Você também pode gostar

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Leadership and Strategic Management - GonoDocumento47 páginasLeadership and Strategic Management - GonoDat Nguyen Huy100% (1)

- Menu EngineeringDocumento9 páginasMenu Engineeringfirstman31Ainda não há avaliações

- Volvo CE Special Tool Catalog 02092023Documento647 páginasVolvo CE Special Tool Catalog 02092023Bradley D Kinser0% (1)

- Personal Selling in Pharma Marketing: Shilpa GargDocumento17 páginasPersonal Selling in Pharma Marketing: Shilpa GargNikhil MahajanAinda não há avaliações

- Sources of Finance: Ib Business & Management A Course Companion (2009) P146-157 (Clark Edition)Documento54 páginasSources of Finance: Ib Business & Management A Course Companion (2009) P146-157 (Clark Edition)sshyamsunder100% (1)

- Sample of Memorandum of Agreement (MOA)Documento12 páginasSample of Memorandum of Agreement (MOA)Johanna BelestaAinda não há avaliações

- Financial Accounting AssignmentDocumento11 páginasFinancial Accounting AssignmentMadhawa RanawakeAinda não há avaliações

- Agency TheoryDocumento2 páginasAgency TheoryAmeh SundayAinda não há avaliações

- VT - DUNS - Human Services 03.06.17 PDFDocumento5 páginasVT - DUNS - Human Services 03.06.17 PDFann vom EigenAinda não há avaliações

- 1 The Objective in Corporate FinanceDocumento51 páginas1 The Objective in Corporate FinanceFrank MatthewsAinda não há avaliações

- The Input Tools Require Strategists To Quantify Subjectivity During Early Stages of The Strategy-Formulation ProcessDocumento24 páginasThe Input Tools Require Strategists To Quantify Subjectivity During Early Stages of The Strategy-Formulation ProcessHannah Ruth M. GarpaAinda não há avaliações

- Cross TAB in Crystal ReportsDocumento15 páginasCross TAB in Crystal ReportsMarcelo Damasceno ValeAinda não há avaliações

- PARCOR-SIMILARITIESDocumento2 páginasPARCOR-SIMILARITIESHoney Lizette SunthornAinda não há avaliações

- MBA Project Report On Dividend PolicyDocumento67 páginasMBA Project Report On Dividend PolicyMohit Kumar33% (3)

- 1st Year Assignments 2019-20 (English)Documento8 páginas1st Year Assignments 2019-20 (English)NarasimhaAinda não há avaliações

- Neax 2000 Ips Reference GuideDocumento421 páginasNeax 2000 Ips Reference Guideantony777Ainda não há avaliações

- Din 11864 / Din 11853: Armaturenwerk Hötensleben GMBHDocumento70 páginasDin 11864 / Din 11853: Armaturenwerk Hötensleben GMBHkrisAinda não há avaliações

- Clementi TownDocumento3 páginasClementi TownjuronglakesideAinda não há avaliações

- 01 Pengantar SCMDocumento46 páginas01 Pengantar SCMAdit K. BagaskoroAinda não há avaliações

- Oil and Gas Industry Overview SsDocumento2 páginasOil and Gas Industry Overview SsVidhu PrabhakarAinda não há avaliações

- Q4M1Documento54 páginasQ4M1Klyn AgananAinda não há avaliações

- RDL1 - Activity 1.2Documento1 páginaRDL1 - Activity 1.2EL FuentesAinda não há avaliações

- Group 13 Excel AssignmentDocumento6 páginasGroup 13 Excel AssignmentNimmy MathewAinda não há avaliações

- Gri 202 Market Presence 2016Documento10 páginasGri 202 Market Presence 2016Pablo MalgesiniAinda não há avaliações

- Ifrs 5Documento2 páginasIfrs 5Foititika.netAinda não há avaliações

- Bony IauDocumento572 páginasBony IauTommy HectorAinda não há avaliações

- Venture Pulse Q1 16Documento101 páginasVenture Pulse Q1 16BusolaAinda não há avaliações

- Report On Financial Market Review by The Hong Kong SAR Government in April 1998Documento223 páginasReport On Financial Market Review by The Hong Kong SAR Government in April 1998Tsang Shu-kiAinda não há avaliações

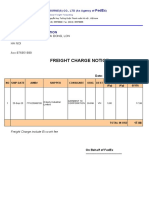

- Freight Charge Notice: To: Garment 10 CorporationDocumento4 páginasFreight Charge Notice: To: Garment 10 CorporationThuy HoangAinda não há avaliações

- Integrated Review Ii: Advanced Financial Accounting and Reporting Module 3: Special Revenue Recognition I. Installment SalesDocumento18 páginasIntegrated Review Ii: Advanced Financial Accounting and Reporting Module 3: Special Revenue Recognition I. Installment SalesDarren Joy CoronaAinda não há avaliações