of ResearchDocumento15 páginasChapter 1: Introduction Topic of ResearchYash DesaiAinda não há avaliações

- Achieving Zero Hunger: The Critical Role of Investments in Social Protection and Agriculture. Second EditionNo EverandAchieving Zero Hunger: The Critical Role of Investments in Social Protection and Agriculture. Second EditionAinda não há avaliações

- Cold Chain industryDocumento20 páginasCold Chain industryazconsulting.connectAinda não há avaliações

- Cold Chain Industry Analysis SummaryDocumento151 páginasCold Chain Industry Analysis SummaryAravind GanesanAinda não há avaliações

- C C C C C C C CCCCCCCCCCCCCCCCCCCCC CC: CCCCCCCCCCCCCDocumento15 páginasC C C C C C C CCCCCCCCCCCCCCCCCCCCC CC: CCCCCCCCCCCCCVelani GonsalvesAinda não há avaliações

- Cold Chain Logistics IntroductionDocumento26 páginasCold Chain Logistics IntroductionMahesh ChandraAinda não há avaliações

- Performance of Warehousing in KarnatakaDocumento51 páginasPerformance of Warehousing in Karnatakamalkanti007Ainda não há avaliações

- Insights on India's Cold Supply Chain ManagementDocumento7 páginasInsights on India's Cold Supply Chain ManagementAnonymous P1xUTHstHTAinda não há avaliações

- Comprehensive Cold Chain Industry OverviewDocumento90 páginasComprehensive Cold Chain Industry OverviewAmit RajAinda não há avaliações

- Cold Chain Grid in India: Developing an Integrated InfrastructureDocumento20 páginasCold Chain Grid in India: Developing an Integrated InfrastructureRonak RawatAinda não há avaliações

- 1.1 ObjectivesDocumento26 páginas1.1 ObjectivesRaj KumarAinda não há avaliações

- Research Methodology for Cold Storage Project ReportDocumento33 páginasResearch Methodology for Cold Storage Project ReportHarpreet Singh SainiAinda não há avaliações

- Cold StorageDocumento7 páginasCold StorageJaleel Ahmed GulammohiddinAinda não há avaliações

- The Regional & Global Trends Shaping AgribusinessDocumento37 páginasThe Regional & Global Trends Shaping AgribusinessSanjay SethiAinda não há avaliações

- CooLogistics - ChilikuriDocumento46 páginasCooLogistics - ChilikurirohitgjoshiAinda não há avaliações

- Food July07Documento1 páginaFood July07sanghvimananAinda não há avaliações

- DocumentDocumento52 páginasDocumentSunilkumar Sunil KumarAinda não há avaliações

- Cold Storage Facilities For Horticulture Products: Press Information Bureau Government of India Ministry of AgricultureDocumento2 páginasCold Storage Facilities For Horticulture Products: Press Information Bureau Government of India Ministry of AgricultureBadri SeetharamanAinda não há avaliações

- Emerging Opportunities-2013Documento9 páginasEmerging Opportunities-2013abhinav gaurAinda não há avaliações

- DPR Coldchain KiwiDocumento37 páginasDPR Coldchain KiwiYuvraj DuggalAinda não há avaliações

- Cold Storages Delhi NCRDocumento66 páginasCold Storages Delhi NCRaparchopra8302100% (1)

- Cold Storage Business Opportunities and Government Subsidies in 2021Documento6 páginasCold Storage Business Opportunities and Government Subsidies in 2021INF Consulting Services Private LimitedAinda não há avaliações

- Commodities Backed Finance Project ReportDocumento74 páginasCommodities Backed Finance Project Reportkamdica100% (2)

- ChallengeColdChain DevelopmentDocumento25 páginasChallengeColdChain DevelopmentAnurag KushwahaAinda não há avaliações

- Cold StorageDocumento31 páginasCold StorageHarpreet Singh SainiAinda não há avaliações

- COLD ROOM SERVICE (1)Documento6 páginasCOLD ROOM SERVICE (1)AbdulkaderAinda não há avaliações

- India's Growing Cold Chain MarketDocumento2 páginasIndia's Growing Cold Chain MarketShubham TiwaryAinda não há avaliações

- LogisticsDocumento45 páginasLogisticsnehadandAinda não há avaliações

- Model Bankable Project On Bulk Milk Cooling Units: National Bank For Agriculture and Rural DevelopmentDocumento15 páginasModel Bankable Project On Bulk Milk Cooling Units: National Bank For Agriculture and Rural Developmentsarvjeet_kaushalAinda não há avaliações

- Dawlance Refrigerator Company AnalysisDocumento23 páginasDawlance Refrigerator Company Analysisaftab100% (4)

- Indian Cold Chain Logistics Industry and Snowman LogisticsDocumento16 páginasIndian Cold Chain Logistics Industry and Snowman LogisticsSalman Mohammed ShirasAinda não há avaliações

- Oppurtunities in Agriculture SectorDocumento18 páginasOppurtunities in Agriculture SectorSurya SrivastavaAinda não há avaliações

- Arifeen 2012 Working PaperDocumento59 páginasArifeen 2012 Working Papershafqat8396Ainda não há avaliações

- Research On Agricultural ProduDocumento8 páginasResearch On Agricultural ProduJane DDAinda não há avaliações

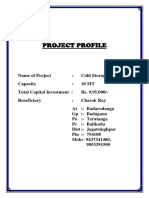

- Project Report On Cold StorageDocumento10 páginasProject Report On Cold StorageCHARAK RAY0% (1)

- Application of Information and Technology in Supply Chain Management of Fruits and Vegetables - A Brief OverviewDocumento7 páginasApplication of Information and Technology in Supply Chain Management of Fruits and Vegetables - A Brief OverviewInternational Journal of Innovative Science and Research TechnologyAinda não há avaliações

- An Assignment On "Cold Chain Management".: Submitted ToDocumento15 páginasAn Assignment On "Cold Chain Management".: Submitted ToSorathiya HiteshAinda não há avaliações

- Cold Storage Energy Efficientpractices - VYadavDocumento12 páginasCold Storage Energy Efficientpractices - VYadavEnergy ProfessionalsAinda não há avaliações

- Data Collection For CropDocumento12 páginasData Collection For CropNarendra ReddyAinda não há avaliações

- 12 Food ProcessingDocumento5 páginas12 Food ProcessingTanay BansalAinda não há avaliações

- COLD ROOM SERVICEDocumento5 páginasCOLD ROOM SERVICEAbdulkaderAinda não há avaliações

- Cold StoreDocumento22 páginasCold StoresajidaliyiAinda não há avaliações

- Cold Storage - Energy Efficient Practices - V YadavDocumento12 páginasCold Storage - Energy Efficient Practices - V Yadavm61367366Ainda não há avaliações

- Agri & Food Processing - IQF and Frozen Food Processing ProjectDocumento7 páginasAgri & Food Processing - IQF and Frozen Food Processing ProjectSunil K GuptaAinda não há avaliações

- Poultry Feed Profile PDFDocumento27 páginasPoultry Feed Profile PDFVivek Shah100% (1)

- Model Scheme On Bulk Milk Cooling CentersDocumento15 páginasModel Scheme On Bulk Milk Cooling Centersstalinkbc100% (2)

- Agro Sector Rough 1Documento4 páginasAgro Sector Rough 1Tonmoy Dash100% (1)

- Ass 3Documento3 páginasAss 3Nick's CreationAinda não há avaliações

- Food Processing IndustriesDocumento4 páginasFood Processing IndustriesJagan RathodAinda não há avaliações

- English Assignment FinalDocumento9 páginasEnglish Assignment FinalShubhojit ManikAinda não há avaliações

- Operations Management Project Report Based On Cold StoragesDocumento21 páginasOperations Management Project Report Based On Cold StoragesGaurav YadavAinda não há avaliações

- IB OutsourcingDocumento20 páginasIB OutsourcingMathangiAnanthanAinda não há avaliações

- Release 1 FDF40110 Certificate IV in Food ProcessingDocumento15 páginasRelease 1 FDF40110 Certificate IV in Food ProcessingMathangiAnanthanAinda não há avaliações

- Howard Seth ModelDocumento8 páginasHoward Seth ModelgsbarashidkhanAinda não há avaliações

- NestleDocumento104 páginasNestleIndu VikasiniAinda não há avaliações

- FilaDocumento27 páginasFilaAhmed BaigAinda não há avaliações

- 14.17 Al MuqasatDocumento5 páginas14.17 Al Muqasatamelia stephanie100% (1)

- Managers Checklist New Empl IntegrationDocumento3 páginasManagers Checklist New Empl IntegrationRajeshAinda não há avaliações

- Cia Part 3Documento6 páginasCia Part 3Nazir Ahmed100% (1)

- Maria Flordeliza L. Anastacio, Cpa Phd. Dbe: Vice President Centro Escolar University MalolosDocumento31 páginasMaria Flordeliza L. Anastacio, Cpa Phd. Dbe: Vice President Centro Escolar University MalolosCris VillarAinda não há avaliações

- Feel Free To Contact Us +88 016 80503030 +88 016 80503030 Sani - IsnineDocumento1 páginaFeel Free To Contact Us +88 016 80503030 +88 016 80503030 Sani - IsnineJahidur Rahman DipuAinda não há avaliações

- Cell No. 0928-823-5544/0967-019-3563 Cell No. 0928-823-5544/0967-019-3563 Cell No. 0928-823-5544/0967-019-3563Documento3 páginasCell No. 0928-823-5544/0967-019-3563 Cell No. 0928-823-5544/0967-019-3563 Cell No. 0928-823-5544/0967-019-3563WesternVisayas SDARMAinda não há avaliações

- 606 Assignment Naresh Quiz 3Documento3 páginas606 Assignment Naresh Quiz 3Naresh RaviAinda não há avaliações

- Company Profile Law Firm Getri, Fatahul & Co. English VersionDocumento9 páginasCompany Profile Law Firm Getri, Fatahul & Co. English VersionArip IDAinda não há avaliações

- Adani's Holistic Approach for India's FutureDocumento26 páginasAdani's Holistic Approach for India's FutureRow Arya'nAinda não há avaliações

- L2-Bus 204 PDFDocumento13 páginasL2-Bus 204 PDFBeka GideonAinda não há avaliações

- 10 - Chapter 2 - Background of Insurance IndustryDocumento29 páginas10 - Chapter 2 - Background of Insurance IndustryBounna PhoumalavongAinda não há avaliações

- An Assignment On Niche Marketing: Submitted ToDocumento3 páginasAn Assignment On Niche Marketing: Submitted ToGazi HasibAinda não há avaliações

- Vinci NewslettersDocumento1 páginaVinci Newsletterscommunity helps itselfAinda não há avaliações

- Your Energy Account: 1st June 2023 - 1st July 2023Documento3 páginasYour Energy Account: 1st June 2023 - 1st July 2023BAinda não há avaliações

- Computer in Community Pharmacy HDocumento13 páginasComputer in Community Pharmacy HMayan Khan100% (2)

- Integration The Growth Strategies of Hotel ChainsDocumento14 páginasIntegration The Growth Strategies of Hotel ChainsTatiana PosseAinda não há avaliações

- Marketing Practices by FMCG Companies For Rural Market: Institute of Business Management C.S.J.M University KanpurDocumento80 páginasMarketing Practices by FMCG Companies For Rural Market: Institute of Business Management C.S.J.M University KanpurDeepak YadavAinda não há avaliações

- Motivation QuizDocumento3 páginasMotivation QuizBEEHA afzelAinda não há avaliações

- Project of T.Y BbaDocumento49 páginasProject of T.Y BbaJeet Mehta0% (1)

- The Limitations of Mutual FundsDocumento1 páginaThe Limitations of Mutual FundsSaurabh BansalAinda não há avaliações

- 2.1 Chapter 2 - The Fundamental Concepts of AuditDocumento21 páginas2.1 Chapter 2 - The Fundamental Concepts of AuditĐức Qúach TrọngAinda não há avaliações

- Assigment 1 - POFDocumento1 páginaAssigment 1 - POFSAMRA MAIRAJAinda não há avaliações

- OneChicago Fact SheetDocumento1 páginaOneChicago Fact SheetJosh AlexanderAinda não há avaliações

- FILIPINAS COMPAÑIA DE SEGUROS vs. CHRISTERN, HUENEFELD and CO., INC.Documento2 páginasFILIPINAS COMPAÑIA DE SEGUROS vs. CHRISTERN, HUENEFELD and CO., INC.zacAinda não há avaliações

- Hidden Costof Quality AReviewDocumento21 páginasHidden Costof Quality AReviewmghili2002Ainda não há avaliações

- CAPSIM Tips on Sector Growth, Leverage, InventoryDocumento4 páginasCAPSIM Tips on Sector Growth, Leverage, InventoryTomi Chan100% (3)

- Chapter-16: Developing Pricing Strategies and ProgramsDocumento16 páginasChapter-16: Developing Pricing Strategies and ProgramsTaufiqul Hasan NihalAinda não há avaliações

- MIT's Mission: Supporting World-Class Education and Cutting-Edge ResearchDocumento11 páginasMIT's Mission: Supporting World-Class Education and Cutting-Edge ResearchDingo BingoAinda não há avaliações

- Job Ad DetailsDocumento12 páginasJob Ad DetailsYudhaAinda não há avaliações

- Mindset by Carol S. Dweck - Book Summary: The New Psychology of SuccessNo EverandMindset by Carol S. Dweck - Book Summary: The New Psychology of SuccessNota: 4.5 de 5 estrelas4.5/5 (327)

- Can't Hurt Me by David Goggins - Book Summary: Master Your Mind and Defy the OddsNo EverandCan't Hurt Me by David Goggins - Book Summary: Master Your Mind and Defy the OddsNota: 4.5 de 5 estrelas4.5/5 (382)

- Summary: Atomic Habits by James Clear: An Easy & Proven Way to Build Good Habits & Break Bad OnesNo EverandSummary: Atomic Habits by James Clear: An Easy & Proven Way to Build Good Habits & Break Bad OnesNota: 5 de 5 estrelas5/5 (1632)

- Make It Stick by Peter C. Brown, Henry L. Roediger III, Mark A. McDaniel - Book Summary: The Science of Successful LearningNo EverandMake It Stick by Peter C. Brown, Henry L. Roediger III, Mark A. McDaniel - Book Summary: The Science of Successful LearningNota: 4.5 de 5 estrelas4.5/5 (55)

- Summary of 12 Rules for Life: An Antidote to ChaosNo EverandSummary of 12 Rules for Life: An Antidote to ChaosNota: 4.5 de 5 estrelas4.5/5 (294)

- The Compound Effect by Darren Hardy - Book Summary: Jumpstart Your Income, Your Life, Your SuccessNo EverandThe Compound Effect by Darren Hardy - Book Summary: Jumpstart Your Income, Your Life, Your SuccessNota: 5 de 5 estrelas5/5 (456)

- The One Thing: The Surprisingly Simple Truth Behind Extraordinary ResultsNo EverandThe One Thing: The Surprisingly Simple Truth Behind Extraordinary ResultsNota: 4.5 de 5 estrelas4.5/5 (708)

- Summary of Slow Productivity by Cal Newport: The Lost Art of Accomplishment Without BurnoutNo EverandSummary of Slow Productivity by Cal Newport: The Lost Art of Accomplishment Without BurnoutNota: 1 de 5 estrelas1/5 (1)

- Summary of The Anxious Generation by Jonathan Haidt: How the Great Rewiring of Childhood Is Causing an Epidemic of Mental IllnessNo EverandSummary of The Anxious Generation by Jonathan Haidt: How the Great Rewiring of Childhood Is Causing an Epidemic of Mental IllnessAinda não há avaliações

- The Body Keeps the Score by Bessel Van der Kolk, M.D. - Book Summary: Brain, Mind, and Body in the Healing of TraumaNo EverandThe Body Keeps the Score by Bessel Van der Kolk, M.D. - Book Summary: Brain, Mind, and Body in the Healing of TraumaNota: 4.5 de 5 estrelas4.5/5 (266)

- How To Win Friends and Influence People by Dale Carnegie - Book SummaryNo EverandHow To Win Friends and Influence People by Dale Carnegie - Book SummaryNota: 5 de 5 estrelas5/5 (555)

- Essentialism by Greg McKeown - Book Summary: The Disciplined Pursuit of LessNo EverandEssentialism by Greg McKeown - Book Summary: The Disciplined Pursuit of LessNota: 4.5 de 5 estrelas4.5/5 (187)

- Summary of The Galveston Diet by Mary Claire Haver MD: The Doctor-Developed, Patient-Proven Plan to Burn Fat and Tame Your Hormonal SymptomsNo EverandSummary of The Galveston Diet by Mary Claire Haver MD: The Doctor-Developed, Patient-Proven Plan to Burn Fat and Tame Your Hormonal SymptomsAinda não há avaliações

- The War of Art by Steven Pressfield - Book Summary: Break Through The Blocks And Win Your Inner Creative BattlesNo EverandThe War of Art by Steven Pressfield - Book Summary: Break Through The Blocks And Win Your Inner Creative BattlesNota: 4.5 de 5 estrelas4.5/5 (273)

- SUMMARY: So Good They Can't Ignore You (UNOFFICIAL SUMMARY: Lesson from Cal Newport)No EverandSUMMARY: So Good They Can't Ignore You (UNOFFICIAL SUMMARY: Lesson from Cal Newport)Nota: 4.5 de 5 estrelas4.5/5 (14)

- The 5 Second Rule by Mel Robbins - Book Summary: Transform Your Life, Work, and Confidence with Everyday CourageNo EverandThe 5 Second Rule by Mel Robbins - Book Summary: Transform Your Life, Work, and Confidence with Everyday CourageNota: 4.5 de 5 estrelas4.5/5 (329)

- Summary of Supercommunicators by Charles Duhigg: How to Unlock the Secret Language of ConnectionNo EverandSummary of Supercommunicators by Charles Duhigg: How to Unlock the Secret Language of ConnectionAinda não há avaliações

- Steal Like an Artist by Austin Kleon - Book Summary: 10 Things Nobody Told You About Being CreativeNo EverandSteal Like an Artist by Austin Kleon - Book Summary: 10 Things Nobody Told You About Being CreativeNota: 4.5 de 5 estrelas4.5/5 (128)

- Book Summary of The Subtle Art of Not Giving a F*ck by Mark MansonNo EverandBook Summary of The Subtle Art of Not Giving a F*ck by Mark MansonNota: 4.5 de 5 estrelas4.5/5 (577)

- Designing Your Life by Bill Burnett, Dave Evans - Book Summary: How to Build a Well-Lived, Joyful LifeNo EverandDesigning Your Life by Bill Burnett, Dave Evans - Book Summary: How to Build a Well-Lived, Joyful LifeNota: 4.5 de 5 estrelas4.5/5 (61)

- Summary of Atomic Habits by James ClearNo EverandSummary of Atomic Habits by James ClearNota: 5 de 5 estrelas5/5 (168)

- We Were the Lucky Ones: by Georgia Hunter | Conversation StartersNo EverandWe Were the Lucky Ones: by Georgia Hunter | Conversation StartersAinda não há avaliações

- Summary of Bad Therapy by Abigail Shrier: Why the Kids Aren't Growing UpNo EverandSummary of Bad Therapy by Abigail Shrier: Why the Kids Aren't Growing UpNota: 5 de 5 estrelas5/5 (1)

- Blink by Malcolm Gladwell - Book Summary: The Power of Thinking Without ThinkingNo EverandBlink by Malcolm Gladwell - Book Summary: The Power of Thinking Without ThinkingNota: 4.5 de 5 estrelas4.5/5 (114)

- The Whole-Brain Child by Daniel J. Siegel, M.D., and Tina Payne Bryson, PhD. - Book Summary: 12 Revolutionary Strategies to Nurture Your Child’s Developing MindNo EverandThe Whole-Brain Child by Daniel J. Siegel, M.D., and Tina Payne Bryson, PhD. - Book Summary: 12 Revolutionary Strategies to Nurture Your Child’s Developing MindNota: 4.5 de 5 estrelas4.5/5 (57)

- Summary of Million Dollar Weekend by Noah Kagan and Tahl Raz: The Surprisingly Simple Way to Launch a 7-Figure Business in 48 HoursNo EverandSummary of Million Dollar Weekend by Noah Kagan and Tahl Raz: The Surprisingly Simple Way to Launch a 7-Figure Business in 48 HoursAinda não há avaliações

- Summary of It's Not You by Ramani Durvasula: Identifying and Healing from Narcissistic PeopleNo EverandSummary of It's Not You by Ramani Durvasula: Identifying and Healing from Narcissistic PeopleAinda não há avaliações

- Psycho-Cybernetics by Maxwell Maltz - Book SummaryNo EverandPsycho-Cybernetics by Maxwell Maltz - Book SummaryNota: 4.5 de 5 estrelas4.5/5 (91)