Você também pode gostar

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Final Word-Over The Counter Exchange of IndiaDocumento14 páginasFinal Word-Over The Counter Exchange of IndiaVidita VanageAinda não há avaliações

- Dissertation Report On Cash Management of Standard Chartered BankDocumento92 páginasDissertation Report On Cash Management of Standard Chartered BankSunil Kumar100% (15)

- Tutorial Letter 108/0/2023: TAX4861 NTA4861Documento75 páginasTutorial Letter 108/0/2023: TAX4861 NTA4861ByouAinda não há avaliações

- Equity Portfolio Management StrategiesDocumento30 páginasEquity Portfolio Management StrategiesSdAinda não há avaliações

- Customer Request and Complaint Form: Please Tick Relevant Request Service Request NumberDocumento1 páginaCustomer Request and Complaint Form: Please Tick Relevant Request Service Request NumberDesikanAinda não há avaliações

- Home Loans V1Documento38 páginasHome Loans V1katari vajrakuntAinda não há avaliações

- UntitledDocumento6 páginasUntitledB - Clores, Mark RyanAinda não há avaliações

- Gente 2015Documento27 páginasGente 2015Very BudiyantoAinda não há avaliações

- Introduction To AccountingDocumento14 páginasIntroduction To AccountingJunaid IslamAinda não há avaliações

- How To Plan A Home BudgetDocumento10 páginasHow To Plan A Home BudgetshreyassrinathAinda não há avaliações

- FINA1904 - ALL Weitzel - Spring 2019Documento11 páginasFINA1904 - ALL Weitzel - Spring 2019JamesAinda não há avaliações

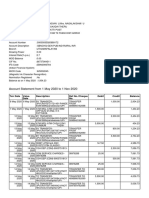

- Account Statement From 1 May 2020 To 1 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocumento9 páginasAccount Statement From 1 May 2020 To 1 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceChellapandiAinda não há avaliações

- Group AssignmentDocumento5 páginasGroup AssignmentDuc Thien LuongAinda não há avaliações

- Punjab Financial Rules Vol-I-2019 PDFDocumento339 páginasPunjab Financial Rules Vol-I-2019 PDFsalmanshahidkhan226Ainda não há avaliações

- Global Family Office Report 2023.pdf - CoredownloadDocumento102 páginasGlobal Family Office Report 2023.pdf - Coredownloadpderby1Ainda não há avaliações

- FX Get DoneDocumento2 páginasFX Get DoneDev GogoiAinda não há avaliações

- SMFG India Credit Company LimitedDocumento9 páginasSMFG India Credit Company Limitedvatsal sinhaAinda não há avaliações

- Account Statement From 1 Mar 2023 To 4 Mar 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocumento2 páginasAccount Statement From 1 Mar 2023 To 4 Mar 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balancesameer bawejaAinda não há avaliações

- Major Project ReportDocumento12 páginasMajor Project ReportAMAN SAXENAAinda não há avaliações

- BIR RULING NO. 100-17: SGV & CoDocumento10 páginasBIR RULING NO. 100-17: SGV & CoThe GiverAinda não há avaliações

- Lecture 7Documento68 páginasLecture 7Hassan NadeemAinda não há avaliações

- FINANCIAL MANAGEMENT Full ModuleDocumento72 páginasFINANCIAL MANAGEMENT Full Modulenegamedhane58Ainda não há avaliações

- Finance MCQDocumento46 páginasFinance MCQPallavi GAinda não há avaliações

- SHR TCDocumento2 páginasSHR TCManikandanAinda não há avaliações

- Government of Kerala: Rs. Rs. RsDocumento25 páginasGovernment of Kerala: Rs. Rs. RsmuhammedAinda não há avaliações

- Block 0 - Bitcoin Cash (BCH) Block ExplorerDocumento2 páginasBlock 0 - Bitcoin Cash (BCH) Block ExplorerscribdtAinda não há avaliações

- Chapter 2 Capital MarketsDocumento9 páginasChapter 2 Capital MarketsFarah Nader Gooda100% (1)

- Chapter 4 - Partnership LiquidationDocumento4 páginasChapter 4 - Partnership LiquidationMikaella BengcoAinda não há avaliações

- Bookkeeper Job DescriptionDocumento2 páginasBookkeeper Job Descriptionvener magpayoAinda não há avaliações

- Industrial FinanceDocumento11 páginasIndustrial Financedesaijpr90% (10)