Você também pode gostar

- Commodities Primer - RBS (2009)Documento166 páginasCommodities Primer - RBS (2009)tacolebelAinda não há avaliações

- 8 Profit Activators - Joe Polish Dan KennedyDocumento33 páginas8 Profit Activators - Joe Polish Dan KennedyRJ100% (1)

- Joint by Products CostingDocumento5 páginasJoint by Products CostingJenelyn FloresAinda não há avaliações

- SAP Logistic Invoice VerificationDocumento29 páginasSAP Logistic Invoice VerificationPraveen KumarAinda não há avaliações

- CIPS L4-Negotiating and Contracting in Procurement and SupplyDocumento166 páginasCIPS L4-Negotiating and Contracting in Procurement and SupplyAsheque Iqbal100% (3)

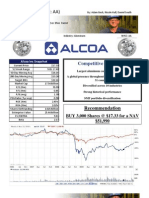

- Alcoa SwotDocumento44 páginasAlcoa SwotKURATHEESH1Ainda não há avaliações

- Business Plan 5000 LayersDocumento11 páginasBusiness Plan 5000 Layersjha.indrajeet79% (29)

- Notes On Sales 1458 1521Documento20 páginasNotes On Sales 1458 1521edelyn roncales0% (1)

- Lead Smelting and Refining, With Some Notes on Lead MiningNo EverandLead Smelting and Refining, With Some Notes on Lead MiningAinda não há avaliações

- Coal Outlook ReportDocumento51 páginasCoal Outlook ReportSterios SouyoutzoglouAinda não há avaliações

- 8633 - International Cost Construction Report FINAL2Documento9 páginas8633 - International Cost Construction Report FINAL2shabina921Ainda não há avaliações

- Unifine Richardson CaseDocumento6 páginasUnifine Richardson Casekoshreed100% (2)

- Die Casting Metallurgy: Butterworths Monographs in MaterialsNo EverandDie Casting Metallurgy: Butterworths Monographs in MaterialsNota: 3.5 de 5 estrelas3.5/5 (2)

- The Nickel Market Out Look 070414 PDocumento42 páginasThe Nickel Market Out Look 070414 Parkent98Ainda não há avaliações

- Chapter 7 - International Parity Conditions - BlackboardDocumento33 páginasChapter 7 - International Parity Conditions - BlackboardCarlosAinda não há avaliações

- Copper Smelter TC and RCDocumento2 páginasCopper Smelter TC and RCcbqucbquAinda não há avaliações

- Global Base Metals Review: November, 2005Documento3 páginasGlobal Base Metals Review: November, 2005user2127Ainda não há avaliações

- An Impressive Start To The Year For Nickel As It Hits 10-Year HighDocumento7 páginasAn Impressive Start To The Year For Nickel As It Hits 10-Year HighOwm Close CorporationAinda não há avaliações

- Commodities and Energy, January 2014Documento4 páginasCommodities and Energy, January 2014Swedbank AB (publ)Ainda não há avaliações

- Commodity Research Report: Copper Fundamental AnalysisDocumento18 páginasCommodity Research Report: Copper Fundamental AnalysisarathyachusAinda não há avaliações

- Nikl Metals WeeklyDocumento7 páginasNikl Metals WeeklybodaiAinda não há avaliações

- Análisis de Mercado Del Metal PlomoDocumento6 páginasAnálisis de Mercado Del Metal PlomoSebastian R Pa MonAinda não há avaliações

- Trabajo II Final RDocumento7 páginasTrabajo II Final RSebastian R Pa MonAinda não há avaliações

- Report-Changing Economies of SteelDocumento16 páginasReport-Changing Economies of SteelprtapbistAinda não há avaliações

- Rba SteelDocumento3 páginasRba Steeltommy-hl6920Ainda não há avaliações

- Aluminium Industry CARE 060112Documento5 páginasAluminium Industry CARE 060112kavspopsAinda não há avaliações

- The Volatility of Commodity Prices PDFDocumento6 páginasThe Volatility of Commodity Prices PDFNishatAinda não há avaliações

- Chinese Silver Market 2012Documento26 páginasChinese Silver Market 2012Nestor Alejandro HillarAinda não há avaliações

- Production and Consumption Trends in The Total Finished Steel Market (In Million Tonnes)Documento6 páginasProduction and Consumption Trends in The Total Finished Steel Market (In Million Tonnes)Monish RcAinda não há avaliações

- Fitch - 2012 Outlook - EMEA Metals - Mining - 02 Dec 2011Documento7 páginasFitch - 2012 Outlook - EMEA Metals - Mining - 02 Dec 2011esteycarAinda não há avaliações

- Do April'11Documento7 páginasDo April'11Satyabrata BeheraAinda não há avaliações

- Stainless Steel JuneDocumento19 páginasStainless Steel JuneJoshua WalkerAinda não há avaliações

- China Sneezes and World Catches C... 4 Min Read. Updated: May 29 2021, 12:00 AmDocumento4 páginasChina Sneezes and World Catches C... 4 Min Read. Updated: May 29 2021, 12:00 AmAmit SharmaAinda não há avaliações

- Five Forces AnalysisDocumento4 páginasFive Forces Analysisneekuj malikAinda não há avaliações

- Energy & Commodities - November 16, 2012Documento4 páginasEnergy & Commodities - November 16, 2012Swedbank AB (publ)Ainda não há avaliações

- Commodities 2011 Craig DrakeDocumento1 páginaCommodities 2011 Craig DrakecsdrakeAinda não há avaliações

- Analysis of Coppers Market and Price Focus On The Last Decades Change and Its Future Trend PDFDocumento8 páginasAnalysis of Coppers Market and Price Focus On The Last Decades Change and Its Future Trend PDFMoe EcchiAinda não há avaliações

- B0611 GLDocumento36 páginasB0611 GLArnu Felix CamposAinda não há avaliações

- Result Review 4Q FY 2013Documento9 páginasResult Review 4Q FY 2013Angel BrokingAinda não há avaliações

- Methods Are We Going To Implement For Concentration 2222Documento3 páginasMethods Are We Going To Implement For Concentration 2222Mash RanoAinda não há avaliações

- Nickel Report FinalDocumento19 páginasNickel Report Finalamjr1001Ainda não há avaliações

- Global Steel Report 2013 ER0046Documento75 páginasGlobal Steel Report 2013 ER0046Spidy BondAinda não há avaliações

- IEA Coal Medium TermDocumento4 páginasIEA Coal Medium Termtimnorris1Ainda não há avaliações

- Global and Regional Developments in Primary and Secondary Lead SupplyDocumento4 páginasGlobal and Regional Developments in Primary and Secondary Lead SupplyetayojcAinda não há avaliações

- Asammd 0309Documento7 páginasAsammd 0309AkimBiAinda não há avaliações

- MS 2012 Outlook: Precious MetalsDocumento6 páginasMS 2012 Outlook: Precious Metalsz2009z2009Ainda não há avaliações

- Essar Steel Limited Annual ReportDocumento10 páginasEssar Steel Limited Annual Reportjagdish62103Ainda não há avaliações

- Strategic Management, Jindal SteelDocumento12 páginasStrategic Management, Jindal Steellino67% (3)

- Metals Result Review, 22nd February, 2013Documento8 páginasMetals Result Review, 22nd February, 2013Angel BrokingAinda não há avaliações

- NPI Application in ChinaDocumento31 páginasNPI Application in Chinamushava nyokaAinda não há avaliações

- Executive Summary: Chart 1. Lead Prices 2008-2011Documento4 páginasExecutive Summary: Chart 1. Lead Prices 2008-2011FransiscaBerlianiDewiThanjoyoAinda não há avaliações

- Risk Managing Volatile MarketsDocumento41 páginasRisk Managing Volatile MarketsSandipAinda não há avaliações

- A Study of Electronic Data Storage Steel Factory in Mumbai11 150218034403 Conversion Gate02Documento51 páginasA Study of Electronic Data Storage Steel Factory in Mumbai11 150218034403 Conversion Gate02NIKHIL CHAUHANAinda não há avaliações

- Project Report On: Oligopoly Market Structure of Aluminium Industry in IndiaDocumento5 páginasProject Report On: Oligopoly Market Structure of Aluminium Industry in IndiaShruti SharmaAinda não há avaliações

- Information 2Documento2 páginasInformation 2Mash RanoAinda não há avaliações

- BML 200 Sep - Dec 2021 WbaDocumento6 páginasBML 200 Sep - Dec 2021 WbaKenya's FinestAinda não há avaliações

- National Steel Policy 2017Documento31 páginasNational Steel Policy 2017Jagdish AroraAinda não há avaliações

- Global Macro Daily LONDON Open (2014!01!16)Documento14 páginasGlobal Macro Daily LONDON Open (2014!01!16)BlundersAinda não há avaliações

- JSW - FInal - 2Documento10 páginasJSW - FInal - 2Devika SinghaniaAinda não há avaliações

- Result Review Metal, 1Q FY 2014Documento10 páginasResult Review Metal, 1Q FY 2014Angel BrokingAinda não há avaliações

- 2QFY2013 - Result Analysis: Profit Remains Under PressureDocumento9 páginas2QFY2013 - Result Analysis: Profit Remains Under PressureAngel BrokingAinda não há avaliações

- Analystpresentation CRU PDFDocumento19 páginasAnalystpresentation CRU PDFSatyabrata BeheraAinda não há avaliações

- Hindalco Industries Initiating CoverageDocumento24 páginasHindalco Industries Initiating CoveragePankaj Kumar BothraAinda não há avaliações

- 0909 PDFDocumento3 páginas0909 PDFCris CristyAinda não há avaliações

- 2019preview - NPI To Extend Its Dominant Role in Nickel Supply - Metal BulletinDocumento6 páginas2019preview - NPI To Extend Its Dominant Role in Nickel Supply - Metal BulletinErie HaryantoAinda não há avaliações

- Alternative Materials for One Cent CoinageNo EverandAlternative Materials for One Cent CoinageAinda não há avaliações

- Market Research, Global Market for Germanium and Germanium ProductsNo EverandMarket Research, Global Market for Germanium and Germanium ProductsAinda não há avaliações

- 118059-2000-Heirs of San Andres v. RodriguezDocumento11 páginas118059-2000-Heirs of San Andres v. RodriguezJuanaAinda não há avaliações

- Case Analysis 3Documento3 páginasCase Analysis 3Aigerim100% (1)

- Foundations of Financial Management Canadian 11th Edition Block Test BankDocumento37 páginasFoundations of Financial Management Canadian 11th Edition Block Test BankDennisLonggtqrx100% (12)

- Ananya Goswami 41943020 2nd Mid EDDocumento5 páginasAnanya Goswami 41943020 2nd Mid EDAnanya GoswamiAinda não há avaliações

- JD Edwards - Sales Order ManagmentDocumento778 páginasJD Edwards - Sales Order ManagmentToronto_Scorpions100% (3)

- 7p Marketi̇ng StrategyDocumento6 páginas7p Marketi̇ng StrategyIsmail SemerciAinda não há avaliações

- Objectives of The Price PolicyDocumento3 páginasObjectives of The Price PolicyPrasanna Hegde100% (1)

- Chapter 14Documento27 páginasChapter 14narasimha100% (1)

- Lychee Is A Traditional Fruit of Vietnam, Which First Occurred inDocumento4 páginasLychee Is A Traditional Fruit of Vietnam, Which First Occurred inAn DoAinda não há avaliações

- Project On Value Added TaxDocumento38 páginasProject On Value Added TaxKavita NadarAinda não há avaliações

- Tender Documents Types of Contracts: Uantity Urveying AND StimationDocumento16 páginasTender Documents Types of Contracts: Uantity Urveying AND StimationFortiter FysproAinda não há avaliações

- Working CapitalDocumento12 páginasWorking CapitalYasin Misvari T MAinda não há avaliações

- Failure of SubhikshaDocumento48 páginasFailure of SubhikshaJapjiv Singh100% (1)

- Regulatory Impact of The 2021 Texas Energy CrisisDocumento12 páginasRegulatory Impact of The 2021 Texas Energy CrisisjgravisAinda não há avaliações

- BIR - Remittance of CWT (Form 1606) Discussion 1Documento92 páginasBIR - Remittance of CWT (Form 1606) Discussion 1Roy RitagaAinda não há avaliações

- 70trades TC V1.5 March 2020Documento7 páginas70trades TC V1.5 March 2020devaraj kAinda não há avaliações

- Colander's Economics, 6 Answers To End-of-Chapter Questions: EditionDocumento195 páginasColander's Economics, 6 Answers To End-of-Chapter Questions: EditionKiran100% (2)

- B123-FTHE-Spring 2020-2021Documento8 páginasB123-FTHE-Spring 2020-2021MUSTAFAAinda não há avaliações

- Eastman Kodak Case AnalysisDocumento3 páginasEastman Kodak Case AnalysisAkshay Goyal100% (1)

- Lesson Two-3Documento10 páginasLesson Two-3Ruth NyawiraAinda não há avaliações

- Managerial EconomicsDocumento158 páginasManagerial EconomicshemantttttAinda não há avaliações

- WalMart Effect On The US EconomyDocumento4 páginasWalMart Effect On The US Economynikhil_chitalia14Ainda não há avaliações