Você também pode gostar

- Pity The Billionaire The Hard-Times Swindle and The Unlikely Comeback of The RightDocumento13 páginasPity The Billionaire The Hard-Times Swindle and The Unlikely Comeback of The RightMacmillan Publishers89% (9)

- Citi Deal Pricing HistoryDocumento1 páginaCiti Deal Pricing HistoryykkwonAinda não há avaliações

- Transcript of Warren Buffett Interview With FCICDocumento23 páginasTranscript of Warren Buffett Interview With FCICSantangel's ReviewAinda não há avaliações

- Cocktail Investing: Distilling Everyday Noise into Clear Investment Signals for Better ReturnsNo EverandCocktail Investing: Distilling Everyday Noise into Clear Investment Signals for Better ReturnsAinda não há avaliações

- The Incredible Analysis of W D GannDocumento79 páginasThe Incredible Analysis of W D GannJohn Kent97% (31)

- THINK 143 Digital Magazine PDFDocumento53 páginasTHINK 143 Digital Magazine PDFmikemexico100% (9)

- .Es-WD Ganns Financial Time Table Extended and AdjustedDocumento3 páginas.Es-WD Ganns Financial Time Table Extended and Adjustedrforteza100% (2)

- America The Storyof Us Episode Bust Great Depression Video GuideDocumento4 páginasAmerica The Storyof Us Episode Bust Great Depression Video GuideJennifer Wright100% (1)

- Crisis Management Plan2Documento26 páginasCrisis Management Plan2mashangh100% (1)

- Williams, 2002 SolutionDocumento16 páginasWilliams, 2002 Solutionimtehan_chowdhury0% (3)

- Lesson 2: The Globalization of Worlds EconomicDocumento11 páginasLesson 2: The Globalization of Worlds Economiclindsay sevillaAinda não há avaliações

- Aviation Week & Space Technology - 29 December 2014Documento156 páginasAviation Week & Space Technology - 29 December 2014권혁록Ainda não há avaliações

- Residential Economic Issues & Trends ForumDocumento56 páginasResidential Economic Issues & Trends ForumNational Association of REALTORS®Ainda não há avaliações

- Calhoun County 2013-14 Economic ForecastDocumento56 páginasCalhoun County 2013-14 Economic ForecastBCEnquirerAinda não há avaliações

- Economic Analysis of British ColumbiaDocumento14 páginasEconomic Analysis of British ColumbiaCityNewsTorontoAinda não há avaliações

- September 2012 Housing Starts in British Columbia: For Immediate ReleaseDocumento5 páginasSeptember 2012 Housing Starts in British Columbia: For Immediate ReleasetflorkoAinda não há avaliações

- ULI - Senior Housing PresentationDocumento29 páginasULI - Senior Housing PresentationProMaturaAinda não há avaliações

- Onsumer Atch Anada: Canadian Housing Prices - Beware of The AverageDocumento4 páginasOnsumer Atch Anada: Canadian Housing Prices - Beware of The AverageSteve LadurantayeAinda não há avaliações

- Foote NENPA Fall ConferenceDocumento36 páginasFoote NENPA Fall Conferencenenpa10Ainda não há avaliações

- Home Economic Report Oct 21Documento2 páginasHome Economic Report Oct 21Adam WahedAinda não há avaliações

- Monthly Statistics Report August 2011Documento1 páginaMonthly Statistics Report August 2011Jim LeeAinda não há avaliações

- Economic Insight: Monthly Briefing From Icaew'S Economic Advisers MAY 2012Documento4 páginasEconomic Insight: Monthly Briefing From Icaew'S Economic Advisers MAY 2012api-125732404Ainda não há avaliações

- Series 13 Regional Growth Forecast: March 8, 2013Documento25 páginasSeries 13 Regional Growth Forecast: March 8, 2013api-63385278Ainda não há avaliações

- Economic and Housing Market OutlookDocumento56 páginasEconomic and Housing Market OutlookNational Association of REALTORS®Ainda não há avaliações

- Property Report MelbourneDocumento0 páginaProperty Report MelbourneMichael JordanAinda não há avaliações

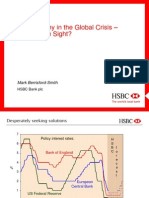

- HSCB Mark Berrisford Smith PresentationDocumento42 páginasHSCB Mark Berrisford Smith PresentationMikeNigawhatupAinda não há avaliações

- U.S. Lodging Market Outlook: Meet The Money 2012Documento38 páginasU.S. Lodging Market Outlook: Meet The Money 2012danilo_papaleoAinda não há avaliações

- China in Numbers: An Overview of China'S Key Economic IndicatorsDocumento11 páginasChina in Numbers: An Overview of China'S Key Economic IndicatorsmontannaroAinda não há avaliações

- TQHR 2011 Q3Documento65 páginasTQHR 2011 Q3Houston ChronicleAinda não há avaliações

- Are Indias Cities in A Housing BubbleDocumento9 páginasAre Indias Cities in A Housing BubbleAshwinBhandurgeAinda não há avaliações

- Kansas, Tax Reform, and Economic Growth: Louis R. Woodhill March 1, 2012Documento13 páginasKansas, Tax Reform, and Economic Growth: Louis R. Woodhill March 1, 2012api-34406941Ainda não há avaliações

- Census 2010 Power Point - KPDocumento42 páginasCensus 2010 Power Point - KPsomosnewyorkAinda não há avaliações

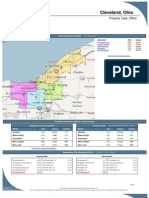

- Office MarketDocumento2 páginasOffice Marketjmrj76Ainda não há avaliações

- American Marketing Association - Jan 12, 2012Documento27 páginasAmerican Marketing Association - Jan 12, 2012roxanne_tsuiAinda não há avaliações

- Employment Tracker December 2011Documento2 páginasEmployment Tracker December 2011William HarrisAinda não há avaliações

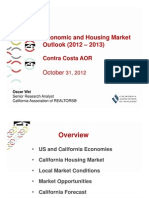

- 10-31-12 Contra Costa AORDocumento97 páginas10-31-12 Contra Costa AORjavthakAinda não há avaliações

- CREB Forecast 2011 Update (August Revision)Documento20 páginasCREB Forecast 2011 Update (August Revision)Mike FotiouAinda não há avaliações

- Anexo 5. C2 - Milton FriedmanDocumento5 páginasAnexo 5. C2 - Milton FriedmanEdison Osorio zuluagaAinda não há avaliações

- 2013-12-09 AmeriCatalyst What If It's Structural - Demographics & HousingDocumento16 páginas2013-12-09 AmeriCatalyst What If It's Structural - Demographics & HousingJoshua RosnerAinda não há avaliações

- Economic and Financial Market Outlook: Just When We Thought It Was SafeDocumento9 páginasEconomic and Financial Market Outlook: Just When We Thought It Was Safe8211210024Ainda não há avaliações

- CREB Market Update - September 2011Documento34 páginasCREB Market Update - September 2011Mike FotiouAinda não há avaliações

- Fed Snapshot Sep 2011Documento47 páginasFed Snapshot Sep 2011workitrichmondAinda não há avaliações

- BK Filing Trends KentuckyDocumento13 páginasBK Filing Trends KentuckyCourier JournalAinda não há avaliações

- Global Realestate TrendsDocumento8 páginasGlobal Realestate TrendscutmytaxesAinda não há avaliações

- Ukrainian Economy Anders As Lund 31008Documento42 páginasUkrainian Economy Anders As Lund 31008ankurbehlcoolAinda não há avaliações

- COMM350: Research ProposalDocumento3 páginasCOMM350: Research ProposalShayne RebelloAinda não há avaliações

- Hong Kong 2011 Economic OutlookDocumento11 páginasHong Kong 2011 Economic OutlookKwok TaiAinda não há avaliações

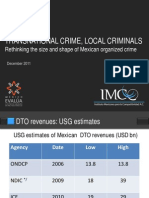

- Alejandro Hope 0Documento14 páginasAlejandro Hope 0S. M. Hasan ZidnyAinda não há avaliações

- Deloitte Corporate Finance Retail and Consumer Update q4 2011Documento8 páginasDeloitte Corporate Finance Retail and Consumer Update q4 2011KofikoduahAinda não há avaliações

- Today's Market : Houston-Baytown-Sugar Land Area Local Market Report, Third Quarter 2011Documento7 páginasToday's Market : Houston-Baytown-Sugar Land Area Local Market Report, Third Quarter 2011Kevin ReadAinda não há avaliações

- Canadian Economic Fact SheetDocumento2 páginasCanadian Economic Fact Sheethimubuet01Ainda não há avaliações

- Anexo 1 - C2 - Economista Adam SmithDocumento5 páginasAnexo 1 - C2 - Economista Adam SmithlinaAinda não há avaliações

- San Antonio Commercial Real Estate Market Overview: Ernest L. Brown IV, CCIMDocumento35 páginasSan Antonio Commercial Real Estate Market Overview: Ernest L. Brown IV, CCIMBusiness Bank of Texas, N.A.Ainda não há avaliações

- Economic and Housing Market Trends and OutlookDocumento37 páginasEconomic and Housing Market Trends and OutlookNational Association of REALTORS®Ainda não há avaliações

- Housing Snapshot - October 2011Documento11 páginasHousing Snapshot - October 2011economicdelusionAinda não há avaliações

- Middletown Profile Connecticut Economic Resource CenterDocumento2 páginasMiddletown Profile Connecticut Economic Resource CenterCassandra DayAinda não há avaliações

- Canada: Cap Rate ReportDocumento4 páginasCanada: Cap Rate ReportRobert DownAinda não há avaliações

- As Macro Revision Trade SterlingDocumento2 páginasAs Macro Revision Trade SterlingAnonymous fIL7OsuyAinda não há avaliações

- ScotiaBank AUG 04 Daily PointsDocumento2 páginasScotiaBank AUG 04 Daily PointsMiir ViirAinda não há avaliações

- Migration Review 2010-2011Documento7 páginasMigration Review 2010-2011IPPRAinda não há avaliações

- 2012 Economic and Housing Market OutlookDocumento38 páginas2012 Economic and Housing Market OutlooknarwebteamAinda não há avaliações

- HSBC - Vietnam Economic Outlook - Lam Phi YenDocumento32 páginasHSBC - Vietnam Economic Outlook - Lam Phi YenBet TranAinda não há avaliações

- Anexo 2 - C2 - Economista David RicardoDocumento5 páginasAnexo 2 - C2 - Economista David RicardolinaAinda não há avaliações

- Ingresos de Los CanadiensesDocumento3 páginasIngresos de Los CanadiensesZami Marquina CieloAinda não há avaliações

- SCV Econ Snapshot JUL2011Documento5 páginasSCV Econ Snapshot JUL2011jeff_wilsonAinda não há avaliações

- Manhattan Beach Real Estate Market Conditions - November 2015Documento15 páginasManhattan Beach Real Estate Market Conditions - November 2015Mother & Son South Bay Real Estate AgentsAinda não há avaliações

- Akeland Oy Hoir: To Track The Monthly Cash Flows For The Lakeland Boychoir For The YearDocumento14 páginasAkeland Oy Hoir: To Track The Monthly Cash Flows For The Lakeland Boychoir For The YearMohammed ZubairAinda não há avaliações

- Anexo 4. C2 - John KeynesDocumento5 páginasAnexo 4. C2 - John KeynesMaider Belen Duran SánchezAinda não há avaliações

- Anexo 2. C2 - David RicardoDocumento5 páginasAnexo 2. C2 - David RicardoMiguel PerdomoAinda não há avaliações

- Configuring the World: A Critical Political Economy ApproachNo EverandConfiguring the World: A Critical Political Economy ApproachAinda não há avaliações

- FloorplanDocumento1 páginaFloorplanDane KingsburyAinda não há avaliações

- VREB News Release - Victoria March 2014 Real Estate UpdateDocumento28 páginasVREB News Release - Victoria March 2014 Real Estate UpdateDane KingsburyAinda não há avaliações

- #315 - 600 Klahanie Floor PlanDocumento1 página#315 - 600 Klahanie Floor PlanDane KingsburyAinda não há avaliações

- Save Thousands - Buying Your First Home? RBC Royal Bank ® Can Help You Save Thousands!Documento2 páginasSave Thousands - Buying Your First Home? RBC Royal Bank ® Can Help You Save Thousands!Dane KingsburyAinda não há avaliações

- REBGV Stats Package October 2010Documento7 páginasREBGV Stats Package October 2010Mike StewartAinda não há avaliações

- December 2011 REBGV Stats Courtesy of Mike Stewart Vancouver RealtorDocumento7 páginasDecember 2011 REBGV Stats Courtesy of Mike Stewart Vancouver RealtorMike StewartAinda não há avaliações

- REBGV Statistics Package September 2010Documento7 páginasREBGV Statistics Package September 2010Mike StewartAinda não há avaliações

- Vancouver Real Estate Stats Package - August2010Documento7 páginasVancouver Real Estate Stats Package - August2010BenAmzalegAinda não há avaliações

- REBGV Stats Package - July2010Documento7 páginasREBGV Stats Package - July2010Mike StewartAinda não há avaliações

- REBGV Stats Package May 2010Documento7 páginasREBGV Stats Package May 2010Mike StewartAinda não há avaliações

- June 2010 Statistics From The Real Estate Board of Greater Vancouver Provided by Mike Stewart Vancouver RealtorDocumento7 páginasJune 2010 Statistics From The Real Estate Board of Greater Vancouver Provided by Mike Stewart Vancouver RealtorMike StewartAinda não há avaliações

- BudgetingDocumento7 páginasBudgetingCarl Angelo MontinolaAinda não há avaliações

- Current Account DeficitDocumento16 páginasCurrent Account Deficitjainudit212Ainda não há avaliações

- US Economic Status 2012Documento11 páginasUS Economic Status 2012RobertrslAinda não há avaliações

- Debt Crisis in GreeceDocumento9 páginasDebt Crisis in GreeceHải TrầnAinda não há avaliações

- Annual Samsung) 2008Documento106 páginasAnnual Samsung) 2008Pui Yi LeungAinda não há avaliações

- THE Independent ISSUE 502Documento44 páginasTHE Independent ISSUE 502The Independent MagazineAinda não há avaliações

- The Calvin Ball Bulletin: Welcome!Documento14 páginasThe Calvin Ball Bulletin: Welcome!Kimberly PruimAinda não há avaliações

- On The Brink - Inside The Race To Stop The Collapse of The Global Financial System by Henry PaulsonDocumento21 páginasOn The Brink - Inside The Race To Stop The Collapse of The Global Financial System by Henry PaulsonKitto IrvinAinda não há avaliações

- Analysis of Structural Regression in Method Approach Detecting The Economic Crisis of Selected CountriesDocumento11 páginasAnalysis of Structural Regression in Method Approach Detecting The Economic Crisis of Selected CountriesInternational Journal of Innovative Science and Research TechnologyAinda não há avaliações

- Sample Letters To Request SupportDocumento4 páginasSample Letters To Request SupportVineet DuhanAinda não há avaliações

- Chapters 1-5Documento174 páginasChapters 1-5Jovinal GonzalesAinda não há avaliações

- YJC 2008 Prelim - H2 P1 QN Paper and AnswersDocumento14 páginasYJC 2008 Prelim - H2 P1 QN Paper and AnswersBong Rei TanAinda não há avaliações

- The Foods and Beverages Merchants in Jabodetabek Lost Their Income Until RP 200 BillionDocumento2 páginasThe Foods and Beverages Merchants in Jabodetabek Lost Their Income Until RP 200 BillionAnna Uswatun.HAinda não há avaliações

- FT - 10 Years After Lehman - Weathering The Financial Crisis - How Seven Lives Were ChangedDocumento38 páginasFT - 10 Years After Lehman - Weathering The Financial Crisis - How Seven Lives Were ChangedelizabethrasskazovaAinda não há avaliações

- Beyond Crisis Management Practical Lifeline For Decision-Makers in The DarkDocumento23 páginasBeyond Crisis Management Practical Lifeline For Decision-Makers in The DarkcapsosAinda não há avaliações

- PeterFrase FourFutures-Introduction PDFDocumento20 páginasPeterFrase FourFutures-Introduction PDFGustavo Meyer100% (2)

- Rakindo KovaiDocumento1 páginaRakindo KovaiRagumuthukumar AlagarsamyAinda não há avaliações

- The Greek Crisis: Social Impact and Policy Responses: Manos MatsaganisDocumento40 páginasThe Greek Crisis: Social Impact and Policy Responses: Manos MatsaganisAnonymous 2TOWteL8JAinda não há avaliações