Você também pode gostar

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Cost Theory Word FileDocumento11 páginasCost Theory Word FileGaurav VaghasiyaAinda não há avaliações

- Sarthak Metals Ltd.Documento21 páginasSarthak Metals Ltd.saggttjsAinda não há avaliações

- New and Old Conceptual Framework, Accounting Principles, Accounting Process, PAS 18 - RevenueDocumento13 páginasNew and Old Conceptual Framework, Accounting Principles, Accounting Process, PAS 18 - RevenueDennis VelasquezAinda não há avaliações

- Class Participation 9 E7-18: Last Name - First Name - IDDocumento2 páginasClass Participation 9 E7-18: Last Name - First Name - IDaj singhAinda não há avaliações

- FFC Dental Clinic Business Website ProposalDocumento8 páginasFFC Dental Clinic Business Website ProposalKimmy Manzano0% (1)

- The Definitive Guide To Direct Investment in Real EstateDocumento13 páginasThe Definitive Guide To Direct Investment in Real EstateMaria KennedyAinda não há avaliações

- Depreciation Provisions and Reserves Class 11 NotesDocumento48 páginasDepreciation Provisions and Reserves Class 11 Notesjainayan8190Ainda não há avaliações

- CORPORATE GOVERNANCE... PowerpointDocumento81 páginasCORPORATE GOVERNANCE... PowerpointEng Tennyson SigaukeAinda não há avaliações

- Nord Gold: New Kid On The BlockDocumento34 páginasNord Gold: New Kid On The Blocksovereign01Ainda não há avaliações

- Chapter-5: Accounting For Merchandising OperationsDocumento39 páginasChapter-5: Accounting For Merchandising OperationsNoel Buenafe JrAinda não há avaliações

- Supply Chain Management Project: Team 1 DMART-Retail Business Analysis Akshaya (08) /ganesh (23) /rengarajanDocumento18 páginasSupply Chain Management Project: Team 1 DMART-Retail Business Analysis Akshaya (08) /ganesh (23) /rengarajanAkshaya Lakshminarasimhan75% (4)

- Interest Rates and Bond Valuation: All Rights ReservedDocumento53 páginasInterest Rates and Bond Valuation: All Rights ReservedMohamed Hussien0% (1)

- Chapter 5Documento36 páginasChapter 5Baby KhorAinda não há avaliações

- MKTG 201 - Principles of Marketing-Aneela Malik PDFDocumento4 páginasMKTG 201 - Principles of Marketing-Aneela Malik PDFmehmood aliAinda não há avaliações

- The PA I-78I-81 Logistics CorridorDocumento20 páginasThe PA I-78I-81 Logistics CorridorAnonymous Feglbx5Ainda não há avaliações

- P3 ModelsDocumento9 páginasP3 ModelsAbdullah Md ShadAinda não há avaliações

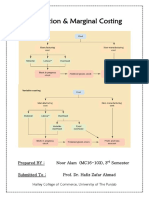

- Absorption & Marginal Costing - Noor Alam (MC16-103)Documento24 páginasAbsorption & Marginal Costing - Noor Alam (MC16-103)Ahmed Ali Khan100% (2)

- The Revaluation ModelDocumento20 páginasThe Revaluation ModelPRECIOUSAinda não há avaliações

- Rochmah Sucita Anggraini: Personal ProfileDocumento1 páginaRochmah Sucita Anggraini: Personal ProfileTia Yustika EnchancersAinda não há avaliações

- Rift Valley University: Department of Marketing Management Strategic Management Final Exam Based Assignments 60%Documento9 páginasRift Valley University: Department of Marketing Management Strategic Management Final Exam Based Assignments 60%Abdulaziz MohammedAinda não há avaliações

- Managerial Accounting 5th Edition Wild Shaw Solution ManualDocumento115 páginasManagerial Accounting 5th Edition Wild Shaw Solution Manualmarsha100% (23)

- BIIB Case Study-BDocumento29 páginasBIIB Case Study-BSurbhi BiyaniAinda não há avaliações

- CME Group Daily Bulletin GlossaryDocumento2 páginasCME Group Daily Bulletin GlossaryavadcsAinda não há avaliações

- 451 Research Pathfinder Report The Employee ExperienceDocumento12 páginas451 Research Pathfinder Report The Employee Experienceabubakar siddiqueAinda não há avaliações

- Introduction To Financial Planning-VK-2015Documento31 páginasIntroduction To Financial Planning-VK-2015Vinod Krishna MakkimaneAinda não há avaliações

- Most Important Questions For JE (COMMERCIAL)Documento23 páginasMost Important Questions For JE (COMMERCIAL)Manish KumarAinda não há avaliações

- Practice Problems - Karysse JalaoDocumento34 páginasPractice Problems - Karysse JalaoKarysse ArielleAinda não há avaliações

- Liquidity Management in Janatha Credit Co-Operative Society LTDDocumento6 páginasLiquidity Management in Janatha Credit Co-Operative Society LTDInternational Journal of Innovative Science and Research TechnologyAinda não há avaliações

- Enron: The Smartest Guys in The Room (2005)Documento2 páginasEnron: The Smartest Guys in The Room (2005)Frances CarpioAinda não há avaliações

- Chapter 9 Investment PropertyDocumento4 páginasChapter 9 Investment PropertyAngelica Joy ManaoisAinda não há avaliações