Você também pode gostar

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5795)

- BCOM 206 Business CommunicationDocumento281 páginasBCOM 206 Business CommunicationtulikaAinda não há avaliações

- IKIKE-CIC - ITT RevDocumento99 páginasIKIKE-CIC - ITT RevMathias Onosemuode100% (1)

- U3 Barrett What Motivates EmployeesDocumento11 páginasU3 Barrett What Motivates EmployeesNadia ClosterAinda não há avaliações

- Management Notes and Discussion QuestionsDocumento4 páginasManagement Notes and Discussion Questionsapi-308919474Ainda não há avaliações

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- 01.12 - Info A A NR 80 - 10 01 2012 ANEXA EthiopiaDocumento96 páginas01.12 - Info A A NR 80 - 10 01 2012 ANEXA EthiopiaChirag Fulwani100% (1)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- MRFDocumento6 páginasMRFSmartvijay Kula100% (1)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Labor 1 - Module 5 - Conditions of Employment - Working Conditions and Rest Periods-1Documento101 páginasLabor 1 - Module 5 - Conditions of Employment - Working Conditions and Rest Periods-1LoAinda não há avaliações

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Housing Loan Application Form (HLA-2019-001)Documento2 páginasHousing Loan Application Form (HLA-2019-001)Michael DaviesAinda não há avaliações

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- Balanced Score CardDocumento9 páginasBalanced Score Cardfahmi810091Ainda não há avaliações

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- Trade Union ActDocumento29 páginasTrade Union ActAkshaya Mali100% (1)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- Your Name: (XXX) XXX-XXXX 142 Your Address BLVD, City Name, CA XXXXXDocumento2 páginasYour Name: (XXX) XXX-XXXX 142 Your Address BLVD, City Name, CA XXXXXNiravsinh ParmarAinda não há avaliações

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Go Forward Tech BriefingDocumento36 páginasGo Forward Tech BriefingThe Vancouver Sun100% (2)

- The Benefits of Free TradeDocumento30 páginasThe Benefits of Free TradeBiway RegalaAinda não há avaliações

- Submitted By:-: Name COLLEGE, Name Rajesh Kumar CABM-Pantnagar, Gbpua&TDocumento21 páginasSubmitted By:-: Name COLLEGE, Name Rajesh Kumar CABM-Pantnagar, Gbpua&Trajesh_chintu100% (1)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- Sports Equipment Retail Business PlanDocumento8 páginasSports Equipment Retail Business PlanSachinAinda não há avaliações

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- Teacher Performance AppraisalDocumento6 páginasTeacher Performance AppraisalRichard sonAinda não há avaliações

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- AmBisyon 2040: Highlights of The National Survey On The Aspirations of The Filipino PeopleDocumento2 páginasAmBisyon 2040: Highlights of The National Survey On The Aspirations of The Filipino PeopleFrancisco Ashley AcedilloAinda não há avaliações

- Copa RFPDocumento181 páginasCopa RFPThe Daily LineAinda não há avaliações

- The Chandigarh Minimum Wages Notification 1st April 2019Documento4 páginasThe Chandigarh Minimum Wages Notification 1st April 2019Manish ShahAinda não há avaliações

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Training Strategy: Management and Professional Development DepartmentDocumento42 páginasTraining Strategy: Management and Professional Development DepartmentschehzadAinda não há avaliações

- Part 3 Microeconomic Decision Makers: Activities: Guidance and AnswersDocumento15 páginasPart 3 Microeconomic Decision Makers: Activities: Guidance and Answerskmmanoj1968100% (1)

- Evaluate The Market Image of Protik Developers Ltd. Comparing With Other Existing Competitor of Same MarketDocumento53 páginasEvaluate The Market Image of Protik Developers Ltd. Comparing With Other Existing Competitor of Same Marketd-fbuser-209866690Ainda não há avaliações

- Pinkerton ApplicationDocumento6 páginasPinkerton ApplicationPraveen AntonyAinda não há avaliações

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1091)

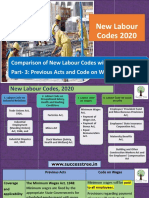

- 4 Comparing Previous Act With New Labour Codes (Part - 3)Documento13 páginas4 Comparing Previous Act With New Labour Codes (Part - 3)abdul gani khanAinda não há avaliações

- Business and Management HL P2 MsDocumento25 páginasBusiness and Management HL P2 MsSharmel Altamirano SancanAinda não há avaliações

- The Debate On DeindustrializationDocumento18 páginasThe Debate On DeindustrializationHarshita SaxenaAinda não há avaliações

- PVR Projects Limited: Sub Contractor Registration & EvaluationDocumento2 páginasPVR Projects Limited: Sub Contractor Registration & EvaluationSuppu GeniousAinda não há avaliações

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Cuba'S Economy After Raúl Castro: A Tale of Three Worlds: Richard E. FeinbergDocumento21 páginasCuba'S Economy After Raúl Castro: A Tale of Three Worlds: Richard E. FeinbergMilton-GenesisAinda não há avaliações

- 20 Aug MOA Template For Work Immersion Cooperative MADDocumento7 páginas20 Aug MOA Template For Work Immersion Cooperative MADFernan Enad100% (3)

- Annual Leave SampleDocumento14 páginasAnnual Leave SampleRichard Thodé Jr100% (1)