Você também pode gostar

- Chapter 24-Money, The Price Level, and InflationDocumento33 páginasChapter 24-Money, The Price Level, and InflationBin WangAinda não há avaliações

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- UNDP Covid-19 and Human Development 0Documento35 páginasUNDP Covid-19 and Human Development 0sofiabloemAinda não há avaliações

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Student Placement Tracker Batch 2017 - 19Documento10 páginasStudent Placement Tracker Batch 2017 - 19nsrivastav1Ainda não há avaliações

- WP392 PDFDocumento41 páginasWP392 PDFnapierlogsAinda não há avaliações

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- CM1 Flashcards Sample - Chapter 14Documento56 páginasCM1 Flashcards Sample - Chapter 14Bakari HamisiAinda não há avaliações

- Change Management Final VersionDocumento13 páginasChange Management Final VersionZheng LinAinda não há avaliações

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- SupplyDocumento19 páginasSupplykimcy19Ainda não há avaliações

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Intermediate Macro Mankiw Ch.7 12 Questions PDFDocumento143 páginasIntermediate Macro Mankiw Ch.7 12 Questions PDFYusuf ÇubukAinda não há avaliações

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- Example Application LetterDocumento12 páginasExample Application LetterDewa Atra100% (2)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Only Technical Analysis Book You Will Ever NeedDocumento143 páginasThe Only Technical Analysis Book You Will Ever Needasadmurodov00100% (3)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Problem Set I For International Trade # Partial Solutions ... - CER-ETH PDFDocumento14 páginasProblem Set I For International Trade # Partial Solutions ... - CER-ETH PDFJGAinda não há avaliações

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- pc1 Resuelta PDFDocumento15 páginaspc1 Resuelta PDFWilliam Vasquez SanchezAinda não há avaliações

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- SSE 107 Macroeconomics SG 5Documento8 páginasSSE 107 Macroeconomics SG 5Aila Erika EgrosAinda não há avaliações

- Ryerson Finance 601 Test BankDocumento4 páginasRyerson Finance 601 Test BankKaushal BasnetAinda não há avaliações

- What Is Corporate Restructuring?: Any Change in A Company's:,, or That Is Outside Its Ordinary Course of BusinessDocumento22 páginasWhat Is Corporate Restructuring?: Any Change in A Company's:,, or That Is Outside Its Ordinary Course of BusinessRidhima SharmaAinda não há avaliações

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Chapter 11: Public Goods and Common Resource Learning ObjectivesDocumento5 páginasChapter 11: Public Goods and Common Resource Learning ObjectivesGuru DeepAinda não há avaliações

- 40 Marketing Interview Questions and AnswersDocumento8 páginas40 Marketing Interview Questions and AnswersAnonymous C5MZ11rK13Ainda não há avaliações

- Materi 1 Engineering Economic DecisionsDocumento16 páginasMateri 1 Engineering Economic DecisionsnoixieAinda não há avaliações

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- Valuation - NotesDocumento41 páginasValuation - NotessreginatoAinda não há avaliações

- RF Bhansali Negative Interest RatesDocumento116 páginasRF Bhansali Negative Interest RatesOwm Close CorporationAinda não há avaliações

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- Sticky Prices Notes For Macroeconomics by Carlin & SoskiceDocumento13 páginasSticky Prices Notes For Macroeconomics by Carlin & SoskiceSiddharthSardaAinda não há avaliações

- Economics Questionnaire SampleDocumento2 páginasEconomics Questionnaire SamplekinikinayyAinda não há avaliações

- Chapter 11 PDFDocumento8 páginasChapter 11 PDFJulie HuynhAinda não há avaliações

- Property CyclesDocumento16 páginasProperty CyclesMarta NowakowskaAinda não há avaliações

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Essay About GlobalizationDocumento5 páginasEssay About GlobalizationJackelin Salguedo FernandezAinda não há avaliações

- How To Record Opening and Closing StockDocumento5 páginasHow To Record Opening and Closing StockSUZANAMIKEAinda não há avaliações

- 2010 12 Applying A Risk Budgeting Approach To Active Portfolio ConstructionDocumento7 páginas2010 12 Applying A Risk Budgeting Approach To Active Portfolio Constructionjeete17Ainda não há avaliações

- (Catherine M. Price (Auth.) ) Welfare Economics PDFDocumento179 páginas(Catherine M. Price (Auth.) ) Welfare Economics PDFNino PapachashviliAinda não há avaliações

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Chapter 1 Derivatives An IntroductionDocumento10 páginasChapter 1 Derivatives An Introductiongovindpatel1990Ainda não há avaliações

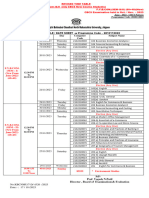

- Revised Time Table of FY-SY-TYBCom Sem I To VI New Old CBCS-CGPA Exam - To Be Held in Oct Nov-2023Documento5 páginasRevised Time Table of FY-SY-TYBCom Sem I To VI New Old CBCS-CGPA Exam - To Be Held in Oct Nov-2023Viraj SharmaAinda não há avaliações