Você também pode gostar

- The Super ProjectDocumento5 páginasThe Super ProjectAbhiAinda não há avaliações

- Super Project CaseDocumento16 páginasSuper Project Casekanne_phAinda não há avaliações

- Super Project - July 2019Documento4 páginasSuper Project - July 2019Wally WannallAinda não há avaliações

- Super ProjectDocumento2 páginasSuper ProjectAnkit MehtaAinda não há avaliações

- Analisis Super ProjectDocumento4 páginasAnalisis Super Projectrcatherineb50% (2)

- Super Project: Corporate FinanceDocumento8 páginasSuper Project: Corporate Financebtarpara1Ainda não há avaliações

- The Super Project Case AnalysisDocumento5 páginasThe Super Project Case Analysisgpadhye123Ainda não há avaliações

- Super ProjectDocumento12 páginasSuper ProjectSrija LahiriAinda não há avaliações

- Super ProjectDocumento12 páginasSuper Projectkaran_w3Ainda não há avaliações

- Super ProjectDocumento1 páginaSuper ProjectVaibhav SaithAinda não há avaliações

- The Super Project: Mark Smukler, Griffin Meyer & Estefania GarciaDocumento8 páginasThe Super Project: Mark Smukler, Griffin Meyer & Estefania GarciaMark SmuklerAinda não há avaliações

- Super ProjectDocumento2 páginasSuper ProjectQiang ChenAinda não há avaliações

- Super ProjectDocumento6 páginasSuper ProjectMônica MelloAinda não há avaliações

- Super Project FinalDocumento29 páginasSuper Project FinalSamuel ChuquistaAinda não há avaliações

- Super Project AnalysisDocumento6 páginasSuper Project AnalysisPeeyush Khandka0% (1)

- Case The Super ProjectDocumento6 páginasCase The Super ProjectpaulAinda não há avaliações

- Nagornov Super Project CaseDocumento3 páginasNagornov Super Project Casetbsssilva100% (1)

- Ocean Carriers Executive SummaryDocumento2 páginasOcean Carriers Executive SummaryAniket KaushikAinda não há avaliações

- Case: Calpine Corporation: The Evolution From Project To Corporate FinanceDocumento7 páginasCase: Calpine Corporation: The Evolution From Project To Corporate FinanceKshitishAinda não há avaliações

- Sealed Air Corporation's Leveraged RecapitalizationDocumento7 páginasSealed Air Corporation's Leveraged RecapitalizationKumarAinda não há avaliações

- EC2101 Practice Problems 8 SolutionDocumento3 páginasEC2101 Practice Problems 8 Solutiongravity_coreAinda não há avaliações

- Analyse The Structure of The Personal Computer Industry Over The Last 15 YearsDocumento7 páginasAnalyse The Structure of The Personal Computer Industry Over The Last 15 Yearsdbleyzer100% (1)

- Group DDocumento16 páginasGroup DAbhishek VermaAinda não há avaliações

- Chasecase PaperDocumento10 páginasChasecase PaperadtyshkhrAinda não há avaliações

- Lockheed Case SolutionDocumento3 páginasLockheed Case SolutionKashish SrivastavaAinda não há avaliações

- A Note On Leveraged RecapitalizationDocumento5 páginasA Note On Leveraged Recapitalizationkuch bhiAinda não há avaliações

- Case 3 - Ocean Carriers Case PreparationDocumento1 páginaCase 3 - Ocean Carriers Case PreparationinsanomonkeyAinda não há avaliações

- Super Project Case SolutionDocumento3 páginasSuper Project Case SolutionasaqAinda não há avaliações

- Lockheed Tristar Case Study 11020241041Documento19 páginasLockheed Tristar Case Study 11020241041R Harika Reddy100% (7)

- Electronic Arts in Online Gaming PDFDocumento7 páginasElectronic Arts in Online Gaming PDFvgAinda não há avaliações

- BMA 12e SM CH 27 Final PDFDocumento9 páginasBMA 12e SM CH 27 Final PDFNikhil ChadhaAinda não há avaliações

- Question-Set 2: How Did You Handle The Ambiguity in Your Decision-Making? What WasDocumento6 páginasQuestion-Set 2: How Did You Handle The Ambiguity in Your Decision-Making? What WasishaAinda não há avaliações

- Sample ProblemsDocumento9 páginasSample ProblemsDoshi VaibhavAinda não há avaliações

- Buckeye Bank CaseDocumento7 páginasBuckeye Bank CasePulkit Mathur0% (2)

- CBRM Calpine Case - Group 4 SubmissionDocumento4 páginasCBRM Calpine Case - Group 4 SubmissionPranavAinda não há avaliações

- HWDocumento6 páginasHWaarushiAinda não há avaliações

- WellfleetDocumento3 páginasWellfleetAziez Daniel AkmalAinda não há avaliações

- Cooper Industries Case QuestionsDocumento3 páginasCooper Industries Case QuestionsChip choiAinda não há avaliações

- Assignment 2 Lockheed CaseDocumento6 páginasAssignment 2 Lockheed CaseBob MarlowAinda não há avaliações

- OM Scott Case AnalysisDocumento20 páginasOM Scott Case AnalysissushilkhannaAinda não há avaliações

- Case Analysis I American Chemical CorporationDocumento13 páginasCase Analysis I American Chemical CorporationamuakaAinda não há avaliações

- Facebook IPO Valuation AnalysisDocumento13 páginasFacebook IPO Valuation AnalysisMegha BepariAinda não há avaliações

- CasoDocumento20 páginasCasoasmaAinda não há avaliações

- SUN Brewing (A)Documento6 páginasSUN Brewing (A)Ilya KAinda não há avaliações

- Sun Brewing Case ExhibitsDocumento26 páginasSun Brewing Case ExhibitsShshankAinda não há avaliações

- M&A and Corporate Restructuring) - Prof. Ercos Valdivieso: Jung Keun Kim, Yoon Ho Hur, Soo Hyun Ahn, Jee Hyun KoDocumento2 páginasM&A and Corporate Restructuring) - Prof. Ercos Valdivieso: Jung Keun Kim, Yoon Ho Hur, Soo Hyun Ahn, Jee Hyun Ko고지현100% (1)

- Decision Models and Optimization: Indian School of Business Assignment 4Documento8 páginasDecision Models and Optimization: Indian School of Business Assignment 4NAAinda não há avaliações

- American Home Products CorporationDocumento7 páginasAmerican Home Products Corporationpancaspe100% (2)

- FRAV Individual Assignment - Pranjali Silimkar - 2016PGP278Documento12 páginasFRAV Individual Assignment - Pranjali Silimkar - 2016PGP278pranjaligAinda não há avaliações

- Sealed Air Corporation's Leveraged Recapitalization (A)Documento7 páginasSealed Air Corporation's Leveraged Recapitalization (A)Jyoti GuptaAinda não há avaliações

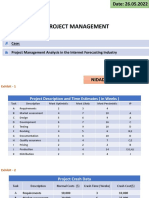

- Project Management Analysis in The Internet Forecasting IndustryDocumento14 páginasProject Management Analysis in The Internet Forecasting IndustryNiranjan NidadavoluAinda não há avaliações

- Polaroid Corporation: Group MembersDocumento7 páginasPolaroid Corporation: Group MemberscristinahumaAinda não há avaliações

- Tire City IncDocumento3 páginasTire City IncAlberto RcAinda não há avaliações

- Krispy Kreme Doughnuts: "It Ain't Just The Doughnuts That Are Glazed!"Documento9 páginasKrispy Kreme Doughnuts: "It Ain't Just The Doughnuts That Are Glazed!"dmaia12Ainda não há avaliações

- Case 5 Midland Energy Case ProjectDocumento7 páginasCase 5 Midland Energy Case ProjectCourse HeroAinda não há avaliações

- Case 22 Victoria Chemicals A DONEDocumento14 páginasCase 22 Victoria Chemicals A DONEJordan Green100% (5)

- Aerocomp Inc Case Study Week 7Documento5 páginasAerocomp Inc Case Study Week 7Aguntuk Shawon100% (4)

- Hola Kola - Docx 2Documento3 páginasHola Kola - Docx 2Gabriela PereiraAinda não há avaliações

- Baird - Euroland Foods CaseDocumento5 páginasBaird - Euroland Foods CaseKyleAinda não há avaliações

- Capital Budgeting - Adv IssuesDocumento21 páginasCapital Budgeting - Adv IssuesdixitBhavak DixitAinda não há avaliações