Você também pode gostar

- Overhead VariancesDocumento11 páginasOverhead VariancesDanica VillaganteAinda não há avaliações

- 3.sales Variance AnalysisDocumento38 páginas3.sales Variance Analysiskamasuke hegdeAinda não há avaliações

- Cost ManagementDocumento18 páginasCost ManagementGeo Rublico ManilaAinda não há avaliações

- Finance Assignment InstructionDocumento7 páginasFinance Assignment InstructionJe-Ta CllAinda não há avaliações

- Lecture 5: Interest Rate Risk (Part I) : DR Lixiong Guo Semester 2, 2015Documento31 páginasLecture 5: Interest Rate Risk (Part I) : DR Lixiong Guo Semester 2, 2015studentAinda não há avaliações

- Chapter 7Documento53 páginasChapter 7Baby KhorAinda não há avaliações

- Standard Costing and Variance Analysis: Fall 2007 CrossonDocumento20 páginasStandard Costing and Variance Analysis: Fall 2007 CrossonBernard SalongaAinda não há avaliações

- CH 8Documento16 páginasCH 8emanmamdouh596Ainda não há avaliações

- CH 13Documento28 páginasCH 13ReneeAinda não há avaliações

- Module IV - Working Capital ManagementDocumento50 páginasModule IV - Working Capital ManagementAshwin DholeAinda não há avaliações

- BM Introduction To BankingDocumento36 páginasBM Introduction To BankingNatasha OliviaAinda não há avaliações

- Target Costing Presentation FinalDocumento57 páginasTarget Costing Presentation FinalMr Dampha100% (1)

- International FInanceDocumento3 páginasInternational FInanceJemma JadeAinda não há avaliações

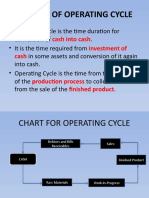

- Concept of Operating Cycle: Cash Into Cash Investment of CashDocumento6 páginasConcept of Operating Cycle: Cash Into Cash Investment of CashVenket RamanaAinda não há avaliações

- Chapter Five: The Financial Statements of Banks and Their Principal CompetitorsDocumento58 páginasChapter Five: The Financial Statements of Banks and Their Principal CompetitorsYoussef Youssef Ahmed Abdelmeguid Abdel LatifAinda não há avaliações

- MCS Assignment - 3Documento13 páginasMCS Assignment - 3MIRAL PATELAinda não há avaliações

- KOCH6Documento63 páginasKOCH6Swati SoniAinda não há avaliações

- Throughput Accounting: Prepared by Gwizu KDocumento26 páginasThroughput Accounting: Prepared by Gwizu KTapiwa Tbone Madamombe100% (1)

- Duration GAP AnalysisDocumento5 páginasDuration GAP AnalysisShubhash ShresthaAinda não há avaliações

- Transfer PricingDocumento57 páginasTransfer PricingbijoyendasAinda não há avaliações

- BEP N CVP AnalysisDocumento49 páginasBEP N CVP AnalysisJamaeca Ann MalsiAinda não há avaliações

- Product Life Cycle Costing / Whole Life Cycle Costing /life Cycle CostingDocumento23 páginasProduct Life Cycle Costing / Whole Life Cycle Costing /life Cycle CostingTapiwa Tbone MadamombeAinda não há avaliações

- Lecture 2: Exchange Rates and The Foreign Exchange Market: TopicsDocumento79 páginasLecture 2: Exchange Rates and The Foreign Exchange Market: TopicsSalvio MachaAinda não há avaliações

- Financial Derivatives: Prof. Scott JoslinDocumento49 páginasFinancial Derivatives: Prof. Scott Joslinarnav100% (2)

- Part Seven: THE Management of Financial InstitutionsDocumento40 páginasPart Seven: THE Management of Financial InstitutionsIrakli SaliaAinda não há avaliações

- Transfer Price Case Study 2Documento1 páginaTransfer Price Case Study 2Professor Sameer Kulkarni100% (5)

- Cash Coversion CYcleDocumento29 páginasCash Coversion CYcleZohaib HassanAinda não há avaliações

- Throughput Accounting: Today's Topics: HomeworkDocumento5 páginasThroughput Accounting: Today's Topics: HomeworkpalaviyaAinda não há avaliações

- ThroughputDocumento15 páginasThroughputVaibhav KocharAinda não há avaliações

- CHP 12 - Strategy, Balanced Scorecard, and Strategic Profitability (With Answers)Documento54 páginasCHP 12 - Strategy, Balanced Scorecard, and Strategic Profitability (With Answers)kenchong7150% (1)

- CVP AnalysisDocumento36 páginasCVP AnalysisNadian100% (1)

- Chapter 4Documento45 páginasChapter 4Yanjing Liu67% (3)

- Activity Based CostingDocumento51 páginasActivity Based CostingAbdulyunus AmirAinda não há avaliações

- Feasibility Study TemplateDocumento6 páginasFeasibility Study TemplateMUTHUVEL MAinda não há avaliações

- Capital BudgetingDocumento31 páginasCapital BudgetinggulafridiAinda não há avaliações

- Cost & Management Accounting - Paper 7Documento7 páginasCost & Management Accounting - Paper 7Turyamureeba JuliusAinda não há avaliações

- Assignment 1 - Investment AnalysisDocumento5 páginasAssignment 1 - Investment Analysisphillimon zuluAinda não há avaliações

- Target - Costing F5 NotesDocumento4 páginasTarget - Costing F5 NotesSiddiqua KashifAinda não há avaliações

- International Finance Lecture SlidesDocumento27 páginasInternational Finance Lecture Slidesmaryam ashfaqAinda não há avaliações

- Target CostingDocumento9 páginasTarget CostingRahul PandeyAinda não há avaliações

- PPT-4 Parity Conditions and Currency ForecastingDocumento42 páginasPPT-4 Parity Conditions and Currency ForecastingKamal KantAinda não há avaliações

- Hierarchy of VariancesDocumento1 páginaHierarchy of VariancesQaisar AbbasAinda não há avaliações

- IMT 58 Management Accounting M3Documento23 páginasIMT 58 Management Accounting M3solvedcareAinda não há avaliações

- Assignment 3Documento7 páginasAssignment 3Abdullah ghauriAinda não há avaliações

- Cost II Chapter ThreeDocumento11 páginasCost II Chapter ThreeSemira100% (1)

- Lecture 2 BEP Numericals AnswersDocumento16 páginasLecture 2 BEP Numericals AnswersSanyam GoelAinda não há avaliações

- Product Costing: Job and Process Operations: Learning Objectives - Coverage by QuestionDocumento45 páginasProduct Costing: Job and Process Operations: Learning Objectives - Coverage by QuestionJoeAinda não há avaliações

- Presented By: Ubaid Azam Wardag Babar Mustafa Muhammad UsmanDocumento13 páginasPresented By: Ubaid Azam Wardag Babar Mustafa Muhammad UsmanShahid AshrafAinda não há avaliações

- Capital Budgeting Techniques Capital Budgeting TechniquesDocumento58 páginasCapital Budgeting Techniques Capital Budgeting TechniquesMuhammad ZeeshanAinda não há avaliações

- 3 - Cost Volume Profit AnalysisDocumento1 página3 - Cost Volume Profit AnalysisPattraniteAinda não há avaliações

- Variable Production Overhead Variance (VPOH)Documento9 páginasVariable Production Overhead Variance (VPOH)Wee Han ChiangAinda não há avaliações

- Chapter 10 SolutionsDocumento68 páginasChapter 10 SolutionsMasha LankAinda não há avaliações

- Pricing PracticesDocumento43 páginasPricing PracticesLeiza FroyaldeAinda não há avaliações

- 324 - International Parity ConditionsDocumento49 páginas324 - International Parity ConditionsTamuna BibiluriAinda não há avaliações

- Topic 2 Support Department Cost AllocationDocumento27 páginasTopic 2 Support Department Cost Allocationluckystar251095Ainda não há avaliações

- Chapter 3 Life Cycle Costing: Answer 1 Target Costing Traditional ApproachDocumento11 páginasChapter 3 Life Cycle Costing: Answer 1 Target Costing Traditional ApproachadamAinda não há avaliações

- Financial Statements, Taxes, and Cash FlowDocumento32 páginasFinancial Statements, Taxes, and Cash Flowhafsa salmanAinda não há avaliações

- Suggested Answers (Chapter 7)Documento7 páginasSuggested Answers (Chapter 7)kokomama231Ainda não há avaliações

- 08 QuestionsDocumento8 páginas08 Questionsw_sampathAinda não há avaliações

- Cost Volume Profit Analysis For Paper 10Documento6 páginasCost Volume Profit Analysis For Paper 10Zaira Anees100% (1)

- MCQs EconomicsDocumento34 páginasMCQs Economicskhalid nazir90% (10)

- Project Report On Inflation NewDocumento78 páginasProject Report On Inflation NewArjun JhAinda não há avaliações

- REVISED NOTES OF FOREIGN EXCHANGE Unit 1 2 - 1Documento40 páginasREVISED NOTES OF FOREIGN EXCHANGE Unit 1 2 - 1komalAinda não há avaliações

- Arithmetic: Problems For PracticeDocumento3 páginasArithmetic: Problems For PracticeArchit HingeAinda não há avaliações

- SubsidiesDocumento5 páginasSubsidiesMahendra ChhetriAinda não há avaliações

- Supply Chain ManagementDocumento2 páginasSupply Chain ManagementAhmed Jan Dahri100% (1)

- The 15 Truths No Coin Dealer Wants You To KnowDocumento36 páginasThe 15 Truths No Coin Dealer Wants You To KnowuighuigAinda não há avaliações

- ValueInvestorInsight Issue 364Documento21 páginasValueInvestorInsight Issue 364freemind3682Ainda não há avaliações

- Chapter 3 MCQs and Analytical Qs Supply and DemandDocumento8 páginasChapter 3 MCQs and Analytical Qs Supply and Demandhamna ikramAinda não há avaliações

- 2012 The Economics of Lotteries A Survey of The LiteratureDocumento40 páginas2012 The Economics of Lotteries A Survey of The LiteratureLe Doan Trung KhangAinda não há avaliações

- Trading GAPS Lazy Trader PDFDocumento12 páginasTrading GAPS Lazy Trader PDFAnonymous LhmiGjO71% (14)

- GBC ECON 101 S1 2023 AssignmentDocumento6 páginasGBC ECON 101 S1 2023 AssignmentBonkAinda não há avaliações

- ENTREP 1 Chapter 5 Opportunity SeizingDocumento92 páginasENTREP 1 Chapter 5 Opportunity SeizingCristineJoyceMalubayIIAinda não há avaliações

- Design BidDocumento57 páginasDesign BidpraveenAinda não há avaliações

- Buying Motives and RoleDocumento20 páginasBuying Motives and RoleBAHHEP BAHHEPAinda não há avaliações

- Assignment On EconomicsDocumento17 páginasAssignment On EconomicsRanganathan ChandrasekhranAinda não há avaliações

- SOL BA Program 1st Year Economics Study Material and Syllabus in PDFDocumento87 páginasSOL BA Program 1st Year Economics Study Material and Syllabus in PDFShamim Akhtar100% (1)

- Fundamentals of Supply and DemandDocumento3 páginasFundamentals of Supply and Demandpierre ejarqueAinda não há avaliações

- Almgren & Chriss - Optimal Execution of Portfolio TransactionsDocumento42 páginasAlmgren & Chriss - Optimal Execution of Portfolio TransactionsehkereiakesAinda não há avaliações

- United States Court of Appeals Second Circuit.: No. 430, Docket 28670Documento8 páginasUnited States Court of Appeals Second Circuit.: No. 430, Docket 28670Scribd Government DocsAinda não há avaliações

- Economics by Nitesh SirDocumento73 páginasEconomics by Nitesh SirKhalid gowharAinda não há avaliações

- Project ManagementDocumento58 páginasProject ManagementAyush VarshneyAinda não há avaliações

- PES Question-Accounting Exercise 2.1 SalamDocumento11 páginasPES Question-Accounting Exercise 2.1 SalamSolomon Tekalign100% (2)

- Commodity MarketingDocumento21 páginasCommodity MarketingNgoni MukukuAinda não há avaliações

- Om Co4 MaterialDocumento51 páginasOm Co4 MaterialvamsibuAinda não há avaliações

- 2019 Fuhrmann B Introduction To Business and EconomicsDocumento64 páginas2019 Fuhrmann B Introduction To Business and EconomicsDaka Radhiyan YahyaAinda não há avaliações

- 9 .Pricing StrategiesDocumento18 páginas9 .Pricing StrategiesMarylyn Tenorio LaxamanaAinda não há avaliações

- Dwnload Full Economics Today The Micro View 19th Edition Miller Solutions Manual PDFDocumento35 páginasDwnload Full Economics Today The Micro View 19th Edition Miller Solutions Manual PDFirisybarrous100% (10)

- Icaew Cfab Mi 2019 Study GuideDocumento42 páginasIcaew Cfab Mi 2019 Study GuideAnonymous ulFku1vAinda não há avaliações

- What Is A Platform?Documento49 páginasWhat Is A Platform?sasobaidAinda não há avaliações