Você também pode gostar

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Presentation Schedule2010BWFLYER FinalDocumento1 páginaPresentation Schedule2010BWFLYER FinalRamon Salsas EscatAinda não há avaliações

- Barro and Grossman - A General Disequilibrium Model of Income and Employment PDFDocumento12 páginasBarro and Grossman - A General Disequilibrium Model of Income and Employment PDFDouglas Fabrízzio CamargoAinda não há avaliações

- Trump and Globalization - 0Documento14 páginasTrump and Globalization - 0Alexei PalamaruAinda não há avaliações

- Company SecretaryDocumento22 páginasCompany SecretaryNikhil DeshpandeAinda não há avaliações

- Rates and ProportionalityDocumento23 páginasRates and ProportionalityJade EncarnacionAinda não há avaliações

- Chapter 2.0Documento22 páginasChapter 2.0MOHAMAD ASHRAF BIN MOHAMAD TAJARI MoeAinda não há avaliações

- Why Poverty Has Declined - Inquirer OpinionDocumento6 páginasWhy Poverty Has Declined - Inquirer OpinionRamon T. Conducto IIAinda não há avaliações

- The Currency Correlation Secret - TwoDocumento10 páginasThe Currency Correlation Secret - Twofebrichow100% (1)

- PDF Rencana Pengembangan Madrasah Contoh RPMDocumento19 páginasPDF Rencana Pengembangan Madrasah Contoh RPMTeguh KaryaAinda não há avaliações

- Guc 57 56 21578 2022-06-21T23 25 51Documento3 páginasGuc 57 56 21578 2022-06-21T23 25 51Mariam MhamoudAinda não há avaliações

- BinsDocumento1 páginaBinsFosterAsanteAinda não há avaliações

- Accounting ProjectDocumento33 páginasAccounting Projectapi-353552300100% (1)

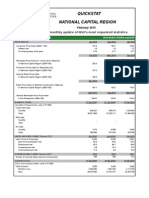

- Quickstat National Capital Region: A Monthly Update of NSO's Most Requested StatisticsDocumento3 páginasQuickstat National Capital Region: A Monthly Update of NSO's Most Requested StatisticsDaniel John Cañares LegaspiAinda não há avaliações

- Strategic Plan DRAFTVolunteerDocumento85 páginasStrategic Plan DRAFTVolunteerLourdes SusaetaAinda não há avaliações

- Factors Responsible For The Location of Primary, Secondary, and Tertiary Sector Industries in Various Parts of The World (Including India)Documento53 páginasFactors Responsible For The Location of Primary, Secondary, and Tertiary Sector Industries in Various Parts of The World (Including India)Aditya KumarAinda não há avaliações

- Operation Flood White Revolution Muhammad Ali 2007-Va-378 Bs (Hons) Dairy TechnologyDocumento23 páginasOperation Flood White Revolution Muhammad Ali 2007-Va-378 Bs (Hons) Dairy TechnologyShawn MathiasAinda não há avaliações

- Amma Mobile InsuranceDocumento1 páginaAmma Mobile InsuranceANANTH JAinda não há avaliações

- Revision MAT Number Securing A C Sheet BDocumento1 páginaRevision MAT Number Securing A C Sheet Bmanobilli30Ainda não há avaliações

- ItcDocumento10 páginasItcPrabhav ChauhanAinda não há avaliações

- Profile Guide: Corrugated Sheet & Foam FillersDocumento275 páginasProfile Guide: Corrugated Sheet & Foam FillersnguyenanhtuanbAinda não há avaliações

- Flight Booking Invoice MMTDocumento2 páginasFlight Booking Invoice MMTNanak JAYANTAAinda não há avaliações

- Midc MumbaiDocumento26 páginasMidc MumbaiparagAinda não há avaliações

- Electoral Roll For Auto Tyres Tubes Panel of CAPEXIL For The Year 2021 22Documento2 páginasElectoral Roll For Auto Tyres Tubes Panel of CAPEXIL For The Year 2021 22asif.ayyub7624Ainda não há avaliações

- Melinda Coopers Family Values Between Neoliberalism and The New Social ConservatismDocumento4 páginasMelinda Coopers Family Values Between Neoliberalism and The New Social ConservatismmarianfelizAinda não há avaliações

- Evaluation Sheet For Extension ServicesDocumento1 páginaEvaluation Sheet For Extension Servicesailine donaireAinda não há avaliações

- What Is Public Choice Theory PDFDocumento8 páginasWhat Is Public Choice Theory PDFSita SivalingamAinda não há avaliações

- List of Important International Organizations and Their Headquarter 2017Documento6 páginasList of Important International Organizations and Their Headquarter 2017Kalaivani BaskarAinda não há avaliações

- mt4 IndicatorDocumento4 páginasmt4 IndicatorNikhil Pillay100% (1)

- 1991 PV Sanjay BaruDocumento131 páginas1991 PV Sanjay Barukishore kommi100% (2)

- Galvor CaseDocumento10 páginasGalvor CaseLawi AnupamAinda não há avaliações